Login to access

Want to subscribe?

This article is part of: Network Innovation

To find out more about how to join or access this report please contact us

Fixed Wireless Access (FWA) is becoming a mainstream proposition across urban, rural and developing environments. 5G is an important enabler but not the only one. Unusually, FWA will benefit almost all market players – fixed and mobile operators, vendors, investors and regulators. This report contains our 5-year forecast and recommendations for all players.

=======================================================================================

Download the additional file on the left for the PPT chart pack accompanying this report

=======================================================================================

Fixed wireless access growth forecast

Fixed Wireless Access (FWA) networks use a wireless “last mile” link for the final connection of a broadband service to homes and businesses, rather than a copper, fibre or coaxial cable into the building. Provided mostly by WISPs (Wireless Internet Service Providers) or mobile network operators (MNOs), these services come in a wide range of speeds, prices and technology architectures.

Some FWA services are just a short “drop” from a nearby pole or fibre-fed hub, while others can work over distances of several kilometres or more in rural and remote areas, sometimes with base station sites backhauled by additional wireless links. WISPs can either be independent specialists, or traditional fixed/cable operators extending reach into areas they cannot economically cover with wired broadband.

There is a fair amount of definitional vagueness about FWA. The most expansive definitions include cheap mobile hotspots (“Mi-Fi” devices) used in homes, or various types of enterprise IoT gateway, both of which could easily be classified in other market segments. Most service providers don’t give separate breakouts of deployments, while regulators and other industry bodies report patchy and largely inconsistent data.

Our view is that FWA is firstly about providing permanent broadband access to a specific location or premises. Primarily, this is for residential wireless access to the Internet and sometimes typical telco-provided services such as IPTV and voice telephony. In a business context, there may be a mix of wireless Internet access and connectivity to corporate networks such as VPNs, again provided to a specific location or building.

A subset of FWA relates to M2M usage, for instance private networks run by utility companies for controlling grid assets in the field. These are typically not Internet-connected at all, and so don’t fit most observers’ general definition of “broadband access”.

Usually, FWA will be marketed as a specific service and package by some sort of network provider, usually including the terminal equipment (“CPE” – customer premise equipment), rather than allowing the user to “bring their own” device. That said, lower-end (especially 4G) offers may be SIM-only deals intended to be used with generic (and unmanaged) portable hotspots.

There are some examples of private network FWA, such as a large caravan or trailer park with wireless access provided from a central point, and perhaps in future municipal or enterprise cellular networks giving fixed access to particular tenant structures on-site – for instance to hangars at an airport.

