Login to access

Want to subscribe?

This article is part of: Edge Insights, Enterprise Platforms, Network Innovation

To find out more about how to join or access this report please contact us

Assuring networks, services and devices in the world of 5G, edge and IoT demands new capabilities in automation, AI and analytics (A3) at the edge of networks. This report sets out a roadmap for telco decision making around assurance tool creation, deployment and possible monetisation.

Why does edge assurance matter?

The assurance of telecoms networks is one of the most important application areas for analytics, automation and AI (A3) across telcos operations. In a previous report estimating the potential value of A3 across telcos’ core business, including networks, customer channels, sales and marketing, we estimated that service assurance accounts for nearly 10% of the total potential value of A3 (see the report A3 for telcos: Mapping the financial value). The only area of greater combined value was in resource management across telecoms existing networks and planned deployments.

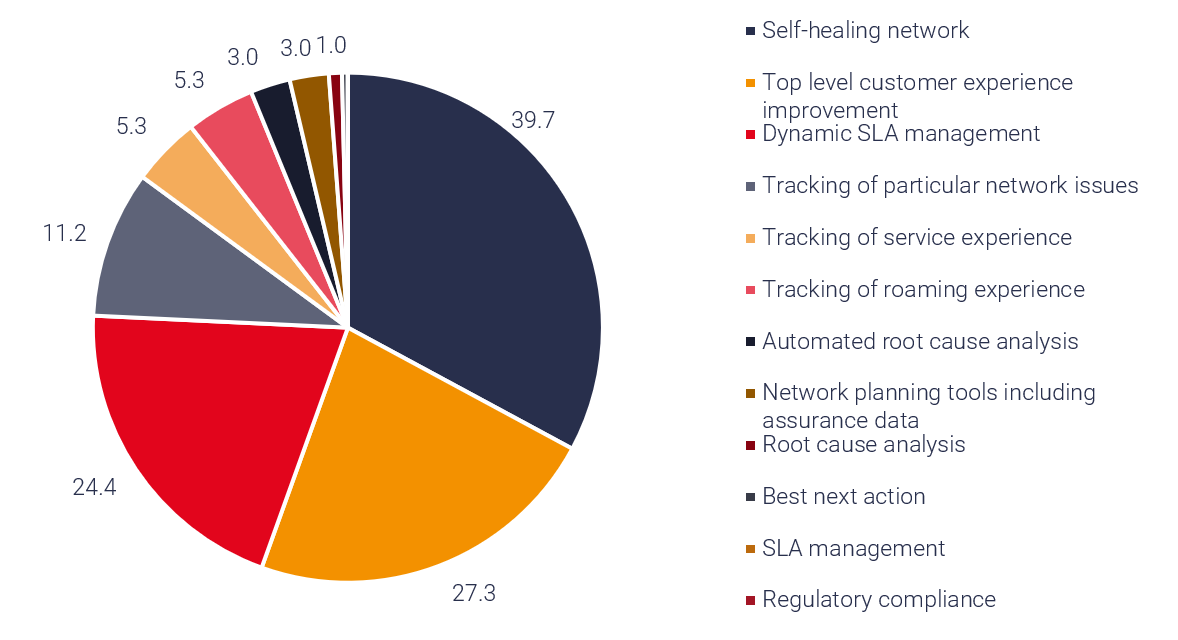

Within service assurance, the biggest value buckets are self-healing networks, impact on customer experience and churn, and dynamic SLA management. This estimate was developed through a bottom up analysis of specific applications for automation, analytics and AI within each segment, and their potential to deliver cost savings or revenue uplift for an average sized telecoms operator (see the original report for the full methodology).

Breakdown of the value of A3 in service assurance, US$ millions

Source: STL Partners, Charlotte Patrick Consult

While this previous research demonstrates there is significant value for telcos in improving assurance on their legacy networks, over the next five years edge assurance will become an increasingly important topic for operators.

What we mean by edge assurance is the new capabilities operators will require to enable visibility across much more distributed, cloud-based networks, and monitoring of a wider and more dynamic range of services and devices, in order to deliver high quality experience and self-healing networks. This need is driven by operators’ accelerating adoption of virtualisation and software-defined networking, for example with increasing experimentation and excitement around open RAN, as well as some operators’ ambitions to play a significant role in the edge computing market (see our report Telco edge computing: How to partner with hyperscalers for analysis of telcos’ ambitions in edge computing).

To give an idea of the scale of the challenge ahead of operators in assuring increasingly distributed network functions and infrastructure, STL Partners’ expects a Tier-1 operator will deploy more than 8,000 edge servers to support virtual RAN by 2025 (see Building telco edge infrastructure: MEC, private LTE and vRAN for the full forecasts).

Forecast of Tier 1 operator edge servers by domain

Source: STL Partners

Given this dramatic shift in network operations, without new edge assurance capabilities:

- A telco will not be able to understand where issues are occurring across the (virtualised) network and the underlying infrastructure, and diagnose the root cause

- The promises of cost saving and better customer experience from self-healing networks will not be fully realised in next-generation networks

- Potential revenue generators such as network slicing and URLLC will be of limited value to customers if the telco can’t offer sufficient SLAs on reliability, latency and visibility

- It will not be possible to make promises to ecosystem partners around service quality.

Despite the significant number of unknowns in the future of telco activities around 5G, IoT and edge computing, this research ventures a framework to allow telcos to plan for their future service assurance needs. The first section describes the drivers affecting telcos decision-making around the types of assurance that they need at the edge. The second sets out products and capabilities that will be required and types of assurance products that telcos could create and monetise.

Enter your details below to request an extract of the report

Table of contents

- Executive Summary

- The three main telco strategies in edge assurance

- What exactly do telcos need to assure?

- Why edge assurance matters

- Factors affecting edge assurance development

- What are telcos measuring?

- Internal assurance applications

- Location of measurement and analysis

- Ownership status of equipment and assets being assured

- Requirements of external assurance users

- Requirements from specific applications

- Telco business model

- The status of edge assurance and recommendations for telcos

- Edge assurance vendors

- Telco assurance products

- Appendix