Login to access

Want to subscribe?

This article is part of: Executive Briefing Service, Consumer

To find out more about how to join or access this report please contact us

Why did AT&T buy, and then sell, DirecTV and Time Warner after only six years? This report looks at AT&T’s decisions, actions and their consequences, and the lessons for others attempting adjacent market moves and M&A.

How AT&T entered and exited the media business

AT&T enters the satellite market at its peak

In 2014, AT&T announced it was buying DirecTV. By that time, AT&T was already bundling DirecTV with its phone and internet service and had approximately 5.9 million linear pay-TV (U-Verse) video subscribers. However, this pay-TV business was already experiencing decline, to the extent that when the DirecTV merger completed in mid-2015, U-Verse subscribers had fallen to 5.6 million by the end of that year.

With the acquisition of DirecTV, AT&T went from a small player in the media and entertainment industry to one of the largest media players in the world adding 39.1 million (US and Latin American) subscribers and paying $48.5bn ($67bn including debt) to acquire the business. The rationale for this acquisition (the satellite business) was to compete with cable operators by being able to offer broadband, increasing AT&T’s addressable market beyond its fibre-based U-Verse proposition which was only available in certain locations/states.

AT&T and DirecTV enjoyed an initial honeymoon, period recording growth up until the end of 2016 when DirecTV subscribers peaked at just over 21 million in the US.

From this point onwards however, AT&T’s satellite subscribers went into decline as customers switched to cheaper competitor offers as well as online streaming services. The popularity of streaming services was reflected by moves among traditional media players to develop their own streaming services such as Time Warner’s HBO GO and HBO NOW. In 2015, DirectTV’s satellite competitor Dish TV likewise launched its own streaming service Sling TV.

Even though it was one of the largest TV distributors on a satellite platform, AT&T also believed online streaming was its ultimate destination. Prior to the launch of its streaming service in late 2016, Bloomberg reported that AT&T envisioned DirecTV NOW as its primary video platform by 2020.

A softwarised platform delivered lowered costs as the service could be self-installed by customers and didn’t rely on expensive truck roll installation or launching satellites. The improved margins would enable AT&T to promote TV packages at attractive price points which would balance inflation demands from broadcasters for the cost of TV programming. AT&T could also more easily bundle the softwarised TV service with its broadband, fibre and wireless propositions and earn more lucrative advertising revenue based on its own network and viewer insights.

Enter your details below to request an extract of the report

The beginnings of a bumpy journey in TV

AT&T’s foray into satellite and streaming TV can be characterised by a series of confusing service propositions for both consumers and AT&T staff, expensive promotional activity and overall pricing/product design misjudgements as well as troubled relations with TV broadcasters resulting in channel blackouts and ultimately churn.

Promotion, pull back and decline of DirecTV NOW

DirectTV NOW launched in November 2016, as AT&T’s first over the top (OTT) low cost online streaming service. Starting at $35 per month for 60+ channels with no contract period, analysts called the skinny TV package as a loss leader given the cost of programming rights and high subscriber acquisition costs (SACs). The loss leader strategy was aimed at acquiring wireless and broadband customers and included initiatives such as:

- Promotional discounts to its monthly $60 mid-tier 100+ channel package reduced to $35 per month for life (subject to programming costs).

- Device promotions and monthly waivers. The service eventually became available on popular streaming devices (Roku, Xbox and PlayStation) and included promotions such as an Apple TV 4K with a four month subscription waiver, a Roku Streaming Stick with a one month waiver or a $25 discount on the first month.

- Customers could also add HBO or Cinemax for an additional $5 per month, which again was seen as a costly subsidy for AT&T to offer.

The service didn’t include DirecTV satellite’s popular NFL Sunday Ticket programming as Verizon held the smartphone rights to live NFL games, nor did it come with other popular shows from programme channels such as CBS. Features such as cloud DVR (digital video recording) functionality were also initially missing, but would follow as AT&T’s TV propositions and functionalities iterated and improved over time.

