Telco plays in live entertainment

Live entertainment is evolving fast, as greater connectivity and digitisation allows for new experiences for both the audience at the venue and the people watching online. How can telcos play a more valuable role?

Live entertainment is evolving fast, as greater connectivity and digitisation allows for new experiences for both the audience at the venue and the people watching online. How can telcos play a more valuable role?

Mobile operators have many of the assets and capabilities required to become a major force in financial services, but they will also need to tap expertise in data analytics/machine learning.

Investment in fintech has increased by 500% in the last 3 years. Interest and investment has spiked as fintech companies seek to leverage new sources of data to develop disruptive offerings across a broad range of financial service areas (e.g. payments, lending & funding). The scale and scope of investment and activity represents a potential paradigm shift within financial services. Telcos, who have a long history developing financial services (e.g. mobile money), need to understand this changing landscape. This report explores why fintech is happening now and maps where and how it is disrupting established financial services.

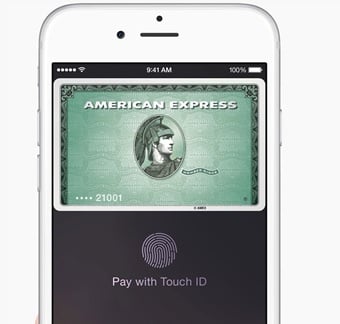

The unveiling of Apple Pay and unravelling of Weve (the UK operators’ payments venture) looked like bad news for telcos’ ambitions in mobile payments in some markets, and highlighted challenges to Google and others’ models. Yet there are already successful telco models and favourable market trends that telcos should exploit. So what are the opportunities now?

Amazon, Google, Apple, eBay/PayPal and Facebook are the big five brokers of digital commerce. But the disruption caused by the rise of mass-market smartphones, and the personal data they generate, means the medium-term leadership of these California-based companies is not assured. Each of them has weaknesses that could hinder their progress towards securing a strong strategic position in the new Digital Commerce 2.0 marketplace, and render them potentially vulnerable to competition from telcos, banks and/or start-ups. (October 2013, Executive Briefing Service, Dealing with Disruption Stream.) Digital Commerce 2.0 Gap

Telcos, Internet and technology players, banks and payment networks have disruptive $billion opportunities to act as intermediaries / enablers in mobile commerce and personal cloud services, based on the appropriate use of customer data. This report is a unique and comprehensive strategic guide for success in these roles. It analyses the strategies of the main and cutting-edge players, and outlines key success factors in designing and delivering customer propositions, technology, organisation and value network strategies. It also includes evaluations of the related strategic opportunities of ‘raw big data’, professional data services, and internal data use, and a business model showing how one type of candidate for the intermediary role, a telco, could grow profitable new revenues equivalent to c.$50Bn (5% of existing core revenues) within five years. (October 2013, Dealing with Dsiruption Stream). Telco 2.0 Transformation Index Small

The transformed mobile web experience, brought about by the adoption of a range of new technologies, is creating a new arena for operators seeking to (re)build their role in the digital marketplace. Operators are potentially well-placed to succeed in this space; they have the requisite assets and capabilities and the desire to grow their digital businesses. This report examines the findings of interviews and a survey conducted amongst key industry players, supplemented by STL Partners’ research and analysis, with the objective of determining the opportunities for operators in the New Mobile Web and the strategies they can implement in order to succeed. (September 2013, Foundation 2.0, Executive Briefing Service.)

Operator Opportunities in the “New Mobile Web”

The ‘Mobile/Digital Wallet’ needs to evolve to support authentication, search and discovery, as well as payments, vouchers, tickets and loyalty programmes. Moreover, consumers will want to be able to tailor the functionality of this “commerce assistant” or “commerce agent” to fit with their own interests and preferences. Our report and analysis of the Digital Commerce 2.0 Executive Brainstorm, 20 March 2013, part of the New Digital Economics Silicon Valley event. (April 2013, Executive Briefing Service, Dealing with Disruption Stream.)

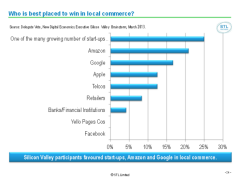

Who is best placed to win in local commerce April 2013

Regardless of business strategy, the development of ‘Smart Pipes’ – more intelligent networks – will be a key driver of shareholder returns from operators. Smarter networks will also benefit network users – upstream service providers and end users, and operators, and their vendors and partners, will need to compete to be the smartest. What are they, why are they needed, and what are the key strategies employed to develop them? (February 2012, Foundation 2.0, Future of the Networks Stream).

Facebook user saturation bubble chart