Login to access

Want to subscribe?

This article is part of: Executive Briefing Service

To find out more about how to join or access this report please contact us

This is part 3 of a 3-part series taking an in-depth look at how 5G pioneers have evolved their approaches to commercialisation since launch, navigating a maze of factors such as handset availability, technology immaturity and more. What should others take from their experience to date?

Telstra: Maintaining its network leadership

SK Telecom, Verizon and Telstra were among the first in the world to start commercialising 5G networks. SK Telecom and Verizon launched broadband-based propositions in 2018, but it was only in 2019, when 5G smartphones became available, that consumer, business and enterprise customers were really able to experience the networks.

Part 3 of our 3-part series looks at Telstra’s 5G experience and how its propositions have developed from when 5G was launched to the current time. It includes an analysis of both consumer and business offerings promoted on Telstra’s website to identify the revenue streams that 5G is supporting now – as opposed to revenues that new 5G use cases might deliver in future. (We have covered this extensively for a number of verticals, including healthcare, manufacturing, energy, and transport and logistics.)

When its 5G network was launched, Telstra went to market with a 12-month free 5G access period and the intention to charge AUD15 ($12) at the conclusion of the free period. However at the end of the promotion period it opted to keep things simple for consumers, choosing to bundle 5G access with higher tier plans (effectively AUD65 / $50 and above) – and only offer 5G under its main Telstra brand. There were no 5G specific services at launch, however capacity advantages were leveraged to offer zero-rated access to subscription services available with the plan (i.e., subscription services would not consume data). From a customer standpoint the principal and most visible benefit from 5G in the early stages was its noticeably faster speeds.

This report examines the market factors that have enabled and constrained Telstra’s 5G monetisation efforts, as it moves to extend 5G access beyond premium early adopters to a wider audience. It identifies lessons in the commercialisation of 5G for those operators that are on their own 5G journeys and those that have yet to start.

Enter your details below to request an extract of the report

Telstra 5G performance to date

Given that four of the top five key purchase considerations for Australian customers (across consumer, small business and enterprise segments) are network-related (i.e., coverage, speed, reliability and security), Telstra has made network leadership a point of competitive differentiation. It views its investment in 5G as enabling it to stay ahead of customer network expectations as they evolve.

The operator was Australia’s 5G first-mover and it has been able to maintain its leadership in terms of 5G network coverage to date. This is a key deliverable of its T22 plan for transformation in response to challenging industry dynamics and the impact of the National Broadband Network (NBN) – the government’s broadband upgrade initiative.

In a market release on 21 April 2021, Telstra announced that its 5G network covered close to 66% of the Australian population and that it would attain its target of 75% coverage by the end of June 2021 (it achieved this goal on 28 June 2021). Telstra 5G sites number more than 3,700, across 200+ cities and towns, and 5G coverage extended to over 2,700 suburbs.

Post launch in 2019, early take-up of 5G devices was skewed towards consumer and SME segments, but the launch of Apple’s first 5G device in October 2020 helped promote 5G take-up in the enterprise segment (there has historically been a higher penetration of Apple devices in the Enterprise market).

- Early consumers were typically metro customers, which aligned to Telstra’s network rollout strategy (covering more populous/high traffic metro areas first).

- Enterprise customers were not among the early adopters of 5G devices.

