Telcos and AI: How to follow the money

STL Partners’ vision for telco growth in the Coordination Age and the AI era

STL Partners’ vision for telco growth in the Coordination Age and the AI era

In 2006, STL Partners came up with a bold new vision for the telecoms industry to use its communications, connectivity, and other capabilities (such as billing, identity, authentication, security, analytics) to build a two-sided platform that enables enterprises to interact with each other and consumers more effectively. We dubbed this Telco 2.0 and the last version of the Telco 2.0 manifesto we published can be found here – we feel it was prescient and that many of the points we made still resonate today. Indeed, many telecoms operators have embraced the Telco 2.0 two-sided business model over the last ten years.

As cloud computing, machine learning, IoT and automation technologies evolved, in 2018 we published the Coordination Age Manifesto, proposing a role for telecom operators in aligning technology and stakeholders in their national markets to drive efficiency in both natural and human resources. In this manifesto and our projection for Telco in 2030 we also proposed how telcos could gradually grow their investments in R&D to re-establish themselves at technology innovators.

Although many operators have built businesses beyond core connectivity, leveraging platform and cloud-based business models to combine more flexible connectivity with cloud, security, analytics and vertically tailored services, the industry has thus far failed to achieve any fundamental shift in its business model.

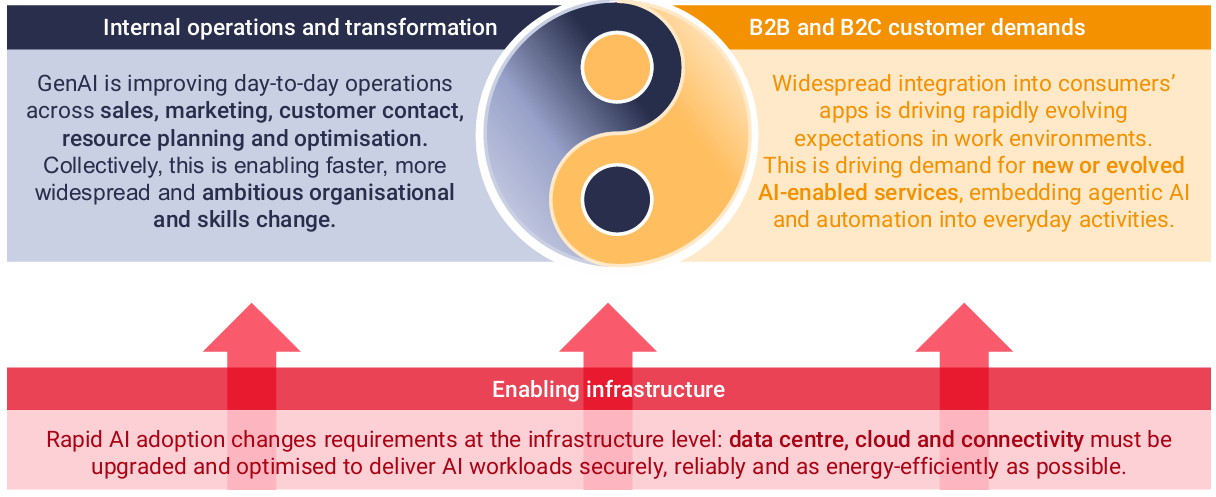

Since 2022, the emergence of generative AI has brought many of the concepts we outlined in the Coordination Age Manifesto to life. For example, much more powerful and accessible AI technologies are enabling:

Fundamentally, it is now much easier to achieve the coordination STL envisaged and AI technologies are now far more accessible to employees at all levels. This technology revolution has also happened alongside the gradual shift towards more cloudified and automated network operations – an essential foundation to providing on-demand, cloud-based connectivity services.

Generative AI may grow into the third industrial revolution, offering telecom operators with high ambitions a generational opportunity to re-establish themselves at the forefront of technological transformation.

