How BT beat Apple and Google over 5 years

Over 5 years, BT Group’s share price has more than tripled, outperforming Apple’s and Google’s, while its revenues have shrunk. Why, and what can other telcos learn from its success?

Over 5 years, BT Group’s share price has more than tripled, outperforming Apple’s and Google’s, while its revenues have shrunk. Why, and what can other telcos learn from its success?

We believe that the global telecoms market is approaching a critical moment of change, as strategic drivers and enablers are combining to open the door to a fundamental shift in the industry. We show how and why with highlights of our recent research, and set the scene for a new vision for Telco 2.0 – what telcos should be in the future, and how to get there.

A primary benefit envisaged of 5G networks is that latency (i.e. delay times for users) will be massively reduced. This would deliver major benefits for many applications providing that the software for those cloud-based applications is located near enough to the users at the edge of the network. This is likely to drive a massive change in the architecture of the cloud and the network industries. This report outlines likely scenarios and identifies some early moves that are starting to play out now.

Cable operators are on the verge of a massive and remarkably easy capacity upgrade. Where it has begun, fixed incumbents are already being forced to deploy fibre. Gigabit WiFi is coming too, so mobile operators are very much concerned.

How will getting into the MVNO business help Google shore up its business model? We examine Google’s objectives, how it could price the service, and the implications for telcos and other players.

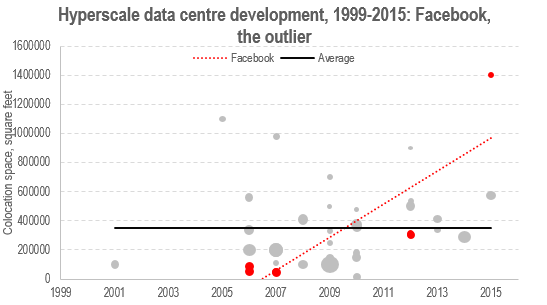

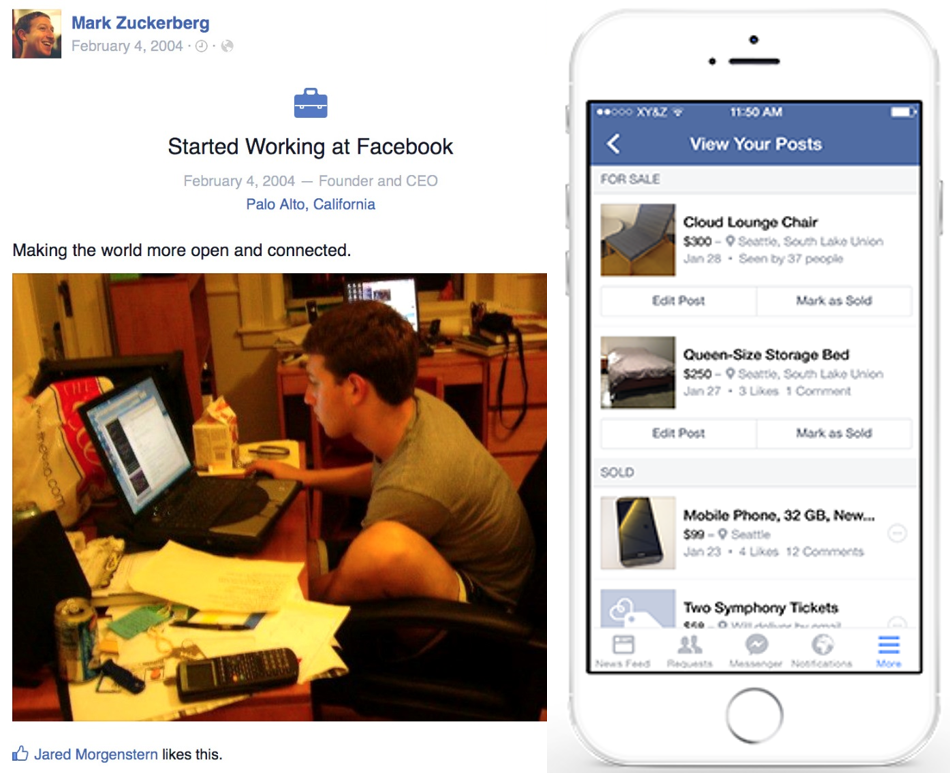

Facebook has changed substantially since we first analysed the company in 2011. In our latest major report we explore the accuracy of our 2011 predictions regarding users, revenue and strategy. We also examine Facebook’s current aspirations and challenges and explain why, where and how operators should be working with Facebook to build value.

Netflix’s success in the US and in Western Europe has demonstrated that consumers are willing to change how they watch and pay for TV and movies. As a result Netflix’s OTT proposition is challenging traditional pay TV models and changing how new broadband services are looking at content. For some players Netflix is a threat and for others an opportunity. So, how should content owners, channels, pay platforms and broadband providers respond?

