Login to access

Want to subscribe?

This article is part of: Consumer

To find out more about how to join or access this report please contact us

Driven in part by the COVID-19 pandemic, demand for both core broadband and value-added services is growing. This presents new challenges and opportunities for operators seeking growth “in the home”. However, traditional growth strategies, such as the triple play proposition, have reached maturity - telcos must therefore find new ways to drive sustained growth and stay relevant in the space.

Winning in the evolving “in home” consumer market

COVID-19 is accelerating significant and lasting changes in consumer behaviours as the majority of the population is being implored to stay at home. As a result, most people now work remotely and stay connected with colleagues, friends, and family via video conferencing. Consumer broadband and telco core services are therefore in extremely high demand and, coupled with the higher burden on the network, consumers have high expectations and dependencies on quality connectivity.

Furthermore, we found that people of all ages (including non-digital natives) are becoming more technically aware. This means they may be willing to purchase more services beyond core connectivity from their broadband provider. At the same time, their expectations on performance are rising. Consumers have a better understanding of the products on offer and, for example, expect Wi-Fi to deliver quoted broadband speeds throughout the house and not just in proximity to the router.

As a result of this changing landscape, there are opportunities, but also challenges that operators must overcome to better address consumers, stay relevant in the market, and win “in the home”.

This report looks at the different strategies telcos can pursue to win “in the home” and address the changing demands of consumers. It draws on an interview programme with eight operators, as well as a survey of more than 1100+ consumers globally . As well as canvassing consumers’ high level views of telcos and their services, the survey explores consumer willingness to buy cybersecurity services from telcos in some depth.

Enter your details below to download an extract of the report

With increasing technical maturity comes an increasingly demanding market

Consumers are increasing in technical maturity

The consumer market as a whole is becoming much more digital. Over the past decade there has been a big shift towards online and self-service models for B2C services (e.g. ecommerce, online banking, automated chatbots, video streaming). This reflects the advent of the Coordination Age – connecting people to machines, information, and things – and the growing technical maturity of the consumer market.

COVID-19 has been a recent, but significant, driver in pushing consumers towards a more digital age, forcing the use of video conferencing and contactless interactions. Even people who are not considered digitally native are becoming increasingly tech savvy and tech capable customers.

Cisco forecasts that, between 2018 and 2023, the number of Internet users globally will increase from 51% to 66% . It has also forecast an increase in data volumes per capita per month from 1.5GB in 2017 to 9.7GB in 2022 . Depending on the roll out of 5G in different markets, this number may increase significantly as demand for mobile data increases to meet the potential increases in supply.

