Login to access

Want to subscribe?

This article is part of: Executive Briefing Service

To find out more about how to join or access this report please contact us

Some telcos are hoping that mobile data growth will resurge and transform their fortunes, though STL Partners has previously argued that data growth will not be enough. In this report we re-examine this argument looking at global trends and present the insights and lessons from six operator case-studies including DNA Finland, T-Mobile US and Reliance Jio.

Introduction

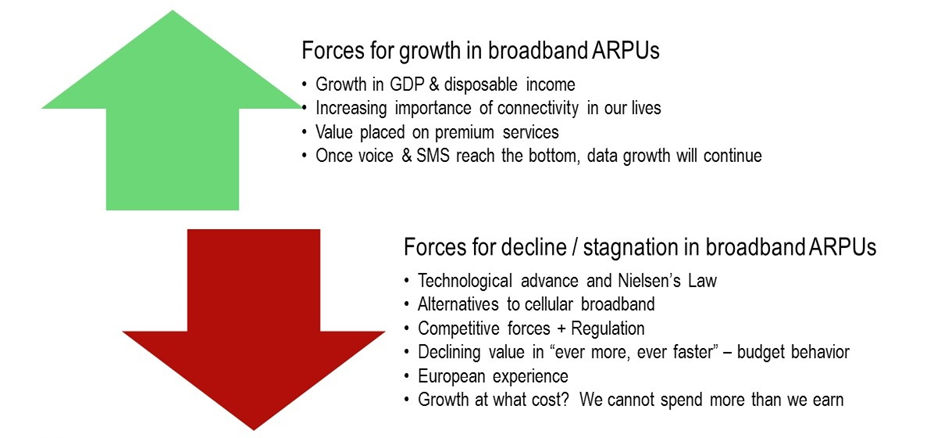

A recent STL Partners report – Which operator growth strategies will remain viable in 2017 and beyond? – looked at the growth strategies of 68 operator groups, and identified eight different growth strategies employed over this sample. The eighth strategy was to expect mobile data growth to start to reverse the decline in revenues once the decline in voice and messaging revenues is complete. In the previous report, we argued that data revenue growth would not rapidly counterbalance the losses of voice and messaging due to the forces outlined in Figure 2 below:

Figure 2: Trust in the increasing value of (and spend in) broadband data

Source: STL Partners

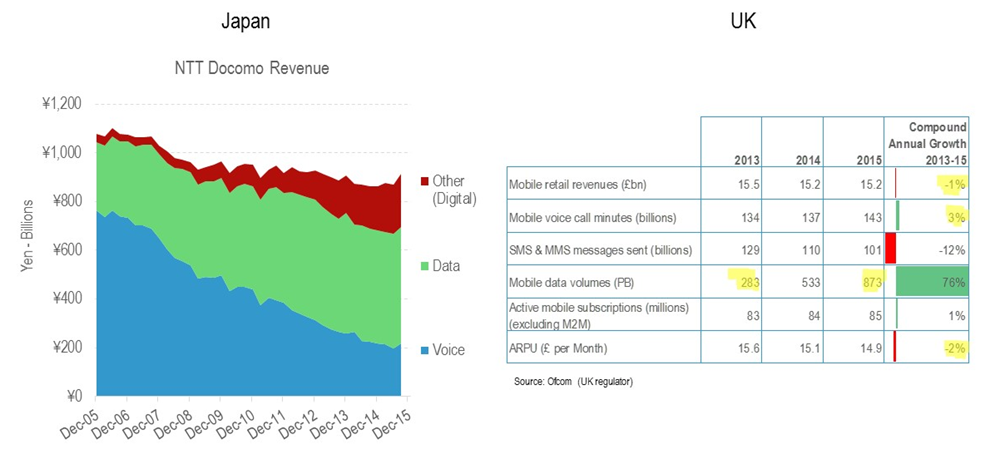

In that report, we showed a number of examples, including NTT Docomo in Japan, which has been experiencing voice and messaging declines for the longest period of telcos we are aware of, and the UK market, which is competitive with relatively good availability of market data (See Figure 3):

Figure 3: STL Partners can find no evidence of long term revenue growth driven by increased mobile broadband demand in mature markets (outside duopolies)

Source: Company accounts, STL Partners

Despite the clarity of our own convictions on this matter, we are aware that some telcos are growing their revenues, and also that a minority of our clients (perhaps one in ten based on a number of informal surveys we have run in workshops etc.) believe that data could start to regrow the market in certain conditions.

Given how attractive this idea is to the industry, and how difficult and lengthy the path of transformation and creating digital services is proving for telcos, we decided that it would be useful to revisit our assertions, to dig deeper to see what signs of growth we could find and what might be learned from them. This report contains our findings from this further analysis.

Background: The telco ‘hunger gap’

This decline is not a new story, and STL Partners has been warning about this phenomenon and the need for business model change since 2006.

