Login to access

Want to subscribe?

This article is part of: Executive Briefing Service, Network Innovation

To find out more about how to join or access this report please contact us

Becoming a Telco Cloud Service Provider (TCSP) is a new vision for the future of telecoms operators, which promises hugely improved agility, a fundamentally new business model, new services, and new growth. What is this vision, how would it work, and how can it overcome the barriers to change that have thwarted most previous efforts?

Introduction

Structural barriers preventing telecoms business model change

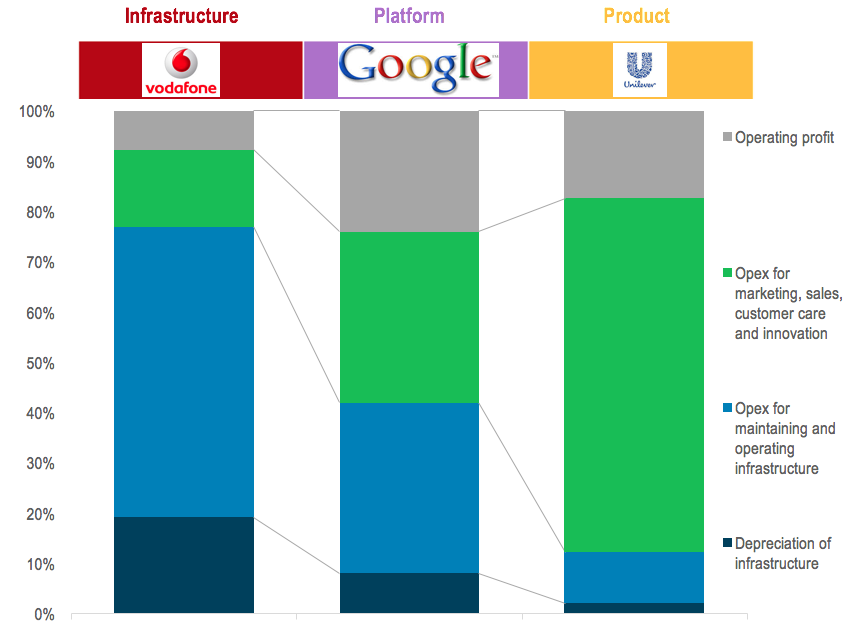

In our recent report, Problem: Telecoms technology inhibits operator business model change (Part 1), we explained how financial and operational processes that have been adopted in response to investor requirements and regulation have prevented operators from innovating.

Operator management teams make large investments over seven- or eight-year investment cycles and are responsible for deploying and managing the networks from which revenues flow. As we show in Figure 1 below, operators therefore have much more of their costs tied up in capital expenditure than platform players or product innovators. Furthermore, they need large quantities of operating expenditure to maintain and operate their networks. The result is a rather small percentage of revenue – we estimate around 15% – which they devote to activities focused on innovation: marketing, sales, customer care, and product and service development (the green section of the bars). This compares unfavourably to a platform player, such as Google, which we estimate devotes around 35% of revenue to these activities. The difference is even more pronounced with a product innovator, such as Unilever, which minimises capital investment by outsourcing some of its manufacturing and all product distribution and so devotes nearly 70% of revenue to ‘innovation’ activities.

Figure 1: The telecoms cost structure inhibits innovation

Sources: Company accounts; STL Partners estimates and analysis

Seen in this context, how can anyone expect operators to be successful at developing new platforms, channels, or products?

- Executive Summary

- Introduction

- Structural barriers preventing telecoms business model change

- Digital service innovation is proving tough for operators

- Structural barriers coming down?

- Virtualisation + cloud business practices could transform the telecoms business model

- The drive for virtualisation is underway

- Cost reduction and a new cost structure

- Cloud business practices are a critical component in the future telco

- The Telco Cloud Service Provider (TCSP)

- Two benefits from becoming a Telco Cloud Service Provider

- Product and service creation in the Telco Cloud Service Provider

- From incremental and slow innovation today…

- …to radical and fast innovation in the TCSP of tomorrow

- Figure 1: The telecoms cost structure inhibits innovation

- Figure 2: Telcos have struggled to launch successful digital services

- Figure 3: Cloud and virtualisation can allow a telco to transform its cost structure

- Figure 4: Cloud business practices – key principles

- Figure 5: Defining the Telco Cloud Service Provider

- Figure 6: Telco Cloud can spur transformation across the entire telco business

- Figure 7: Product development – telco today vs Telco Cloud Service Provider