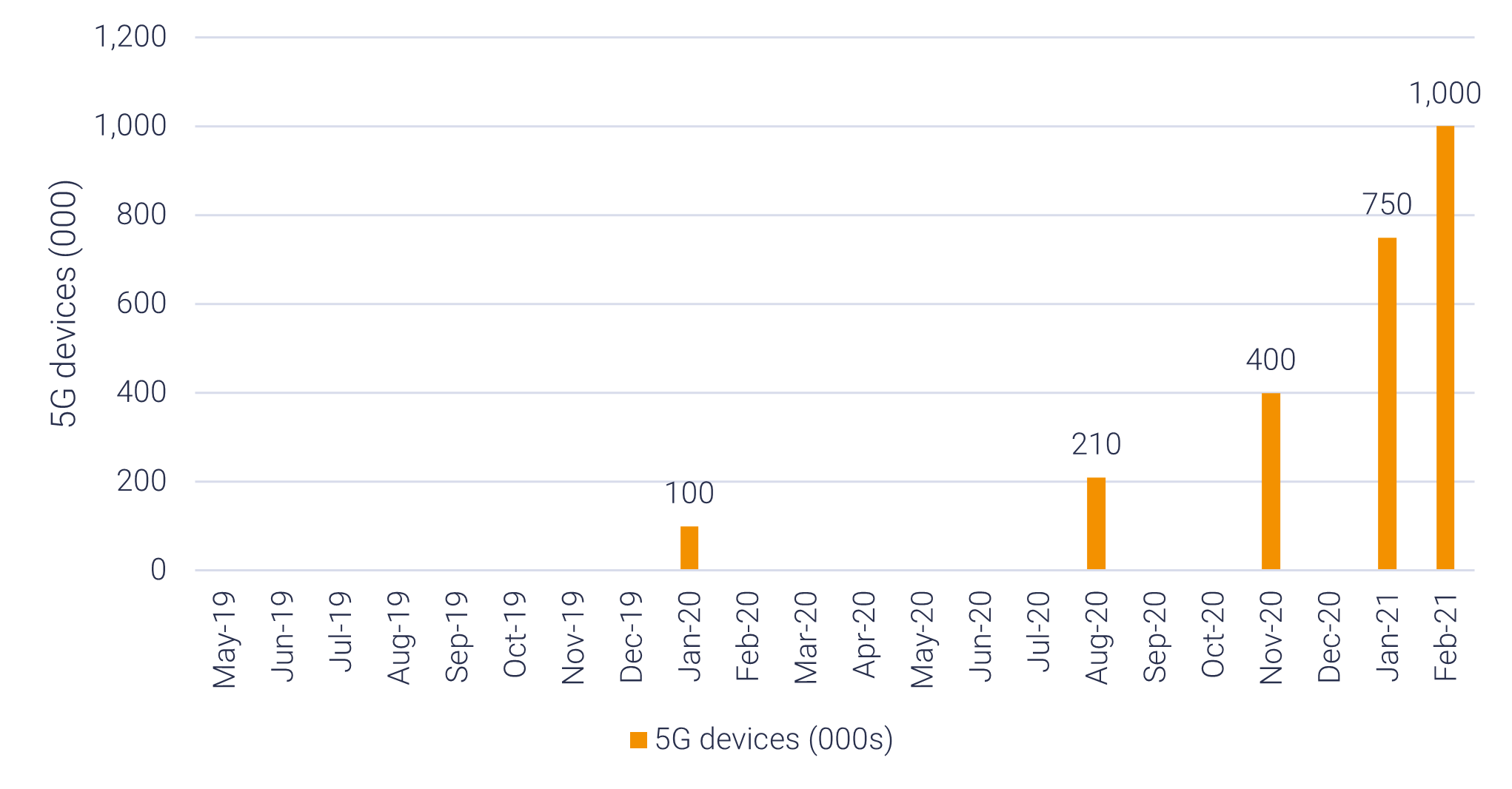

Net porting to the Telstra network was higher for 5G than for 4G for the first few quarters after launch and Telstra saw strong growth from its installed base (largely the early adopters). In August 2020, Telstra reported 210,000 5G devices connected to its network (before iPhone). The launch of iPhone 12 caused the number of 5G devices to jump to 400K by November 2020 (reported at Telstra’s November investors meeting), with 40K new 5G devices being added per week.

- 72% of 5G iPhones devices were on plans which included 5G access (i.e. top tier).

At the same meeting in November, Telstra reported that 65% of all new Android device sales were of 5G models (e.g. Oppo, Google, Motorola, Samsung), a factor attributed to getting handsets below the AUD1,000 ($771) threshold. This has helped to increase 5G readiness among its customer base.

By February 2021, the number of 5G devices on the Telstra network was over 1 million (this compares to 8.6 million postpay retail customers reported in December 2020, and 19 million customers overall). The share of devices on 5G plans is not public. Telstra continues to report that it is adding “thousands” of 5G devices to its network weekly.

5G devices connected to Telstra’s network since launch

Source: STL Partners based on Telstra public data

Telstra continues to see an increase in customer take-up of 5G-ready plans (new connections and upgrades). It attributes the increase in postpay service additions over the period to a leadership in 5G (supporting its network leadership perceptions), but also acknowledges that other non-network considerations, such as large data allowances may also be driving the uptake of these plans.

Telstra has reported an increase in the “transacting minimum monthly commitment” (TMMC) versus previous calendar period (PCP) for its postpay handheld customers for six months ending December 2020. TMMC is regarded as a lead indicator of ARPU trends (actual ARPU declined due to lost roaming revenue, new plan accounting which allocates more revenue to handsets, lost out-of-bundle revenue and other factors). Telstra regards some of the increase in TMMC as having been driven by the introduction of the latest model handsets. It noted a high attach rate for 5G inclusive plans – AUD65 and above plans – with iPhone 12 devices and the latest Samsung handsets that were introduced during the period (i.e., customers want 5G-ready plans with these new 5G handsets, not 5G access alone).

AUD ($) increase in TMMC on PCP for postpay handheld customers

Source: Telstra

Whilst the initial most obvious benefits of 5G relate to speed, Telstra assumes a broader perspective of 5G’s success metrics, including a comparison of overall NPS which has been consistently higher for customers on 5G plans than for those on 4G plans. There could be a number of reasons for this, aside from better network performance, e.g.:

- Positive associations with having something “new”;

- A positive effect as a result of iPhone ownership (though Telstra has noticed that the positive trend started before the iPhone launch);

- Post-purchase rationalisation;

- Richer device capabilities.

Telstra continues to monitor this trend to determine if it will be maintained.

Contents

- Executive Summary

- Introduction

- Performance indicators to date

- Details of launch

- Consumer propositions

- At launch…

- …And now

- Consumer monetisation summary

- Business propositions

- At launch…

- …And now

- Business monetisation summary

- Analysis of 5G market developments

- What next?

- Conclusions

- Index

- Appendix 1

This report builds on earlier STL Partners research, including:

- Verizon’s journey in commercialising 5G

- SK Telecom’s journey in commercialising 5G

- Monetising 5G with consumers: What are the options?

- 5G strategies: Lessons from the early movers