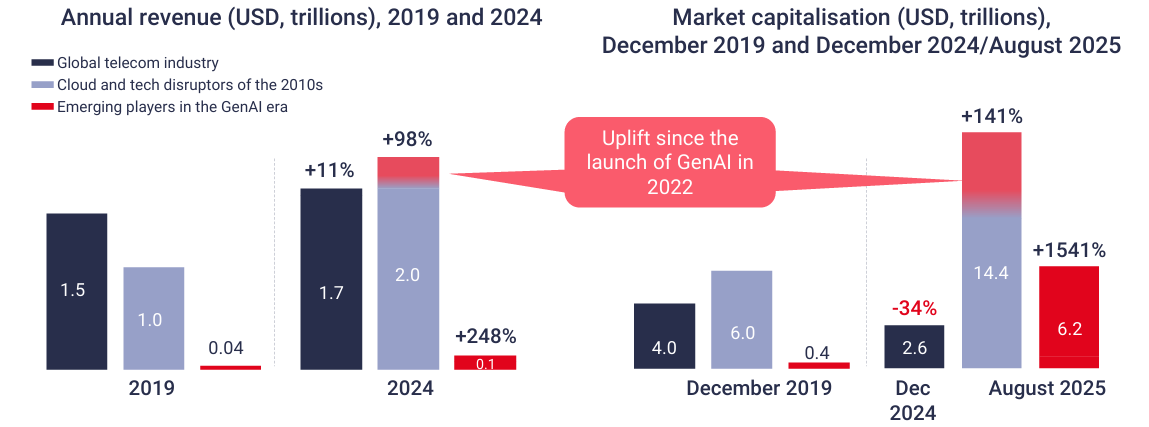

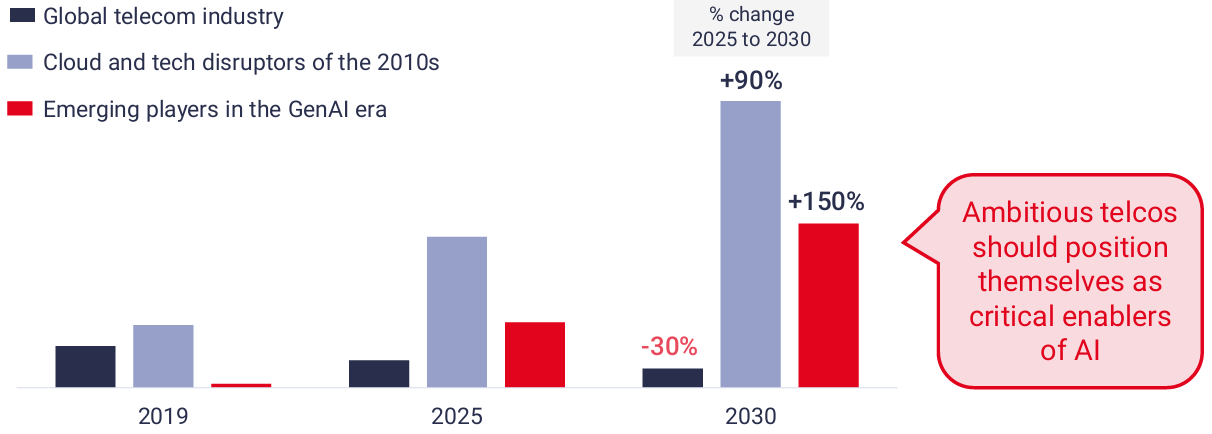

Since 2019 – and the emergence of GenAI in 2022 – financial markets have continued to reward the hyperscale cloud and tech disruptors of the 2010s, as they have pivoted their businesses towards R&D in GenAI. Despite most of their revenue growth since 2019 occurring before GenAI was launched in 2022, the continued rise in their market capitalisation suggests that investors believe they will capture a large share of future AI revenues.