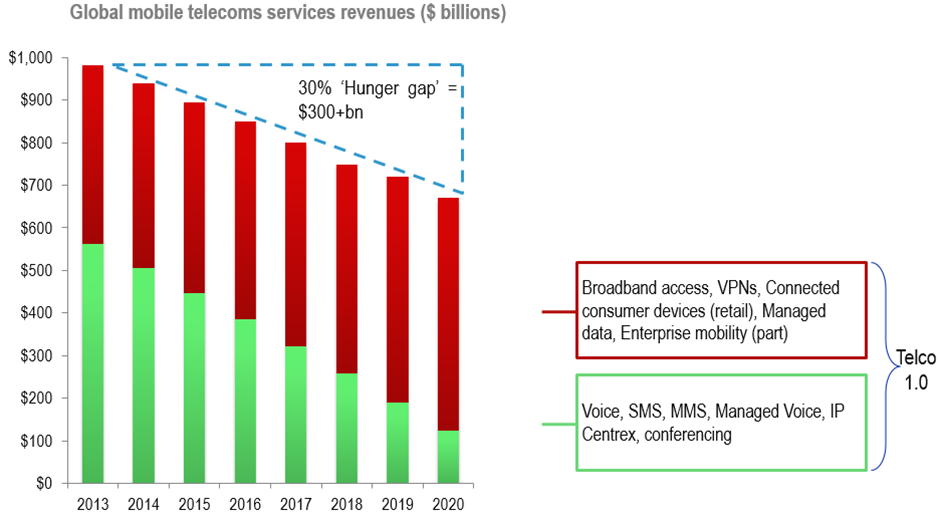

Back in 2013, STL Partners estimated that digital business would need to represent 25+% of Telco revenue by 2020 to avoid long-term industry decline. However, to date we have not taken the view that data revenues will to grow enough to make up for the decline in traditional services, meaning that “hunger gap” will not be filled this way (see Figure 4).

Figure 4: The telco ‘hunger gap’ between the decline in traditional and data revenues

Source: STL Partners

However, making the transition to new business models is challenging for telcos, who have traditionally relied on an infrastructure-based business model. Digital businesses are very different, and the astronomical growth in demand for mobile data services over the past decade is placing severe strain on networks and resources.

We have argued that telcos now need to make a fundamental shift from their traditional infrastructure-based business model to a complex amalgam of infrastructure, platform, and product innovation businesses.

Alternatively, growing data would be an innately attractive prospect for the telecoms industry. It would not require all the hard work, risk, change and investment of transformation. Hard-pressed executives would love nothing better than the ‘do little’ strategy to work out. It’s an idea that can easily find traction and supporters.

But is it a realistic prospect to grow data revenues faster than voice and messaging are shrinking?

To sense-check our original assertion that data will not grow overall revenues, this report takes a new look at the available evidence. We picked six different telcos appearing to exhibit representative or outlier strategies to see whether there may currently be grounds to change our view that data revenue growth will not grow the overall telecoms market.

Content:

- Executive Summary

- Introduction

- Background: the telco ‘hunger gap’

- Methodology

- Review of global trends in data growth

- The explosion in mobile data growth

- The link between data consumption and ARPU

- The rise of 4G

- Data tariff bundles increase in volume

- Mobile data offloading

- Multiplay bundling and the fixed network advantage

- International data roaming

- Zero rating and net neutrality

- Case studies – different data strategies

- Four data growth strategies

- The traditional growth model

- The disruptor/challenger model

- The innovator model

- The OTT proposition

- Case studies comparison: Investment vs risk in summary

- Case study: Innovator: DNA (Finland)

- Case study: Disruptor/Innovator: T-Mobile US

- Case study: Super-disruptor: Reliance Jio (India)

- Case study: Disruptor: Free (France)

- Case study: Traditional/Innovator: Vodafone UK

- Case study: Traditional: Cosmote (Greece)

- Conclusions

- Case studies comparison: Investment vs risk in summary

- Telcos need to seek fresh business models

- Network investment will need to be even more intelligently targeted than with 3G/4G

- New growth opportunities are emerging

- A little thoughtful innovation goes a long way

- Recommendations

Figures:

- Figure 1: Trust in the increasing value of (and spend) in broadband data

- Figure 2: Trust in the increasing value of (and spend) in broadband data

- Figure 3: STL Partners can find no evidence of long-term revenue growth driven by increased mobile broadband demand in mature markets (outside duopolies)

- Figure 4: The telco “hunger gap” between the decline in traditional and data revenues

- Figure 5: Cisco global data growth 2016-2021

- Figure 6: Total estimated UK mobile retail revenues

- Figure 7: SMS and MMS sent in the UK, 2007-2015

- Figure 8: Selected telco data growth strategies

- Figure 9: Analysis of mobile operator growth strategies

- Figure 10: DNA revenues and churn 2012-2016

- Figure 11: DNA mobile data growth 2010-2016

- Figure 12: DNA mobile data growth forecast

- Figure 13: USA average monthly data use, 2010-2015

- Figure 14: Deutsche Telekom non-voice % of ARPU, 2009-2016

- Figure 15: T-Mobile US total revenues and non-voice ARPU, 2009-2016

- Figure 16: Reliance Jio subscription growth

- Figure 17: Free Mobile 4G subscriptions and 4G data, 2015-2016

- Figure 18: Iliad Free revenue growth 2012-2016

- Figure 19: France average mobile data use per SIM, 2009-2015

- Figure 20: France mobile value added service revenues, 2009-2015

- Figure 21: Vodafone UK data use and total mobile ARPU, 2011-2016

- Figure 22: UK mobile retail ARPU, 2010-2016

- Figure 23: UK estimated mobile retail revenues, 2010-2015

- Figure 24: Vodafone UK total mobile revenue 2013-2016

- Figure 25: Greece data use and total mobile revenues