Lightstorm’s SmartNet and Polarin – NaaS case study

Welcome to this series analysing innovative B2B offerings by leading telcos worldwide. In this second edition, we turn our focus to a successful NaaS player in India.

Welcome to this series analysing innovative B2B offerings by leading telcos worldwide. In this second edition, we turn our focus to a successful NaaS player in India.

Welcome to this series analysing innovative B2B offerings by leading telcos worldwide.

In this first edition, we turn our focus to a successful software-as-a-service (SaaS) offering coming from Singapore.

To avoid becoming pure utilities, telcos must evolve their core businesses into more efficient and flexible infracos. But if they also want to accelerate growth and capture the full value of their network investments, they should strive towards building services businesses and becoming telecom techcos. We explore different pathways leading operators are taking to get there.

The early high hopes for SDN and NFV have given way to the realization that the road to cloud-telco ‘heaven’ is strewn with ‘infernal’ rocks and pitfalls. We present the “devil’s advocate’s” (i.e. an extremely sceptical) view of NFV set out in eight indictments. We then examine the argument for the defence.

Becoming a Telco Cloud Service Provider (TCSP) is a new vision for the future of telecoms operators, which promises hugely improved agility, a fundamentally new business model, new services, and new growth. What is this vision, how would it work, and how can it overcome the barriers to change that have thwarted most previous efforts?

If telcos in certain markets act swiftly, there is a major new and addressable opportunity in cloud created by profound recent changes in data sovereignty and security requirements. We outline the market opportunities, specific customer needs, and market sizing in our latest research.

When Amazon Web Services (AWS) landed in Australia in 2012, everyone expected carnage for Australian carriers. Telstra’s Network Applications & Services division, though, is growing fast and making some interesting moves. How did Telstra do it, and what else can be learned from its successes and its latest moves into the Healthcare market?

Albeit pioneering, Telefonica’s Digital business unit as was lacked focus and combined too many clashing cultures and incompatible businesses. Our latest analysis sees the change as ‘the end of the beginning’ for Telefonica’s Telco 2.0 services, and summarises lessons for all players implementing strategic transformation.

Amazon, Google, Apple, eBay/PayPal and Facebook are the big five brokers of digital commerce. But the disruption caused by the rise of mass-market smartphones, and the personal data they generate, means the medium-term leadership of these California-based companies is not assured. Each of them has weaknesses that could hinder their progress towards securing a strong strategic position in the new Digital Commerce 2.0 marketplace, and render them potentially vulnerable to competition from telcos, banks and/or start-ups. (October 2013, Executive Briefing Service, Dealing with Disruption Stream.) Digital Commerce 2.0 Gap

