Consumer innovation tracker

A global database of innovative telco consumer services beyond connectivity

A global database of innovative telco consumer services beyond connectivity

Trends and insights from our database of quantum technology trials and deployments within telcos worldwide

It was no surprise that AI dominated MWC this year. But there were lots of other notable trends on the rise – including cybersecurity and data centres – and some that were disappointingly overlooked. Find out what the STL Partners team saw and missed at MWC 2025.

As society becomes ever more dependent on connectivity, telcos face a growing risk of being regulated like traditional utility companies. This report details how operators can avoid falling into “the utility trap” and drive growth in the next decade.

With the rollout of 5G, the telecoms industry could coordinate the development of early warning systems to mitigate the impact of pollution, wildfires, floods, infectious diseases and other threats.

What can others learn from SK Telecom’s advanced efforts to grow in the face of declining core telecoms revenues? 5G is a part of the story, but not all of it.

Edge computing is a strategic opportunity for telcos. We examine the driving needs and applications for telco edge computing, describe the market and the options for telcos, discuss their partnerships with hyperscalers and recommend key actions.

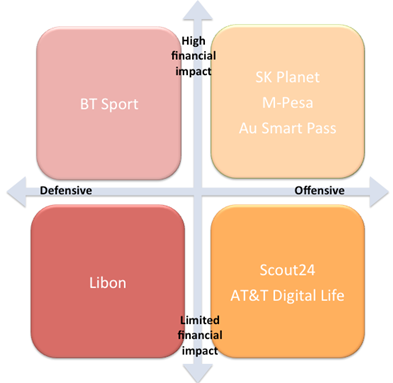

Although telcos aren’t generally associated with disruption, many operators around the world have attempted to disrupt adjacent markets, such as digital commerce, entertainment and financial services. In some cases, telcos have even disrupted their core broadband and communications markets. While many of these moves have fizzled out or have flown below investors’ radar screens, several have had a major impact on both the telco’s revenues and relevance. These include SK Planet, M-Pesa, Au Smart Pass and BT Sport. Why do some disruptive moves by telcos succeed and others fail?

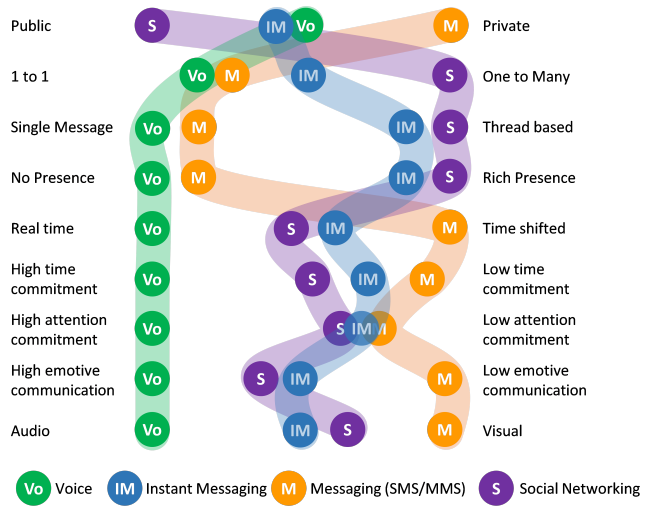

Consumer and enterprise communications behaviours are changing significantly around the globe as new solutions meet core needs more effectively and change customer expectations. This extract from our latest major report provides insight to the changes, and describes effective strategies that meet these evolving needs for both incumbents attempting to defend existing services and innovators seeking to disrupt and create new value. (December 2013, Executive Briefing Service)

Psychological and social advantages of voice, SMS, IM, and Social Media Dec 2013

Telcos, Internet and technology players, banks and payment networks have disruptive $billion opportunities to act as intermediaries / enablers in mobile commerce and personal cloud services, based on the appropriate use of customer data. This report is a unique and comprehensive strategic guide for success in these roles. It analyses the strategies of the main and cutting-edge players, and outlines key success factors in designing and delivering customer propositions, technology, organisation and value network strategies. It also includes evaluations of the related strategic opportunities of ‘raw big data’, professional data services, and internal data use, and a business model showing how one type of candidate for the intermediary role, a telco, could grow profitable new revenues equivalent to c.$50Bn (5% of existing core revenues) within five years. (October 2013, Dealing with Dsiruption Stream). Telco 2.0 Transformation Index Small