Cloud gaming: New opportunities for telcos?

How telcos should be preparing for the seismic shift in the video games market signposted by Google’s new Stadia cloud gaming service.

How telcos should be preparing for the seismic shift in the video games market signposted by Google’s new Stadia cloud gaming service.

Successful innovation for telcos is important but has proved elusive. We look at some successes and more failures to draw out the common factors required for innovation to succeed.

How AT&T, Deutsche Telekom and Orange are taking on GAFA (Google, Amazon, Facebook and Apple) in the fast-growing smart home market.

Recently, Orange passed 22 million homes, Telefónica 20 million, and AT&T is now reaching five million more every year. The Chinese have over 300 million FTTH connections. What does FTTH do for ARPU, churn, OPEX and 5G that makes it so compelling?

The Consumer Internet of Things (IoT) market could be huge, but hasn’t yet taken off. We look at why, analysing leading telcos’ and others strategies to date (including DTAG, Orange, and Telefonica), and outline a strategy for how telcos could play a major role by solving some of the key problems.

We outline three potential roles for telcos in the IoT, describing twelve potential application areas and forty use cases, as well as the structure and trends driving change. Looking beyond this we ask which market areas are most attractive, and what should telcos do within them?

There is no excerpt because this is a protected post.

This report provides detailed analysis of the IoT ecosystem, the technologies enabling it, and how telcos can establish themselves within it, by presenting case-studies of strategies from AT&T, Vodafone, SK Telecom, and Deutsche Telekom. The report also discusses the connectivity needs of several different IoT use-cases.

The last few years have seen attempts by many leading telecoms operators to refresh their business model and generate new sources of growth and value. Now many digital initiatives are being scaled back. Telefonica and Telenor, two companies in the vanguard of the ‘drive to digital’ have both disbanded their digital organisations. In the first of two reports, STL Partners explores why efforts to yoke platform and product innovation businesses to a traditional infrastructure business have proved so difficult. The financial and operational constraints associated with traditional telecoms – particularly the need for long investment cycles in ‘one-function’ infrastructure – have made achieving the switch to ‘agile digital innovation’ all but impossible. But all that may be about to change and the future could be a little brighter.

