Telco edge computing: Turning vision into practice

Telcos are well-placed to take advantage of the edge computing opportunity. In this report, we dive into the questions and challenges they face and how they can overcome these to succeed.

Telcos are well-placed to take advantage of the edge computing opportunity. In this report, we dive into the questions and challenges they face and how they can overcome these to succeed.

All telcos know they need to change. We believe the defining characteristic of those that will grow most is a clear focus on where and how they can create value beyond connectivity. This report lays out the two viable paths forward, and six steps all telcos must take in this new version of the Telco 2.0 vision.

Can the partnership between Google and telcos strike the balance between interoperability and speed of development needed to challenge Facebook and Tencent in conversational commerce?

What the leading on-demand entertainment specialists – Netflix and Spotify – will need to do the mount a serious challenge to GAFA in the top tier of Internet platforms and how telcos can help them make the online world more competitive.

Most telcos have now accepted that they need to offer more than connectivity if they want to move up the IoT value chain. This report presents a four-step framework to help telcos define a successful IoT strategy.

Telcos can draw ten lessons around organisational structure, strategy and staying relevant with customers from AccorHotels’ rapid digital transformation. This is the second in our series of transformation case studies from outside the telecoms sector.

Veon (rebranded VimpelCom) has embarked upon a bold strategy, shedding its network to move from being a traditional telco business to an agile consumer IP communications platform. We analyse its new strategy, its risks, and what it will need to do to succeed.

Healthcare is an attractive vertical for telcos to address with digital solutions, given the sector’s low digital base and rising demand for healthcare services from ageing populations and changing lifestyles. Although many telcos have made attempts to capture this opportunity through telehealth or consumer wellness services, TELUS stands out as an example of the value of a long-term commitment to healthcare. In this case study, we examine TELUS’ strategy in health, evidence of its success, and draw out lessons for other telcos.

Our latest adjacent market case study analyses Axel Springer’s successful 10 year digital transformation from print to online publisher, and holds many lessons for telcos, not least of which are the pitfalls of under commitment, and the required level of investment in M&A.

Dialog Axiata in Sri Lanka has developed a fast growing API platform that engages developers significantly more than plays by big telcos like AT&T, Orange and Vodafone relative to its scale. How has it achieved this and driven monetisation, innovation and efficiency within the company? And what is next?

The last few years have seen attempts by many leading telecoms operators to refresh their business model and generate new sources of growth and value. Now many digital initiatives are being scaled back. Telefonica and Telenor, two companies in the vanguard of the ‘drive to digital’ have both disbanded their digital organisations. In the first of two reports, STL Partners explores why efforts to yoke platform and product innovation businesses to a traditional infrastructure business have proved so difficult. The financial and operational constraints associated with traditional telecoms – particularly the need for long investment cycles in ‘one-function’ infrastructure – have made achieving the switch to ‘agile digital innovation’ all but impossible. But all that may be about to change and the future could be a little brighter.

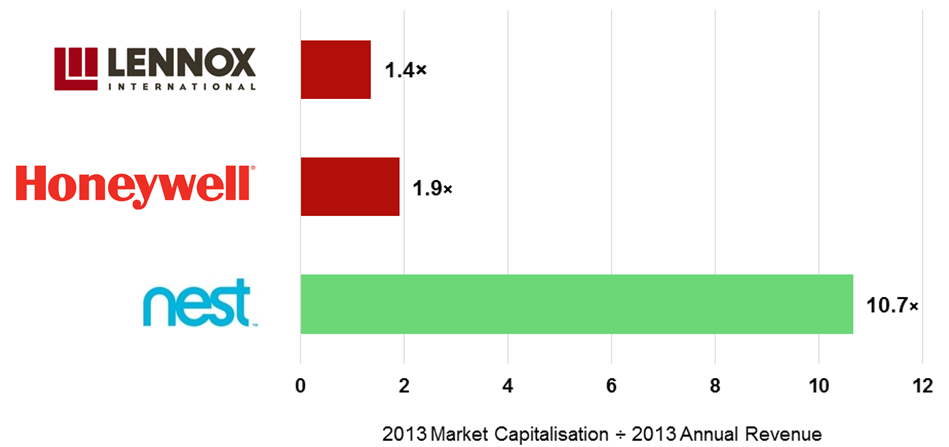

Since Google acquired Nest for $3.2bn, Apple and Samsung have also entered the complex battle for the connected home. We analyse in-depth why Google wanted Nest, the players’ goals and strategies, and what should telcos and others do to stay in the game?

