Login to access

Want to subscribe?

This article is part of: Edge Insights

To find out more about how to join or access this report please contact us

STL Partners takes stock of the development of the edge computing ecosystem over the past five years, how AI has now reshaped the landscape and proposes its view on the future outlook of the market: including the likely winners and losers.

AI is reshaping the edge computing landscape

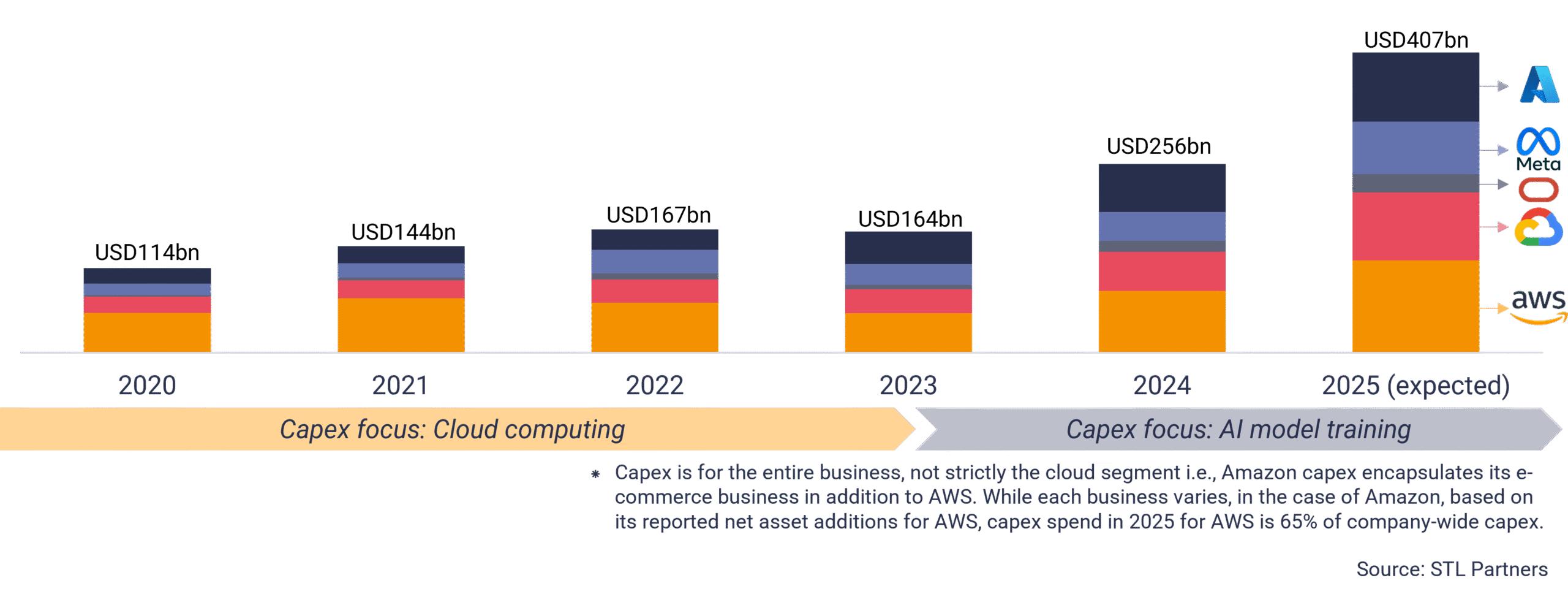

- Following the onset of the AI hype wave in 2023, capex from the five largest cloud providers (by market capitalisation) has increased substantially, as investment pours into the development of infrastructure that is capable of supporting AI model training. Indeed, these headline capex figures understate the total spend on this infrastructure, as cloud providers (namely Microsoft) also lease GPU capacity from third-party hosting providers – costs that appear as opex.

- While these companies are the most visible examples, this step-change increase in investment is reflected across the wider digital infrastructure ecosystem.

- Unlike previous infrastructure booms (such as fibre in the dotcom boom), much of today’s investment is directed towards infrastructure with a comparatively shorter lifecycle – GPUs that have a lifecycle of approximately five years. Therefore, a proportion of this capex will likely be sustained in perpetuity, illustrating the substantial value the major cloud players see in AI.

Capital expenditure: five major cloud players

If you are not a subscriber, enter your details below to download an extract of the report

Investment in model training is predicated on a view that inferencing will generate lucrative returns: But where will inferencing occur?