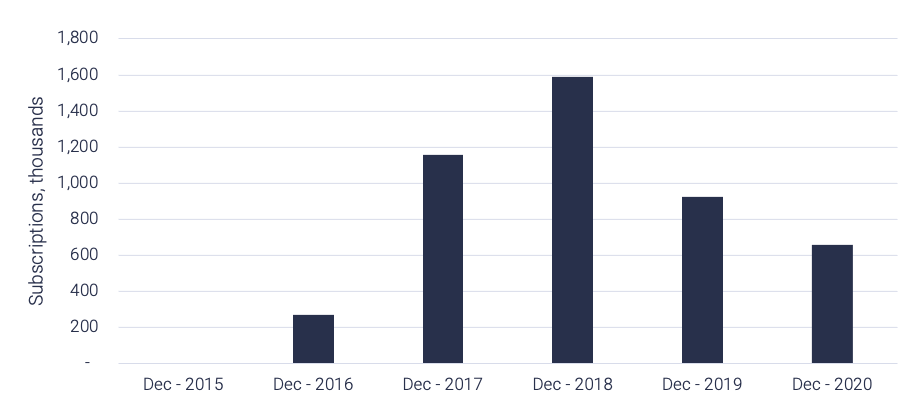

The DirecTV NOW streaming service enjoyed continuous quarterly growth through 2017 but peaked in Q3 2018 with net additions turning immediately negative in the final quarter of 2018 as management pulled back on costly promotions and discounted pricing.

The proposition became unsustainable financially in terms of its ability to cover rising programming costs and was positioned comparatively as a much less expensive service to its larger DirecTV satellite pay-TV propositions.

The DirecTV satellite service sold some of the most expensive TV propositions on the market and reported higher pay-TV ARPU ($131) than peers such as Dish ($89) and Comcast ($86) in Q4 2019.

- The launch of a $35 DirecTV NOW streaming service with no contract and with a similar sounding name to the full linear service confused both new and existing DirecTV satellite customers and some would have viewed their satellite package as expensive compared to the cheaper steaming option.

Rising programming costs

AT&T’s low-cost skinny TV packages brought them into direct confrontation with TV programmers in terms of negotiating fees for content. When the streaming service launched, analysts highlighted the channels within AT&T’s base package were expected to rise in price annually by around 10% each year and this would eventually require AT&T to eventually balance programming costs with rising monthly package pricing.

Confrontations with programmers included a three-week dispute with CBS and an eight week dispute with Nexstar in 2019, which resulted in a blackout of both CBS and Nexstar channels across AT&T’s TV platforms such as Direct TV, U-Verse, DirectTV NOW. Commenting on the blackouts in Q3 2019, Randall Stephenson noted there were “a couple of significant blackouts in terms of content, and those blackouts drove some sizable subscriber losses”.

AT&T’s confrontation with content owners may have been a contributory reason to consider acquiring a content creation platform of its own in the form of Time Warner.

In mid-2018, as AT&T withdrew promotions and discounts for DirecTV NOW (later rebranded it to AT&T TV NOW), customers began to drop the OTT TV service.

- AT&T TV NOW went from a peak of 1.86 million subscribers in Q3 2018 to 656,000 at the end of 2020.

DirecTV NOW subscriptions

Source: STL Partners, AT&T Q2 Earnings 2021

Name changes and new propositions create more confusion

Confusion amongst staff and customers

The new AT&T TV proposition confused not only customers but also AT&T staff, as they were found mixing up the AT&T TV proposition with the skinny AT&T TV NOW proposition. By 2019 the company diverted its attention away from AT&T TV NOW pulling back on promotional activity in order to focus on its core AT&T TV live TV service.

According to Cord Cutters News, both services used the same app but remained separate services. AT&T’s app store marketing incorrectly communicated the DirectTV NOW service was now AT&T TV when in fact it was AT&T TV NOW. Similarly, technical support was also incorrectly labelled with online navigation sending customers to the wrong support channels.

AT&T’s own customer facing teams misunderstood the new propositions

Source: Cord Cutters News

Withdrawal of AT&T TV NOW

By January 2021, AT&T TV NOW was no longer available to new customers but continued to be available to existing customers. The AT&T TV proposition, which was supposed to offer “more value and simplicity” was updated to include some features of the skinny bundle such as the option to go without an annual contract requirement. Customers were also not required to own the set-top box but could instead stream over Amazon Fire TV or Apple TV. In terms of pricing, AT&T TV was twice the price of the originally launched DirecTV NOW proposition costing $70 to $95 per month.