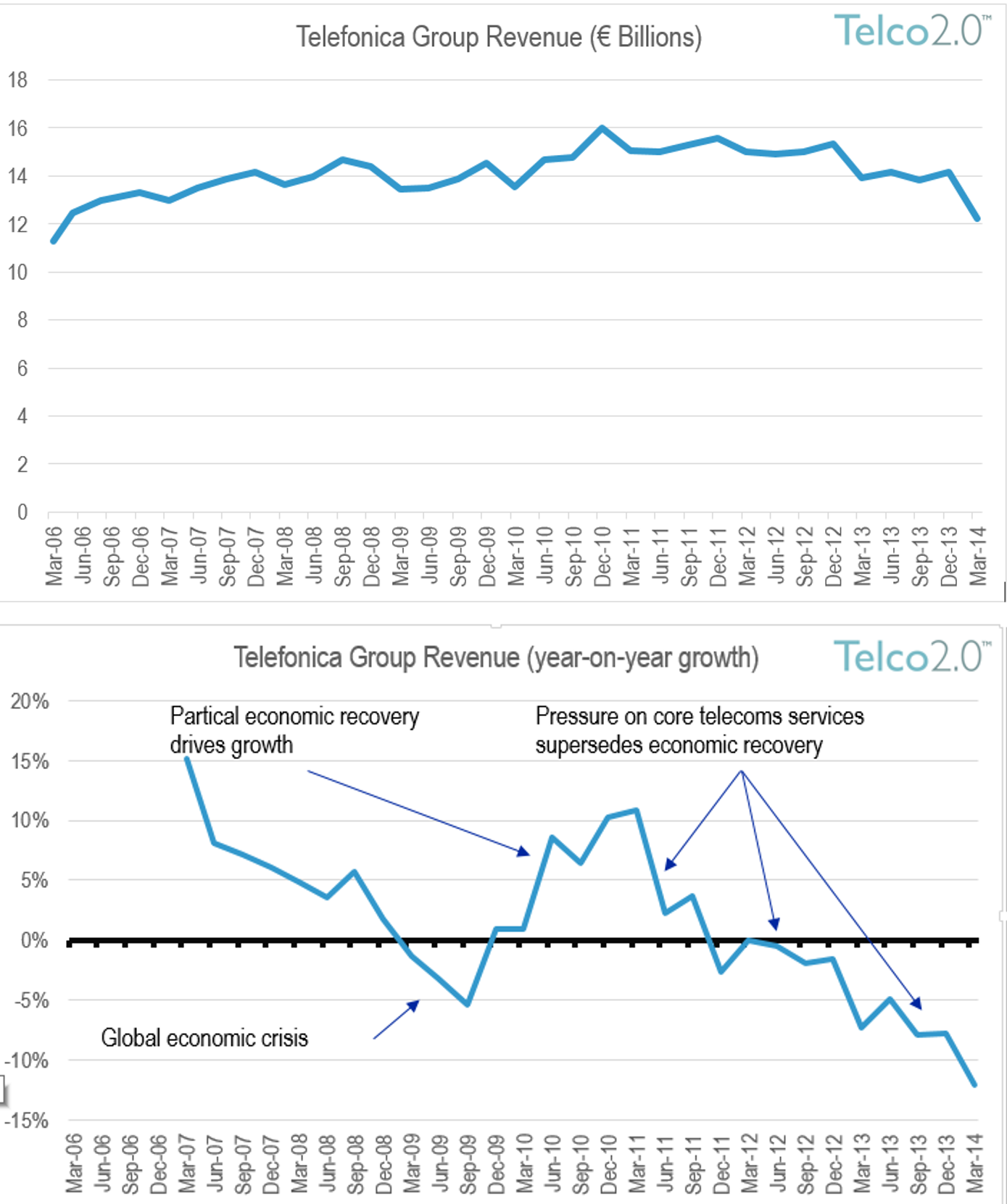

The latest results for Telefonica are grim, showing a 12% y-o-y revenue decline, following Orange and Deutsche Telekom’s 4% drops. This signals unequivocally that transformation is now a necessity not a luxury for European operators – and the rest of the world is not far behind. Longer term recovery is possible but not a certainty – what are the key steps? (May 2014, Foundation 2.0, Executive Briefing Service, Telco 2.0 Transformation Stream.)

Enterprise Mobility Framework December 2013

Albeit pioneering, Telefonica’s Digital business unit as was lacked focus and combined too many clashing cultures and incompatible businesses. Our latest analysis sees the change as ‘the end of the beginning’ for Telefonica’s Telco 2.0 services, and summarises lessons for all players implementing strategic transformation.

Telcos, Internet and technology players, banks and payment networks have disruptive $billion opportunities to act as intermediaries / enablers in mobile commerce and personal cloud services, based on the appropriate use of customer data. This report is a unique and comprehensive strategic guide for success in these roles. It analyses the strategies of the main and cutting-edge players, and outlines key success factors in designing and delivering customer propositions, technology, organisation and value network strategies. It also includes evaluations of the related strategic opportunities of ‘raw big data’, professional data services, and internal data use, and a business model showing how one type of candidate for the intermediary role, a telco, could grow profitable new revenues equivalent to c.$50Bn (5% of existing core revenues) within five years. (October 2013, Dealing with Dsiruption Stream). Telco 2.0 Transformation Index Small

Opportunities exist for operators to support third-party businesses in Customer Profiling, Marketing offers, ID & Authentication, Network QoS, and Billing, Payments & Collection. However, our in-depth research among senior execs in ‘upstream’ industries (e.g. retail, media, IT, etc.) and telcos shows that poor communication of the telecoms value proposition and slow implementation by operators is frustrating upstream customers and operators alike. Our independent new analysis (kindly sponsored by Openet) identifies strategic customer segments for telcos building new ‘Telco 2.0’ business models, key obstacles to overcome, six real-world implementation strategy scenarios, and strategic recommendations for telcos. (April 2012, Executive Briefing Service, Transformation Stream.)

