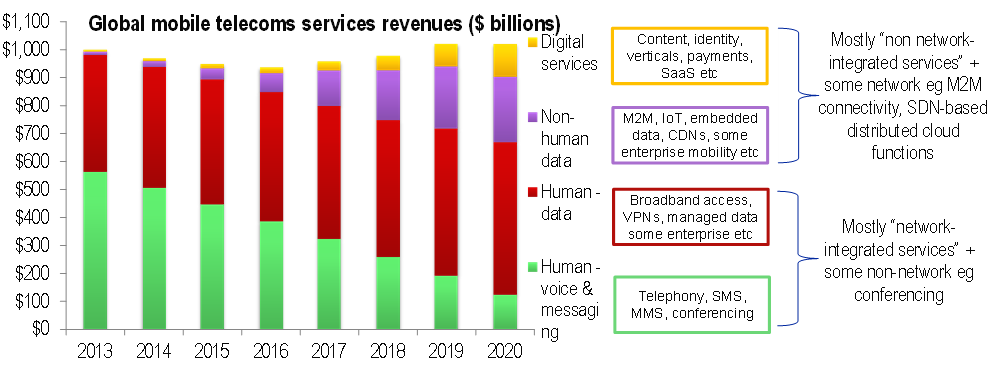

The network is one of telcos’ key assets. The case for investing in it was once straightforward: the bigger and faster the better. Yet today, many forces are combining to cloud that picture, such as virtualisation, regulation, the success of Internet services, network sharing, market consolidation and in some cases saturation, to name a few. To kick off our ‘Future of the Network’ research stream, we outline the key questions determining future investments in the network and our forthcoming work to address them. In Part 2, we’ll outline the key disruptive forces on the network.