Enter your details below to request an extract of the report

FWA today

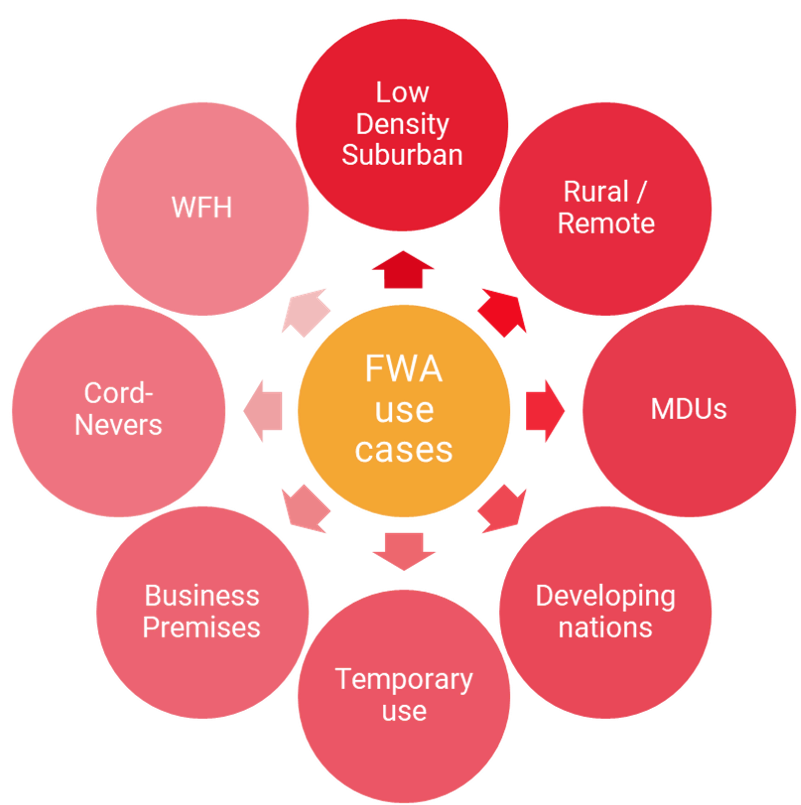

Today, fixed-wireless access (FWA) is used for perhaps 8-9% of broadband connections globally, although this varies significantly by definition, country and region. There are various use cases (see below), but generally FWA is deployed in areas without good fixed broadband options, or by mobile-only operators trying to add an additional fixed revenue stream, where they have spare capacity.

Fixed wireless internet access fits specific sectors and uses, rather than the overall market

Source: STL Partners

FWA has traditionally been used in sparsely populated rural areas, where the economics of fixed broadband are untenable, especially in developing markets without existing fibre transport to towns and villages, or even copper in residential areas. Such networks have typically used unlicensed frequency bands, as there is limited interference – and little financial justification for expensive spectrum purchases. In most cases, such deployments use proprietary variants of Wi-Fi, or its ill-fated 2010-era sibling WiMAX.

Increasingly however, FWA is being used in more urban settings, and in more developed market scenarios – for example during the phase-out of older xDSL broadband, or in places with limited or no competition between fixed-network providers. Some cellular networks primarily intended for mobile broadband (MBB) have been used for fixed usage as well, especially if spare capacity has been available. 4G has already catalysed rapid growth of FWA in numerous markets, such as South Africa, Japan, Sri Lanka, Italy and the Philippines – and 5G is likely to make a further big difference in coming years. These mostly rely on licensed spectrum, typically the national bands owned by major MNOs. In some cases, specific bands are used for FWA use, rather than sharing with normal mobile broadband. This allows appropriate “dimensioning” of network elements, and clearer cost-accounting for management.

Historically, most FWA has required an external antenna and professional installation on each individual house, although it also gets deployed for multi-dwelling units (MDUs, i.e. apartment blocks) as well as some non-residential premises like shops and schools. More recently, self-installed indoor CPE with varying levels of price and sophistication has helped broaden the market, enabling customers to get terminals at retail stores or delivered direct to their home for immediate use.

Looking forward, the arrival of 5G mass-market equipment and larger swathes of mmWave and new mid-band spectrum – both licensed and unlicensed – is changing the landscape again, with the potential for fibre-rivalling speeds, sometimes at gigabit-grade.

Enter your details below to request an extract of the report

Table of contents

- Executive Summary

- Introduction

- FWA today

- Universal broadband as a goal

- What’s changed in recent years?

- What’s changed because of the pandemic?

- The FWA market and use cases

- Niche or mainstream? National or local?

- Targeting key applications / user groups

- FWA technology evolution

- A broad array of options

- Wi-Fi, WiMAX and close relatives

- Using a mobile-primary network for FWA

- 4G and 5G for WISPs

- Other FWA options

- Customer premise equipment: indoor or outdoor?

- Spectrum implications and options

- The new FWA value chain

- Can MNOs use FWA to enter the fixed broadband market?

- Reinventing the WISPs

- Other value chain participants

- Is satellite a rival waiting in the wings?

- Commercial models and packages

- Typical pricing and packages

- Example FWA operators and plans

- STL’s FWA market forecasts

- Quantitative market sizing and forecast

- High level market forecast

- Conclusions

- What will 5G deliver – and when and where?

- Index