The short life of AT&T Watch TV

In April 2018, while giving testimony for AT&T’s merger with Time Warner, AT&T’s then CEO Randall Stephenson positioned AT&T Watch TV as a potential new low-cost service that would benefit consumers if the merger was successful. Days following AT&T’s merger approval in the courts, the low cost $15 per month, ultra-skinny bundle launched as a suitable low-cost cord-cutter/cord-never option for cable, broadband and mobile customers from any network. The service was also free to select AT&T Unlimited mobile customers.

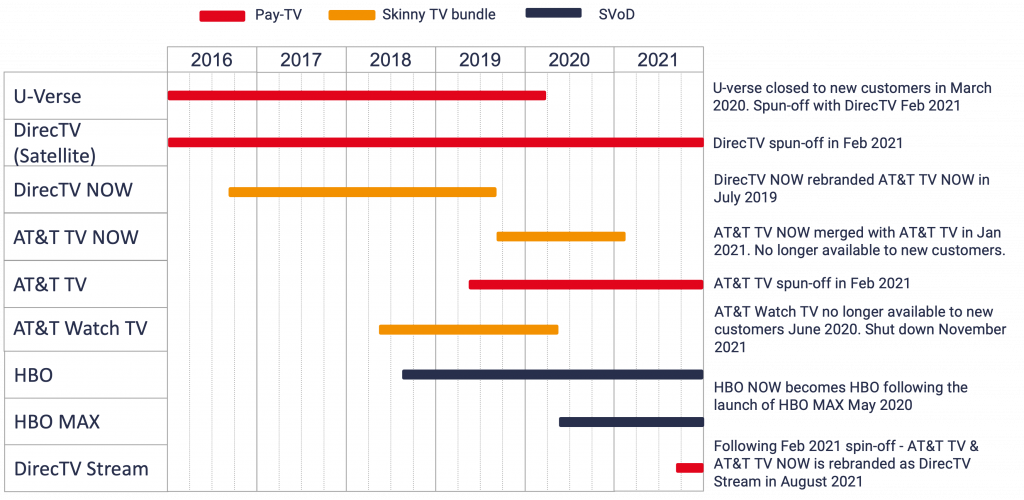

Timeline of AT&T entertainment propositions

Source: STL Partners

The decline of DirecTV

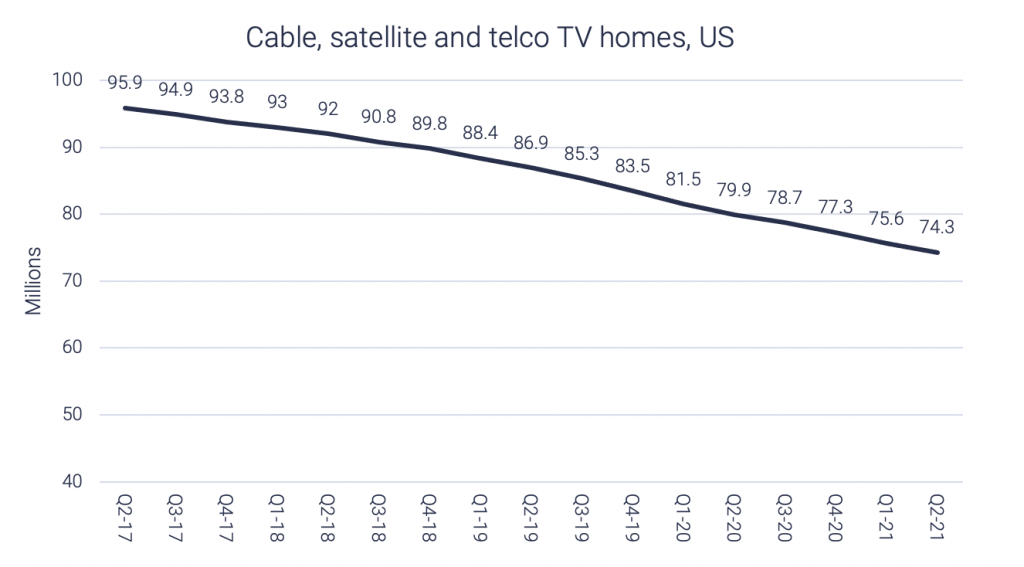

As the graphic belowshows, in June 2021 there were 74.3 million pay-TV households in the US, reflecting continued contraction of the traditional pay-TV market supplied by multichannel video programming distributor (MVPD) players such as cable, satellite, and telco operators. According to nScreenMedia, traditional pay-TV or MVPD market lost 6.3 and 6.2 million customers over 2019 and 2020, but not all were cord-cutters. Cord-shifters dropped their pay-TV but shifted across to virtual MVPD (vMVPD) propositions such as Hulu Live, Sling TV, YouTube TV, AT&T TV NOW, Fubo TV and Philo. Based on current 2021 cord-cutting levels, nScreenMedia predicts 2021 will be the highest year of cord-cutting yet.