STL Partners’ industry transformation analysis, including a recent global survey of telco executives, suggests operators’ digital ambitions are rising fast but, given 9 substantial implementation challenges, too little is currently being done to engender successful industry-wide business model transformation. We also look at the lessons from NTT DoCoMo, one of the operators that has made the most overall progress towards a ‘digital’ model.

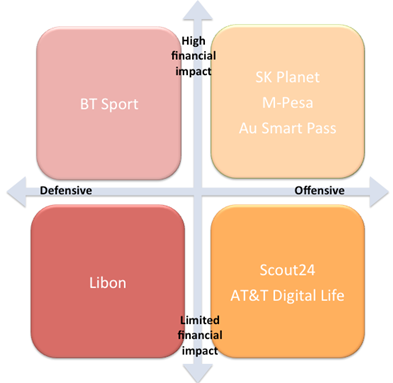

Although telcos aren’t generally associated with disruption, many operators around the world have attempted to disrupt adjacent markets, such as digital commerce, entertainment and financial services. In some cases, telcos have even disrupted their core broadband and communications markets. While many of these moves have fizzled out or have flown below investors’ radar screens, several have had a major impact on both the telco’s revenues and relevance. These include SK Planet, M-Pesa, Au Smart Pass and BT Sport. Why do some disruptive moves by telcos succeed and others fail?

What is disruption, when is it a good idea, and what do you do when it happens to you? We illustrate five principles of disruptive strategy based on our analysis of the telecoms and adjacent markets over the past eight years. The analysis covers both principles of creating and defending against disruption.

A small and surprising set of national operators are delivering outstanding performance in the challenging European market. Our analysis shows how they’re achieving differentiation with smart strategies that target the hottest customer need, and the considerable ramifications for the rest of the market.

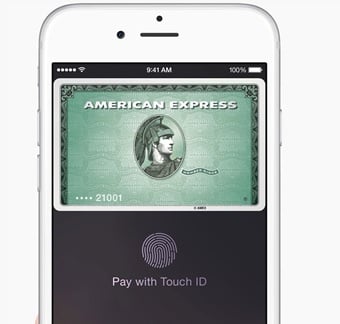

The unveiling of Apple Pay and unravelling of Weve (the UK operators’ payments venture) looked like bad news for telcos’ ambitions in mobile payments in some markets, and highlighted challenges to Google and others’ models. Yet there are already successful telco models and favourable market trends that telcos should exploit. So what are the opportunities now?

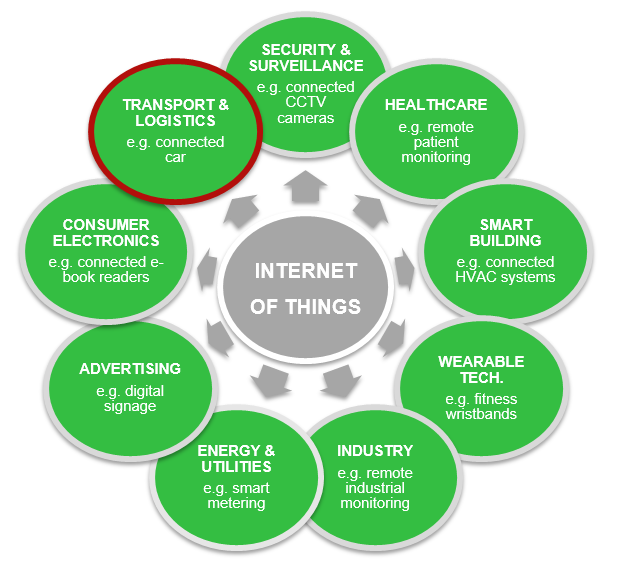

Connected cars are set to revolutionise the automotive industry as we know it, turning the car into the ‘ultimate mobile device’ and driving the growth of M2M in a big way. With Apple, Google, telcos and many others in the chase, we analyse the growth drivers, value chain, and key battles for control of this increasingly complex ecosystem, and outline a new connected car services framework.

Free’s shock bid for T-Mobile USA will stretch its finances and management capacity to the limit. Can Free’s package of tactics, technology, and procedures work in the US context?

Since Google acquired Nest for $3.2bn, Apple and Samsung have also entered the complex battle for the connected home. We analyse in-depth why Google wanted Nest, the players’ goals and strategies, and what should telcos and others do to stay in the game?

Facing lockout from a growing chunk of the Internet and mounting competition from the Facebook-Microsoft alliance and Amazon, Google’s core business is under intense pressure. The search giant’s response is to innovate, offering consumers proactive recommendations, as well as reactive search results. Once an interesting sideline, Google Now has become fundamental to the Mountain View company’s future. Is the suggestion service good enough to maintain Google’s position as the world’s leading big data company?

A launcher is a customizable home screen for an Android device that allows users to reorganize, customize and interact with their device. Launchers are gaining popularity, with Facebook, Google, Twitter and Yahoo all having either acquired or developed their own versions, but the market is fragmented with different launchers providing different functionality, services and monetization methods. Our latest analysis shows how telcos should seek to explore this area to help them establish more relevance in the digital ecosystem.