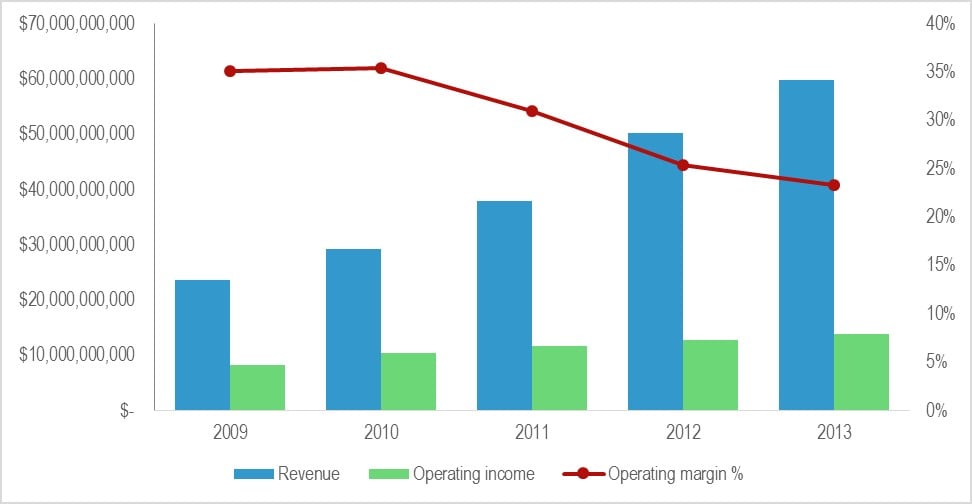

Tariffs and telcos: Uncertainty and long-term moves

No one can foresee how and when import tariffs will stabilise – but some

long-term implications are starting to arise.

No one can foresee how and when import tariffs will stabilise – but some

long-term implications are starting to arise.

Who is most likely to win the battle for contextually aware personal assistants on smartphones – and is there an opportunity for telcos?

It was no surprise that AI dominated MWC this year. But there were lots of other notable trends on the rise – including cybersecurity and data centres – and some that were disappointingly overlooked. Find out what the STL Partners team saw and missed at MWC 2025.

Based on its deep industry knowledge, STL Partners is sharing its vision on how telcos can reverse the trend of stagnating consumer revenues by focusing on innovation, new ventures and excellent customer experience.

Artificial intelligence (AI) is more powerful and affordable than ever, and the leading consumer-facing AI platforms – Google, Apple, Facebook and Amazon – are in an arms race to bring the technology to smartphones. AI will radically change the way people use smartphones, but what are the implications for data traffic and consumer expectations, and what role should telcos play in this evolution?

Facing lockout from a growing chunk of the Internet and mounting competition from the Facebook-Microsoft alliance and Amazon, Google’s core business is under intense pressure. The search giant’s response is to innovate, offering consumers proactive recommendations, as well as reactive search results. Once an interesting sideline, Google Now has become fundamental to the Mountain View company’s future. Is the suggestion service good enough to maintain Google’s position as the world’s leading big data company?

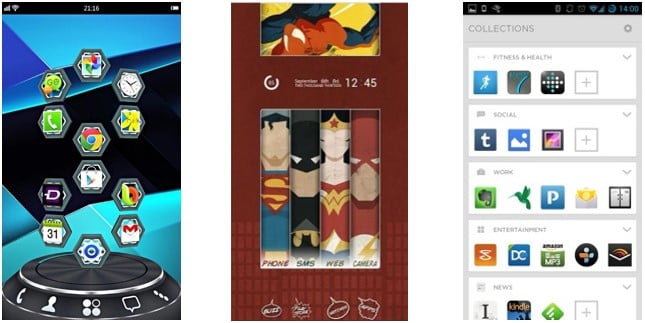

A launcher is a customizable home screen for an Android device that allows users to reorganize, customize and interact with their device. Launchers are gaining popularity, with Facebook, Google, Twitter and Yahoo all having either acquired or developed their own versions, but the market is fragmented with different launchers providing different functionality, services and monetization methods. Our latest analysis shows how telcos should seek to explore this area to help them establish more relevance in the digital ecosystem.

Telco 2.0 presents a new strategy report examining the evolution of cloud services; the current opportunities for vendors and Telcos in the Cloud market, plus a penetrating analysis on the positioning Telcos need to adapt in order to take advantage of the potential $200Bn global Cloud services market. This report offers over 140 pages of insightful commentary from those who’ve been working at the cutting edge, and includes an introduction to the sector’s key technologies and emerging trends, as well as detailed recommendations for Telcos and vendors. (December 2012, Strategy Report, Cloud and Enterprise ICT Stream.)

Cloud Strategy Report Image

The debacle with Sprint, AT&T and T-Mobile US over Carrier IQ’s phone monitoring software highlights the pitfalls and opportunities of recording user behaviour, controlling mobile broadband networks and working with personal data – a key enabler of the new digital economy and new telco business models. This is our analysis of the issues and key lessons. (December 2011, Executive Briefing Service)

Carrier IQ Smartphone Eye image Dec 2011 Telco 2.0

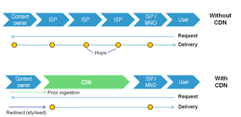

Content Delivery Networks (CDNs) are becoming familiar in the fixed broadband world as a means to improve the experience and reduce the costs of delivering bulky data like online video to end-users. Is there now a compelling need for their mobile equivalents, and if so, should operators partner with existing players or build / buy their own? (August 2011, Executive Briefing Service, Future of the Networks Stream).

Telco 2.0 Six Key Opportunity Types Chart July 2011