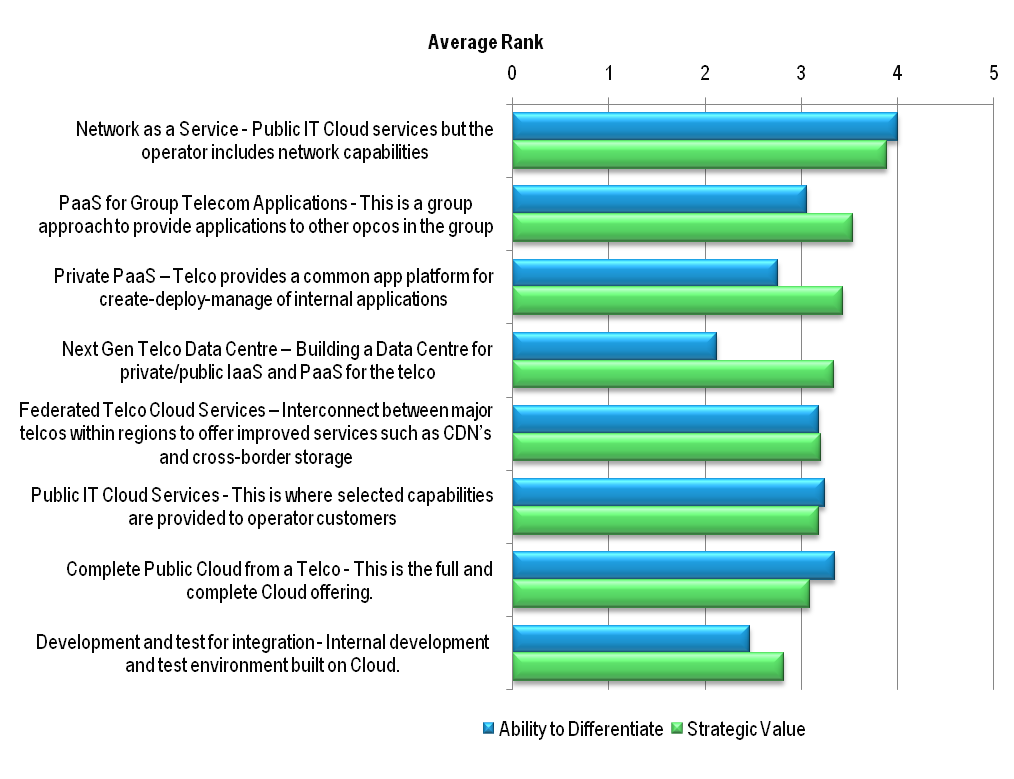

Telco 2.0 presents a new strategy report examining the evolution of cloud services; the current opportunities for vendors and Telcos in the Cloud market, plus a penetrating analysis on the positioning Telcos need to adapt in order to take advantage of the potential $200Bn global Cloud services market. This report offers over 140 pages of insightful commentary from those who’ve been working at the cutting edge, and includes an introduction to the sector’s key technologies and emerging trends, as well as detailed recommendations for Telcos and vendors. (December 2012, Strategy Report, Cloud and Enterprise ICT Stream.)

Cloud Strategy Report Image

Cloud 2.0: Event Summary Analysis. A summary of the findings of the Cloud 2.0 Executive Brainstorm, 10th November 2011, held in the Gouman Tower Hotel, London. The Brainstorm explored telcos’ strategic options to grow in the fast changing digital economy. It also considered how telcos can defend their core voice and messaging business, while also examining the steps they can take to improve the customer experience. (November 2011, Executive Briefing Service, Cloud & Enterprise ICT Stream)

Cloud 2.0: Event Summary Analysis Presentation

M2M 2.0: Service enabler strategies across multiple home hubs. Presentation by Kim Bybjerg, Head of M2M Northern Europe, Vodafone, at the EMEA Executive Brainstorm in November 2011.

M2M 2.0: Service enabler strategies across multiple home hubs Presentation

Telco 2.0’s analysis of operators’ potential role and opportunity in ‘Cloud Services’, a set of new business model opportunities that are still in an early stage of development – although players such as Amazon have already blazed a substantial trail. (December 2010, , Executive Briefing Service, Cloud & Enterprise ICT Stream & Foundation 2.0)

The early stage of development of the market means there is some confusion on the telco Cloud opportunity, yet clarity is starting to emerge, and the concept of ‘Network-as-a-Service’ found particular favour with Telco 2.0 delegates at our recent Brainstorms. (December 2010, Executive Briefing Service, Cloud & Enterprise ICT Stream)

IBM say that telcos are well positioned to provide cloud services, and forecast an $89Bn opportunity over 5 years globally. Video presentation and slides including forecast, case studies, and lessons for future competitiveness. (December 2010, Executive Briefing Service, Cloud & Enterprise ICT Stream).

The point and value of Cloud Services can sometimes seem elusive. Here’s a well received presentation that includes a simple, workable definition and seven case studies that illustrate different types of ‘Cloud Services’ / xAAS (e.g. Network, Platform-As-A-Service). (December 2010, Executive Briefing Service, Cloud & Enterprise ICT Stream)

Over the last 10 years, Nokia has sustained a keen interest in applications and services as a complement to its dominant position in hardware and operating systems. It’s hard to say that they’ve made any progress in making a business of it.