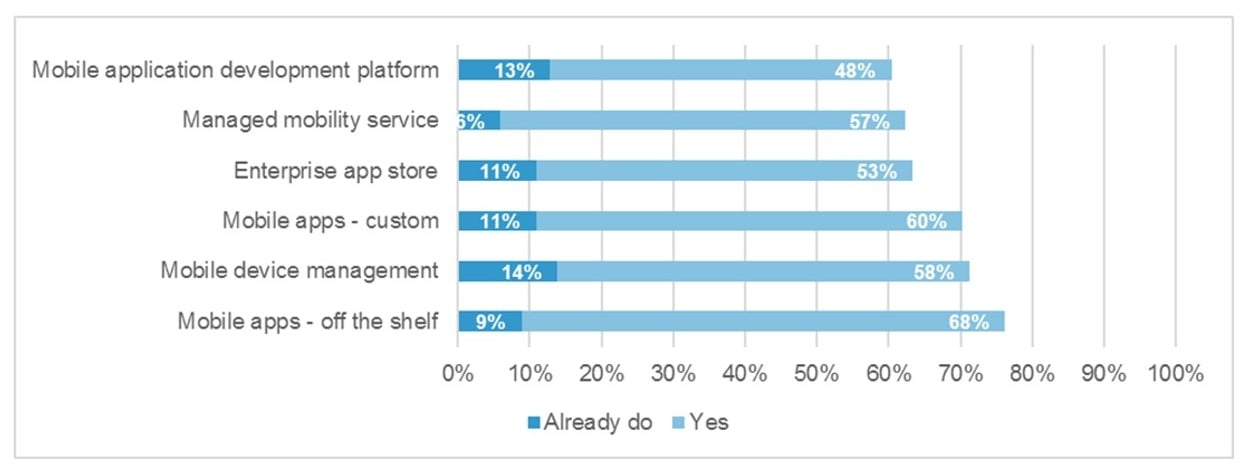

Our new global research among enterprises and telcos shows that many telcos are ideally positioned, but underprepared, to exploit the fast emerging and evolving $50bn Enterprise Mobility opportunity. How can telcos address this gap?

Enterprises are turning to mobility to transform their operations, creating a c.$50bn ‘Enterprise Mobility’ opportunity globally. There are four levels of engagement that telcos can adopt to start to capture a share of this market, and upgrade and repurpose their internal capabilities to deliver repeatable, high volume, customer-facing growth initiatives. They need tools, technologies and partnerships to provide the deep industry knowledge and mobile workforce expertise. This will allow them to take a defined proposition to market and evolve from being “just another channel” to originators and owners of intellectual property. (December 2013, Foundation 2.0, Executive Briefing Service, Cloud and Enterprise ICT Stream).

Enterprise Mobility Framework December 2013

Telco 2.0 presents a new strategy report examining the evolution of cloud services; the current opportunities for vendors and Telcos in the Cloud market, plus a penetrating analysis on the positioning Telcos need to adapt in order to take advantage of the potential $200Bn global Cloud services market. This report offers over 140 pages of insightful commentary from those who’ve been working at the cutting edge, and includes an introduction to the sector’s key technologies and emerging trends, as well as detailed recommendations for Telcos and vendors. (December 2012, Strategy Report, Cloud and Enterprise ICT Stream.)

Cloud Strategy Report Image

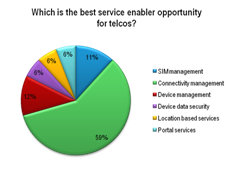

Our latest report on M2M 2.0 covers: M2M market growth, structure and dynamics; business models; the best role(s) for telcos; and leading thinking from Deutsche Telekom, Vodafone, Telenor, KPN and Swisscom. It describes how ‘Service Enablers’ are key to the telco opportunity in M2M in addition to connectivity. (July 2011, Executive Briefing Service)

M2M Pie Chart Service Enablers July 2011