- The initial pre-training of AI models does not, in itself, generate value. It is only when these models are applied to new data streams to produce outputs – the process of inferencing – that end-customer value is realised. As such, the unprecedented levels of capex that is being directed into AI training infrastructure is ultimately predicated on the expectation that substantial returns will be generated during this inferencing stage of the AI model lifecycle.

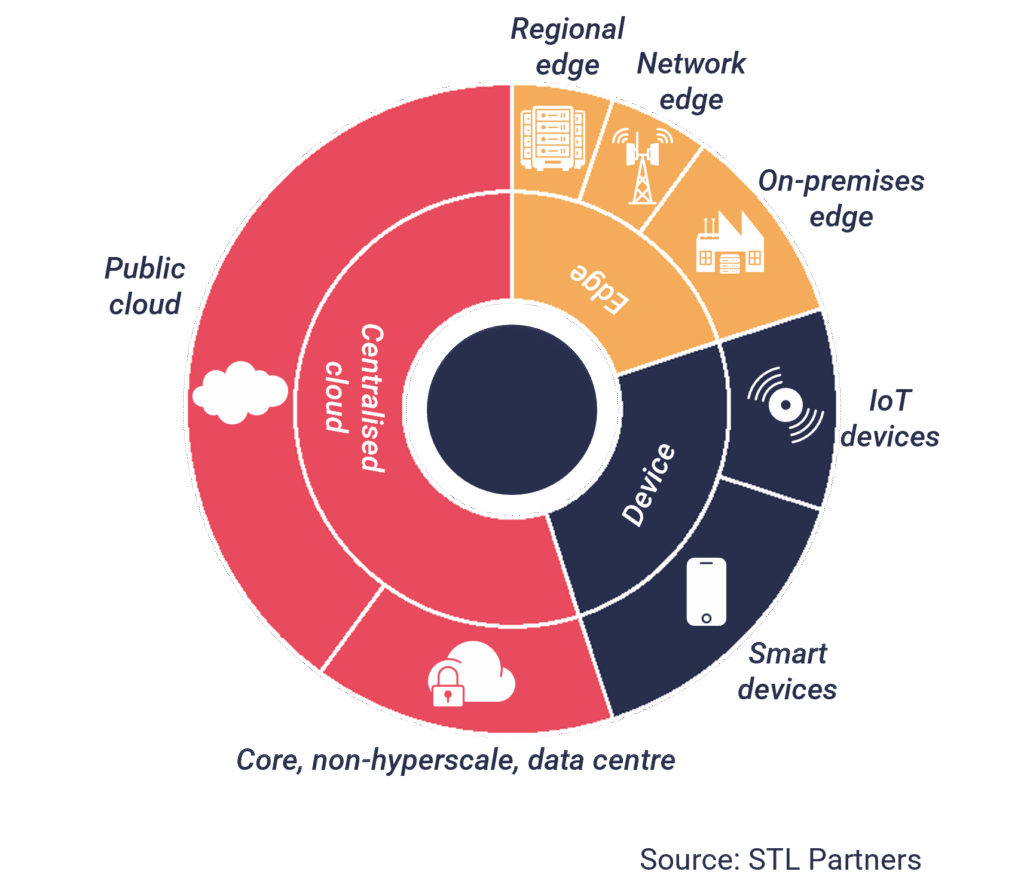

- From an edge computing perspective, the critical question is the extent to which the edge will support these inferencing workloads. Inferencing is less compute intensive than training, in some scenarios demands low latency conditions, and increasingly benefits from the interaction with proprietary enterprise data – this lends itself to deployment at the edge.

- While the cloud remains, and will continue to remain, the dominant platform for AI workloads overall, a growing share of inferencing activity will shift towards the edge, and this has visibly energised this space.

Indicative view of environments that can support inferencing workloads

This manifesto examines how, and when, the edge will be leveraged to support inferencing workloads, how this role will evolve in the near and long term, and what this ultimately means for the ecosystem: who is likely to win, and how far the value chain will consolidate.

This manifesto examines how, and when, the edge will be leveraged to support inferencing workloads, how this role will evolve in the near and long term, and what this ultimately means for the ecosystem: who is likely to win, and how far the value chain will consolidate.

Table of contents

- Executive summary

- 2020-2025: Edge in review

- AI is reshaping the edge computing landscape

- Who will win: STL’s take

Related research

- Telco edge manifesto

- Edge AI market forecast: The USD157 billion opportunity

- The telecom industry in the AI era: How telcos can follow the money

- External pressures shaping the edge AI landscape