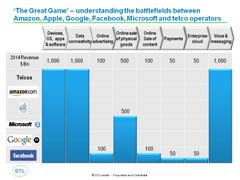

Samsung and Google versus Apple?

Apple is weakening Samsung Electronics’ grip in the high-end of the handset market, lowering the Korean company’s profitability and capacity to compete effectively. After a series of largely unsuccessful attempts to break into software and services, a daring option for Samsung is to seek a strong, strategic alliance with Google to enable both companies to mount a serious challenge to Apple’s dominance in the affluent demographic. Telcos could back such an alliance in return for a profitable role in the service layer. This report analyses the strategic rationale for such an approach.