Login to access

Want to subscribe?

This article is part of: Executive Briefing Service Executive Briefing Service

To find out more about how to join or access this report please contact us

Transformation lies at the heart of most telecoms operators’ strategies but change at companies is painfully slow. This report explains why agility and innovation – the goals of transformation – will remain elusive until CFOs adopt new resource allocation models at their organisations.

The telecoms operator’s conundrum – how to break the service innovation status quo

Telco CFOs need to upweight telecoms R&D investments to drive differentiating service innovations. If they don’t, telcos will recede further into the category of low yield, low growth commodities.

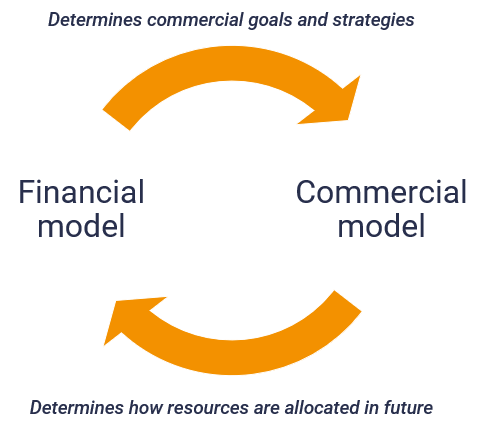

The relationship between a company’s financial and commercial model is complex:

- The financial model determines the commercial model of a company – what commercial goals it is able to pursue and how it is able to pursue them

- But the commercial model also feeds directly back into the financial model of the business and determines how resources are allocated

The interrelatedness of commercial and financial models means that change is sometimes difficult – a ‘chicken and egg’ situation occurs in which each model relies on change in the other before it can change.

Enter your details below to request an extract of the report

This ‘chicken and egg’ situation is apparent within the telecoms industry:

- Business owners within operators want their organisation to become more agile, more flexible, more innovative which implies having resources that can be (re)deployed quickly, but they find it hard to secure budget owing to the huge and slow capital investment programmes involved in upgrading networks

- Finance departments at the same organisations want to deploy resources efficiently to maximise returns and capital investment in the existing business model (infrastructure that drives connectivity revenue) has a much stronger ROI than speculative operating expenditure in platforms and services that have (so far) proved unsuccessful

The result is status quo: the same financial model drives the same commercial model at a time when returns for core services are reducing every year.

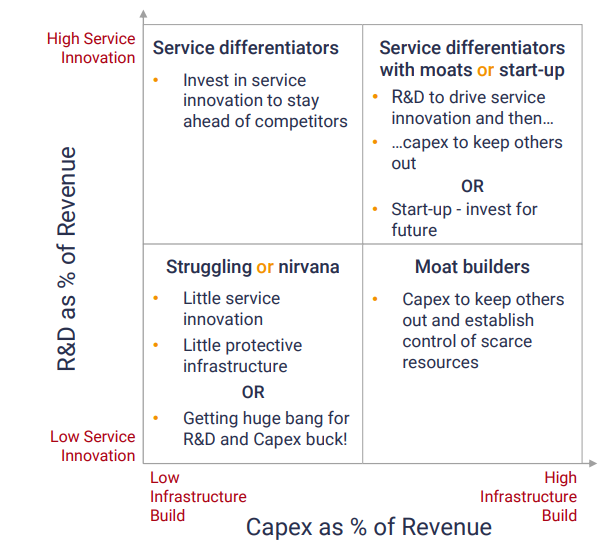

We start by mapping out the relationship between financial and commercial models…

In this framework, we use R&D operating expenditure (vertical axis) as a proxy for service innovation. We recognise that this is not perfect as service innovation requires much more than R&D. Nevertheless, it is probably fair to say that service innovation is unlikely to be sustained without material R&D expenditure.

Capital investment (horizontal axis) is a proxy for infrastructure build – developing assets which will generate returns over a long period of time such as buildings, manufacturing plants, telecoms networks.

Telcos are classic ‘Moat builders’, making money from capital investment in infrastructure and putting little into telecoms R&D investments.

The Internet giants and tech players typically start out as ‘service differentiators’, keeping capital investment light and instead focusing on flexible operating expenditure to drive service innovation. Increasingly however, they are investing capital in cloud computing infrastructure, to construct moats to protect their services – giving them cheaper distribution and better customer experience than smaller competitors.

A framework for understanding capex versus R&D spending

Source: STL Partners

…which reveals that telcos are moat builders and are radically out-invested in service innovation by tech players

Historically, for telecoms operators service innovation resulted from network capital investment because voice and messaging services were integrated into there were no alternative sources for communications – a customer had to use the service provider by the telecoms operator:

- Telcos effectively outsourced innovation to Network Equipment Players (NEPs)

- There was no need to invest significantly in R&D

Now, services are independent of the network (thanks to the internet) – telco customers can use communication (and other) services provided by dozens of third-parties and value has shifted to companies (such as the internet giants and tech companies) that invest in service innovation.

Telcos still invest only in infrastructure but value is increasingly in network-independent services so they are missing out on value-creation and are instead competing on price on the only commodity service that third-parties cannot substitute: connectivity.

R&D and Capex % of Revenue, 2017

Source: Company accounts, STL Partners analysis

Proof point: Internet players are vastly more valuable than telecoms operators

Revenue and Market Capitalisation 2017. Telco v Internet

Source: Company accounts, stock market data, STL Partners analysis

Seven internet giants’ market capitalisation is bigger than 165 telecoms operators combined because:

Service innovation + moats = Revenue + profit growth = Future value creation

In other words, telcos’ current business model (financial and commercial models) are not deemed to be strong value creators.

The result is that capital markets demand that operators hand profits back to investors in the form of high-dividend yields so that they can invest in higher-growth companies.

In the rest of this report, we outline why CFOs need to drive business model change that will enable telcos to compete more effectively as ‘Service differentiators’, and four steps they should take to start this process – fundamentally increasing telecoms R&D investments.