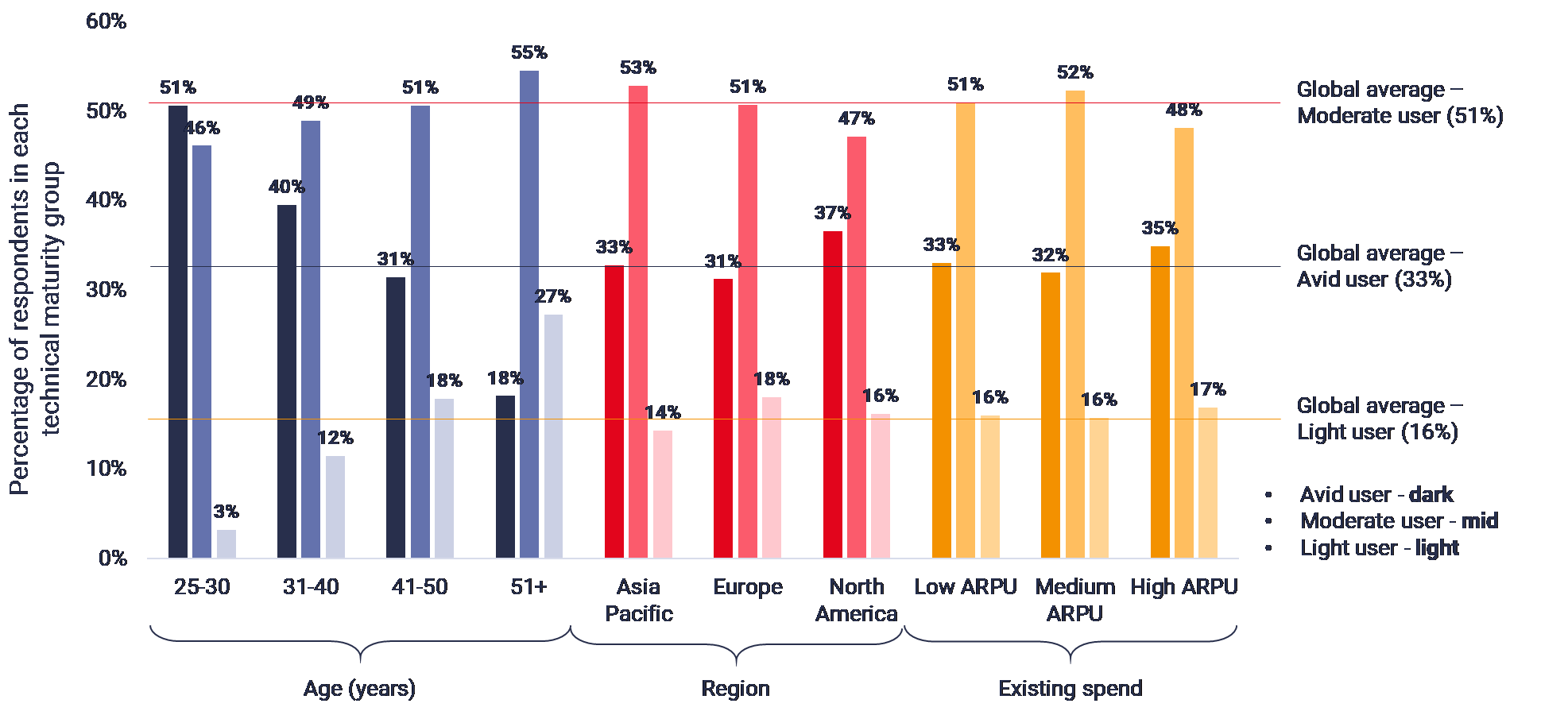

Furthermore, in our survey of 1,100+ consumers globally, 33% of respondents considered themselves avid users and 51% considered themselves moderate users of technology. Only 16% of the population felt they were light users, using technology only when essential for a limited number of use cases and needing significant support when purchasing and implementing new technology-based solutions.

Though this did not vary significantly by region or existing spend, it did vary (as would be expected) by age – 51% of respondents aged between 25 and 30 considered themselves avid users of technology, while only 18% of respondents over 50 said the same. Nevertheless, even within the 50+ segment, 55% considered themselves moderate users of technology.

Self-proclaimed technical maturity varies significantly by age

Source: STL Partners consumer survey analysis (n=1,131)

The growing technical maturity of consumers suggests a larger slice of the market will be ready and willing to adopt digital solutions from a telco, providing an opportunity for potential growth in the consumer market.

Consumers have higher expectations on telco services

Coupled with the increasing technical maturity comes an increase in consumer expectations. This makes the increasing technical maturity a double edged sword – more consumers will be ready to adopt more digital solutions but, with a better understanding of what’s on offer, they can also be more picky about what they receive and more demanding about performance levels that can be achieved.

An example of this is in home broadband. It is no longer sufficient to deliver quoted throughput speeds only within proximity to the router. A good Wi-Fi connection must now permeate throughout the house, so that high-quality video content and video calls can be streamed from any room without any drop in quality or connection. It must also be able to handle an increasing number of connected devices – Cisco forecasts an increase from a global average of 1.2 to 1.6 connections per person between 2018 and 2023 .

Consumers are also becoming increasingly impatient. In all walks of life, whether it be dating, technology or experiences, consumers want instant gratification. Additionally, with the faster network speeds of 4G+, fibre, and eventually 5G, consumers want (and are used to) continuous video feeds, seamless streaming, and near instant downloads – buffering should be a thing of the past.

One of our interviewees, a Northern European operator, commented: “Consumers are not willing to wait, they want everything here, now, immediately. Whether it is web browsing or video conferencing or video streaming, consumers are increasingly impatient”.

However, these demands extend beyond telco core services and connectivity. In the context of digital maturity, a Mediterranean operator noted “There is increasing demand for more specialized services…there is more of a demand on value-added, rather than core, services”.

This presents new challenges and opportunities for operators seeking growth “in the home”. Telcos need to find a way to address these changing demands to stay relevant and be successful in the consumer market.

Table of Contents

- Executive summary

- Introduction

- Growing demand for core broadband and value-added services

- COVID-19 is driving significant, and likely lasting, change

- With increasing technical maturity comes an increasingly demanding market

- Telcos need new ways to stay relevant in B2C

- The consumer market is both diverse and difficult to segment

- Should telcos be looking beyond the triple play?

- How can telcos differentiate in the consumer market?

- Differentiate through price

- Differentiate through new products beyond connectivity

- Differentiate through reliability of service

- Conclusions and key recommendations

- Appendices

- Appendix 1: Consumer segments used in the survey

- Appendix 2: Cybersecurity product bundles used in the conjoint analysis