New MVNOs: Challenger brands and lessons from the UK market

Disruptors from other industries are turning their attention to the mobile market. They can learn from the vibrant UK MVNO market.

Disruptors from other industries are turning their attention to the mobile market. They can learn from the vibrant UK MVNO market.

This report presents quantitative analysis of the global demand for private networks over a 7-year period. We explore the revenue trends across the value chain and provide insights into different deployment models and technologies across 14 verticals.

Edge computing is a key enabling technology for AI and GenAI applications, providing the local processing power and low-latency connectivity needed for real-time decision-making and data processing. This report looks at the trends in investments in edge computing companies – from edge data centres to platforms and applications – and the market outlook for 2025.

The market for edge IoT presents a significant opportunity for technology solution providers but has yet to reach its full potential. In this report, we present the results from a four-part research series conducted in partnership with Volt Active Data, focusing on how to capture this value. This report addresses critical aspects such as the technical challenges, ecosystem dynamics and ultimately, the pathway to monetisation for edge IoT solutions.

As society becomes ever more dependent on connectivity, telcos face a growing risk of being regulated like traditional utility companies. This report details how operators can avoid falling into “the utility trap” and drive growth in the next decade.

This report presents quantitative analysis of the global demand for private networks over a 7-year period. We explore the revenue trends across the value chain and provide insights into different deployment models and technologies across 14 verticals.

The utilities sector is a promising opportunity area for private LTE and 5G networks. But it is not an easy one for telcos to address, as utility companies often deploy and manage networking technology in-house or via specialist service providers to satisfy service requirements. This report examines the sector realities.

Telecoms is too important to leave up to traditional fixed and mobile operators. Thanks to the “democratisation” of shared spectrum, virtualised networks, fibre and cloud – plus the demands of industry, government and local communities – a plethora of new service providers are emerging to fill the gaps. This report is intended as a “spotter’s guide” to the categories of network owners and operators.

We spoke to Telefónica about its 10 year experience of building a data monetisation business (previously called LUCA). This deep dive into its strategy, organisational structure and the products developed highlights what it takes to succeed in this challenging market.

As analytics, AI and automation (A3) technologies mature, we explore nine potential A3 capabilities telcos could offer to their enterprise customers. We identify the sweet spots for telcos by assessing the importance of each of the nine capabilities across 14 industry verticals and mapping them against telcos’ existing levels of expertise.

It has been six years since telcos began introducing data and analytics products into their portfolio of enterprise services. This report assesses the potential value of data monetisation across 13 verticals, and by type of data analytics product.

Telcos are looking towards the enterprise market to make the business case for 5G. But for most industries, 5G is just one of many technologies needed to drive efficiency and innovation. Which verticals’ needs best match telcos’ capabilities?

We outline three potential roles for telcos in the IoT, describing twelve potential application areas and forty use cases, as well as the structure and trends driving change. Looking beyond this we ask which market areas are most attractive, and what should telcos do within them?

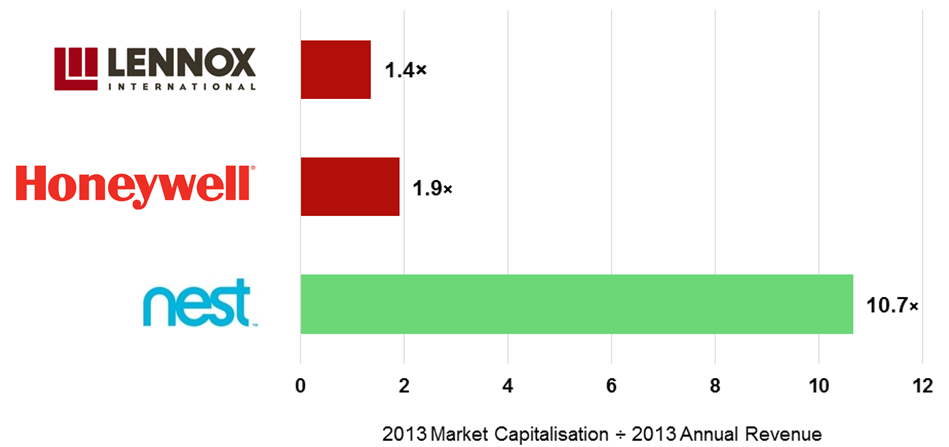

Since Google acquired Nest for $3.2bn, Apple and Samsung have also entered the complex battle for the connected home. We analyse in-depth why Google wanted Nest, the players’ goals and strategies, and what should telcos and others do to stay in the game?