Decline in traditional pay-TV households

Source: nScreenMedia, STL Partners

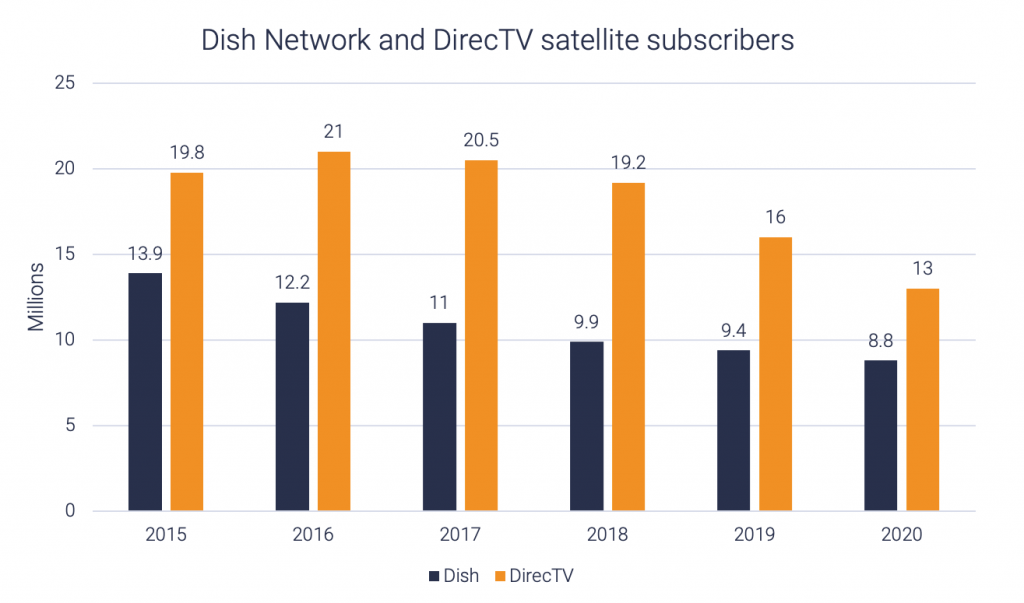

Satellite subscribers to Dish and DirecTV 2015-2020

Source: nScreenMedia, STL Partners

When considering AT&T’s management of DirecTV, nScreenMedia research shows the market number of MVPD subscribers declined by over 20 million between 2016 and 2020. In that time, DirecTV lost eight million subscribers. While it represented 20% of the MVPD market in 2016, DirecTV accounted for 40% of the pay-TV losses in the market (40% of 20 million equals ~8 million). AT&T’s satellite rival Dish weathered the decline in pay-TV slightly better over the period.

- In Q4 2020 the operator wrote down $15.5bn on its premium TV business, which included DirecTV decline, to reflect the cord cutting trend as customers found cheaper streaming alternatives online. The graphic (below) shows a loss of 8.76 million Premium TV subscribers between 2017 and 2020 with large losses of 3.4 million and 2.9 million subscribers in 2019 and 2020.

AT&T’s communications business has also been enduring losses in legacy voice and data (DSL) subscriptions in recent years. AT&T has used a bundling strategy for both products. As customers switched to AT&T fibre or competitor broadband offerings this also impacted the video subscription.

Table of contents

- Executive Summary

- What can others learn from AT&T’s experience?

- How AT&T entered and exited the media business

- AT&T enters the satellite market at its peak

- The beginnings of a bumpy journey in TV

- Vertical integration strategy: The culture clash

- AT&T’s telco mindset drives its video strategy

- HBO MAX performance

- The financial impact of AT&T’s investments

- Reversing six years of strategic change in three months

- Lessons from AT&T’s foray into media

Related Reports

Enter your details below to request an extract of the report