Login to access

Want to subscribe?

This article is part of: Executive Briefing Service

To find out more about how to join or access this report please contact us

As AI and national sovereignty increasingly intersect, telecoms operators face both opportunity and risk. This report sets out a practical framework to help telcos determine whether, where and how to play in sovereign AI.

Introduction: Defining the sovereign AI opportunity for telcos

AI is a profoundly transformative technology, with economic and societal implications that have pushed it to the top of national strategic agendas. Governments are motivated both by the opportunity to harness AI for productivity, competitiveness and public services, and by the risks that widespread adoption creates. Chief among these threats is growing dependency on foreign AI technology providers at a time that the established global order is undergoing upheaval. As a result, many countries are pursuing some form of “sovereign AI”, supported by policy intent, regulation and targeted funding.

This growing intersection between AI and sovereignty creates an opportunity for certain telecoms operators. Most telcos are nationally anchored organisations, owners and operators of critical infrastructure, and experienced in delivering highly regulated, resilient systems. Most importantly they are held accountable (and in some cases owned) by the national authorities. These attributes position them as natural enablers of sovereign AI infrastructure. However, sovereign intent does not automatically translate into sustainable commercial opportunity. Enterprise AI adoption is mostly at an early stage, global infrastructure players are well capitalised, and AI technologies continue to evolve faster than most enterprises can deploy them at scale, creating both opportunity and risk for operators.

Despite this uncertainty, telecoms operators cannot afford to remain on the sidelines in markets where credible demand signals for sovereign AI are emerging. Waiting for full clarity is not a viable strategy. By the time outcomes are certain, key ecosystem positions will already be occupied and the cost of late entry may be prohibitive for most operators and their shareholders. If sovereign AI develops at scale without meaningful telco participation, the risk is structural: operators are further marginalised into commoditised connectivity roles, excluded from higher-value AI infrastructure, platforms and services. This risk is compounded by the limited impact AI is likely to have on access traffic volumes, meaning telcos cannot count on AI-driven growth in their core connectivity businesses.

For telecoms operators in markets where sovereign AI demand is strong, the strategic question is less about whether to engage, and more about how, and how much, to do so. Given the fast-evolving nature of enterprise AI and national approaches to sovereignty, how should telecoms operators approach sovereign AI opportunities?

This report addresses that question. It introduces a structured framework to help operators assess domestic demand for sovereign AI, evaluate their right to win a share of that opportunity, and commit to a level of investment that secures a viable position in their emerging sovereign AI ecosystems. While this is a long-term journey and early moves may not deliver immediate returns, they preserve relevance, build critical capabilities and maintain strategic optionality. In a competitive market where waiting risks permanent exclusion, the priority is to be in the game.

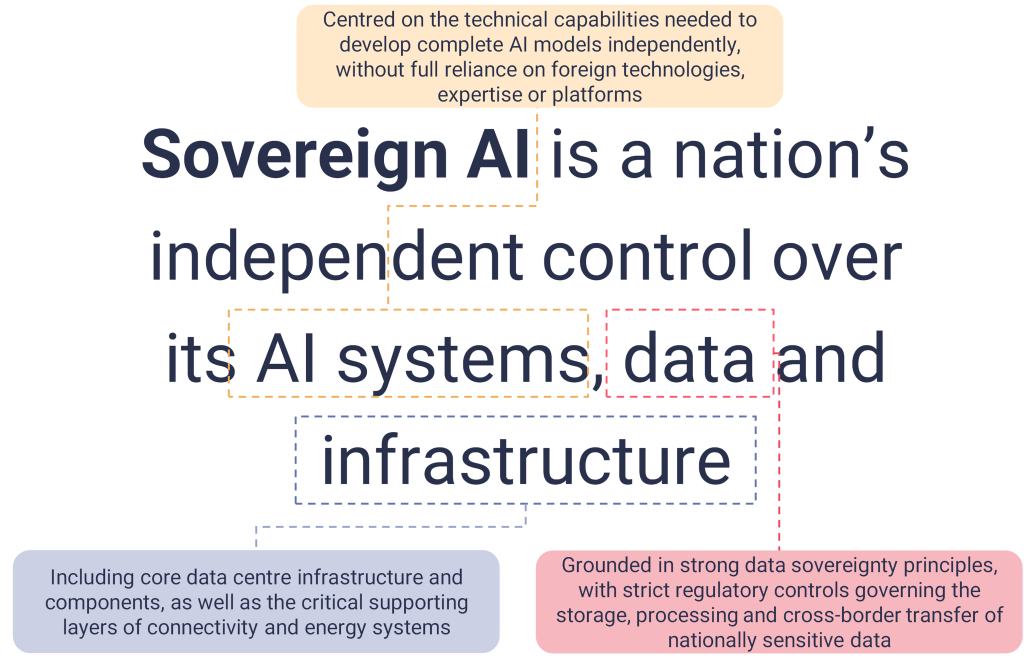

What is sovereign AI?

Source: STL Partners

In practice, sovereign AI spans three core dimensions:

1. AI systems: The technical capability to develop, govern, deploy and operate AI models without full or partial dependency and lock-in to technologies, expertise or platforms controlled by entities accountable to foreign jurisdictions.

2. Data: Data sovereignty principles governing the storage, processing and cross-border transfer of nationally sensitive, nationally protected personal or regulated data.

3. Infrastructure: Control over core data centre infrastructure and components, alongside the critical supporting layers of connectivity and energy systems required to operate AI at scale.

Beyond a policy objective, sovereign AI is increasingly emerging as a productised proposition. Governments and enterprises are seeking to encourage or mandate the adoption of commercial offerings that deliver one or more of these sovereignty dimensions. This report focuses on sovereign AI as a commercial and marketplace opportunity, expressed through distinct infrastructure, platform and service propositions that comply with sovereign AI principles.

This shift creates a significant opportunity for telecoms operators. As owners and operators of domestic digital infrastructure, and increasingly of AI compute and associated services, telcos are well positioned to act as foundational enablers of sovereign AI in their home markets.

If you are not a subscriber, enter your details below to download a free copy of the report

Table of contents

- Foreword

- Executive Summary

- Introduction: Defining the sovereign AI opportunity for telcos

- What is sovereign AI?

- Sovereign AI is coming into increasing focus as an opportunity

- Sovereign AI exists as a spectrum

- Telcos can lead in sovereign AI

- Sovereign AI is gaining traction with telecoms operators

- Partnerships underpin entry into sovereign AI

- Timing is important for telcos launching sovereign AI propositions

- The sovereign AI matrix: How to play?

- Understanding your positioning on the sovereign AI matrix: A step-by-step guide

- From sovereign AI strategy to execution

- Conclusion

Related research

- Agentic AI: Making operator data AI ready

- Telco generative AI adoption tracker

- Enterprise AI: What are the best opportunities for telcos?

- Enterprise AI: Practical steps for telcos to address customer needs