Google’s Advertising Revenues Cascade

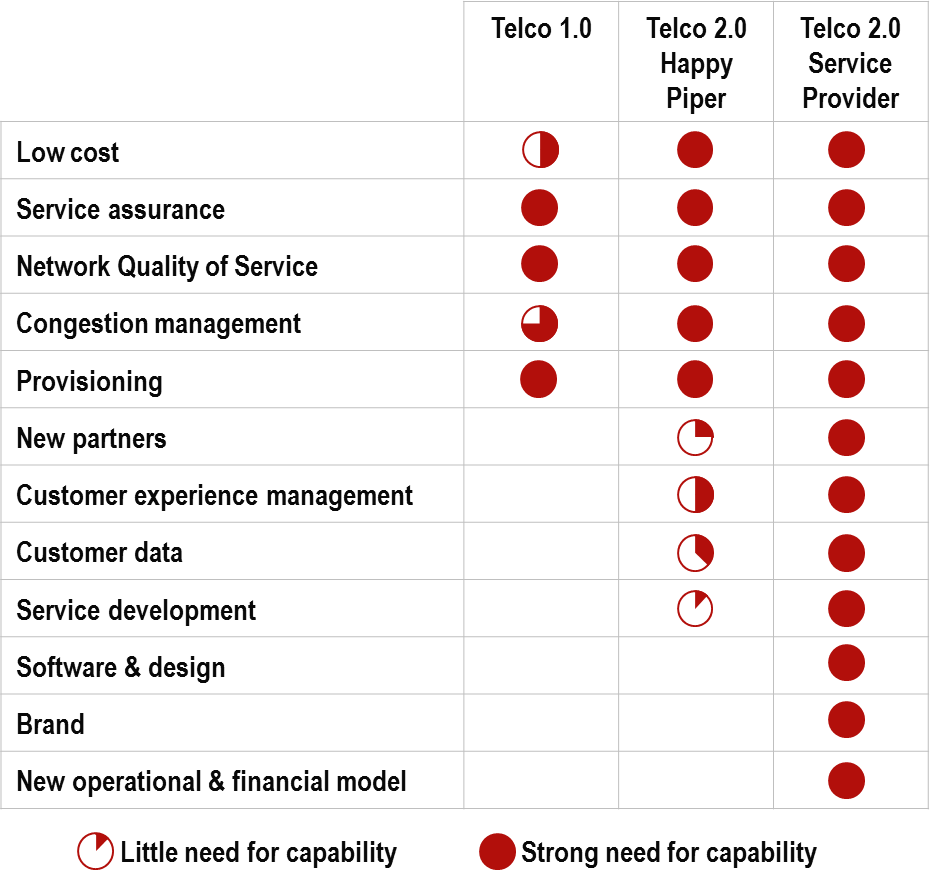

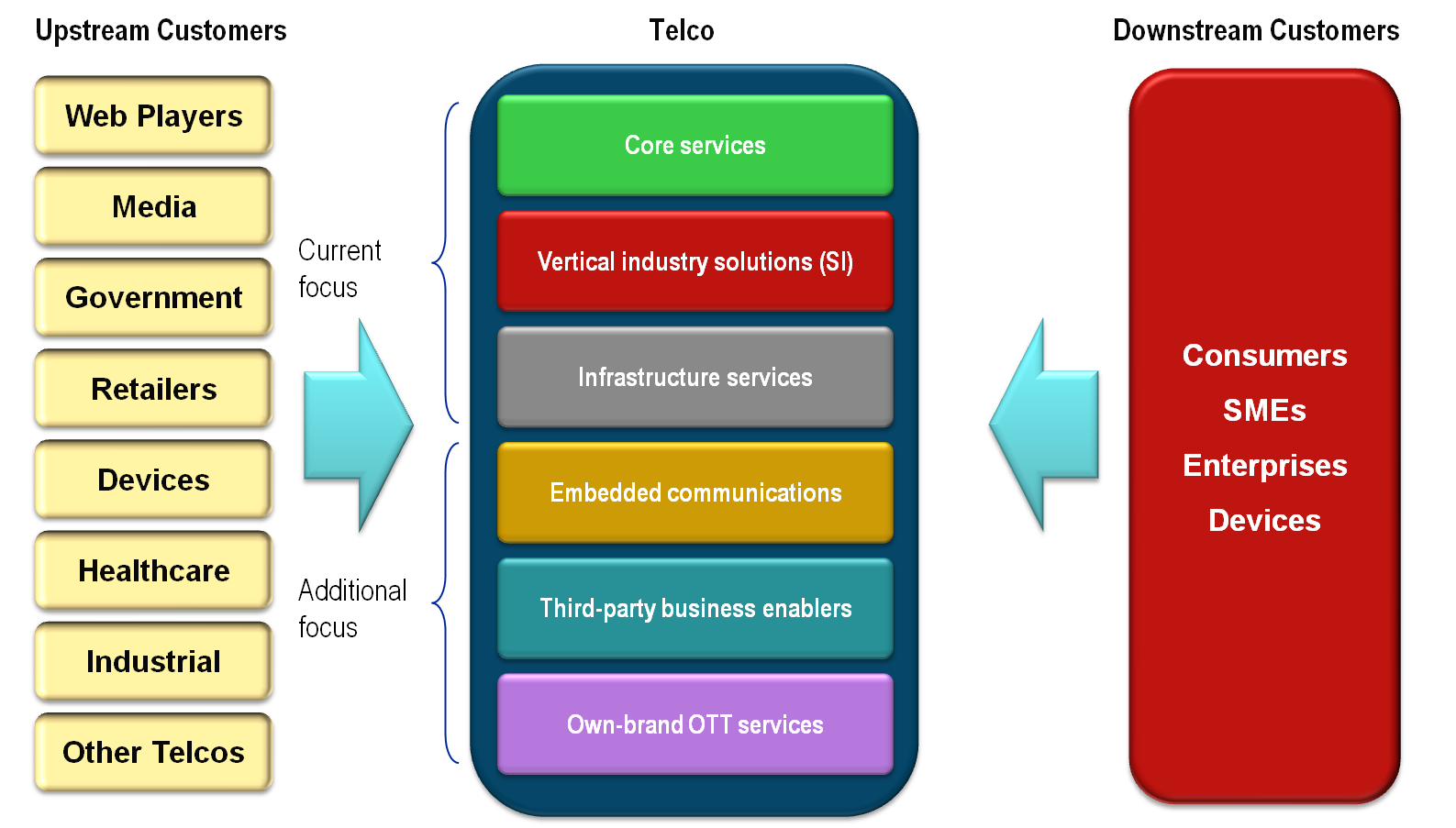

A summary of the six Telco 2.0 opportunities to transform telco’s business models for success in an IP-based, post PSTN world: Core Services, Vertical Solutions, Infrastructure Services, Embedded Communications, 3rd Party Enablers, and Own Brand OTT Services. It includes an extract from the Roadmap to New Telco 2.0 Business Models, updates on latest developments, and feedback from over 500 senior TMT industry execs. (July 2011, Executive Briefing Service, Transformation Stream).

Telco 2.0 Six Key Opportunity Types Chart July 2011

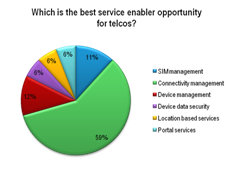

Our latest report on M2M 2.0 covers: M2M market growth, structure and dynamics; business models; the best role(s) for telcos; and leading thinking from Deutsche Telekom, Vodafone, Telenor, KPN and Swisscom. It describes how ‘Service Enablers’ are key to the telco opportunity in M2M in addition to connectivity. (July 2011, Executive Briefing Service)

M2M Pie Chart Service Enablers July 2011

Innovation appears to be flourishing in mobile broadband. At the Telco 2.0 EMEA Executive Brainstorm earlier this month we saw working applications that enable a.) users to monitor and control their network usage and services and b.) operators to support ‘dynamic pricing’. Despite growing enthusiasm for LTE, delegates considered offloading traffic and network sharing strategies as at least as effective in managing costs. (May 2011, Executive Briefing Service, Future of the Networks Stream) Mobile Broadband Fuel Gauge

This Strategy Report plots the transformational path that telcos need to follow to achieve the $375Bn p.a. ‘Telco 2.0’ opportunities. It describes the six growth opportunity areas for the Telecoms industry, identifies new categories of operators, benchmarks the primary strategies needed by each to evolve and thrive in the new industry environment, and highlights leading examples of telco business model innovation. It has 284 pages, including a 13 page Executive Summary and a detailed index. (April 2011, Telco 2.0 Transformation Stream) The Roadmap to new Telco 2.0 Business Models