Companies providing the infrastructure and technology most specifically aligned with generative AI – GPUs (Nvidia, TSMC) and LLMs (OpenAI, Anthropic) – have seen their market capitalisation and revenues grow even faster.

Despite connectivity remaining an essential piece of the AI value chain and achieving some revenue growth over the past five years, telecom operators have fallen under increasing pressure from investors.

Source: Company annual reports, Telegeography, Deloitte, STL Partners analysis

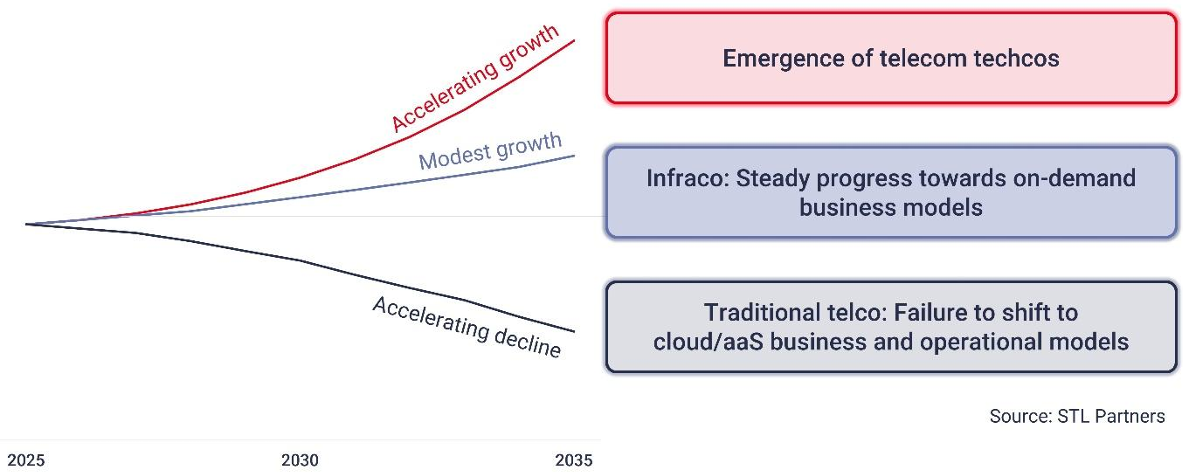

As the AI era unfolds, we project three scenarios for telco revenues over the next 5-10 years. We believe that the determining factor for telcos is the degree to which they can evolve their business and operational models.

Those that don’t change how they supply and sell connectivity will not survive. Those that do make these changes will maintain the trajectory the industry has followed over the last five years – modest revenue growth, but further drops in market capitalisation. Those that change how they supply and sell connectivity and successfully innovate unique new services on top of their core expertise may break the mould to achieve accelerating revenue growth.

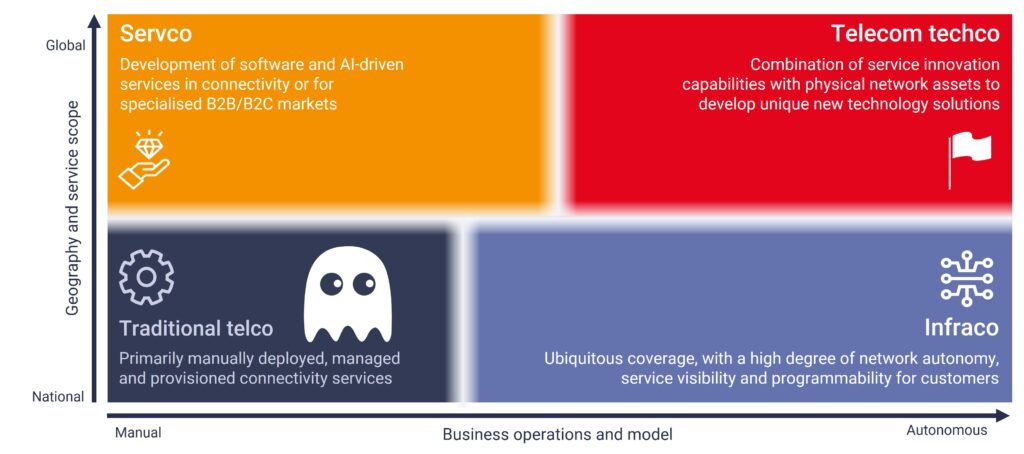

Traditional telco:

Infraco:

Telecom techco:

Our expectation is that most telecom operators will follow the infraco path, although some will fail to evolve and any remaining assets will get swallowed up by more successful operators. A small subset of telcos may break the mould to become true telecom techcos.

Assuming telecom operators follow the most predictable path – i.e., they become infracos – we project the current downwardmarket capitalisation trend to continue.

Extrapolating past performance out to 2030 would see existing tech giants and emerging AI players’ financial market valuations continue to significantly outperform the overall telecom industry, while telcos will increasingly be seen as utility providers.

Telcos must, at the very least, capitalise on the growing connectivity needs of AI applications. They also risk missing out on a generational opportunity if they don’t attempt to meet distributed compute needs as they arise.

AI inferencing will be the big story in demand for compute over the next 10 years. It is not a given that this will require distributed compute, but the velocity of innovation means that regardless of how distributed compute power will be, global players will not hold a monopoly. They will not be able to serve the vast range of customer needs and adapt to national regulations in every market.

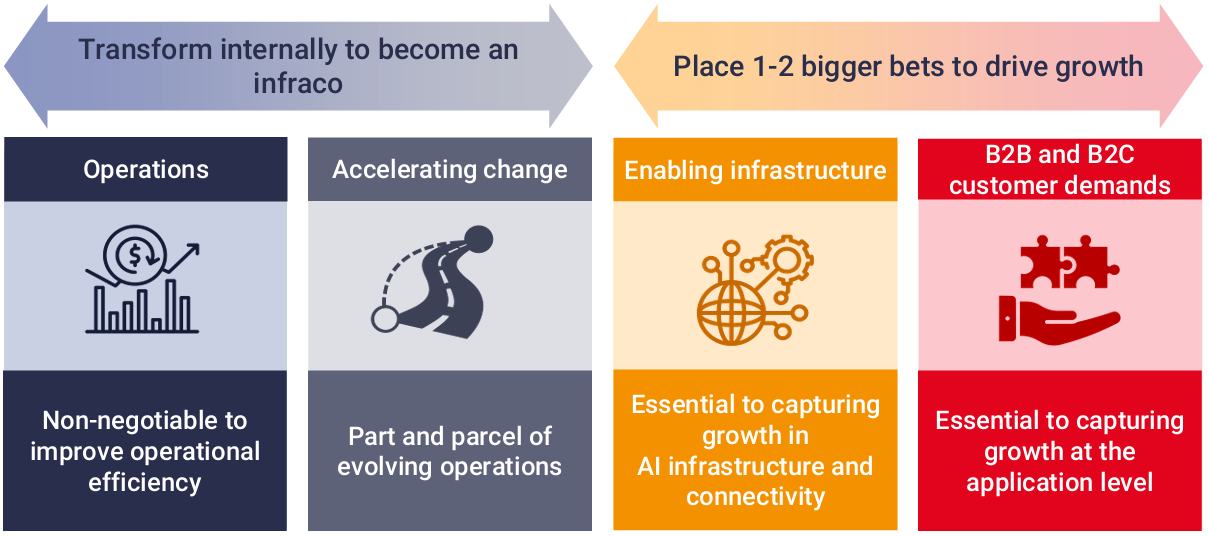

In this context, the priority for every player in telecoms seeking to achieve meaningful long-term growth – telco or vendor – is to have a clear view of how AI will change both what and how they sell to customers. What changes are non-negotiable and will become table stakes, and which bets can enable them to break the mould of ongoing commoditisation?