Facebook + WhatsApp + Voice: So What?

So Facebook is buying the mobile IM app WhatsApp for $19bn including $4bn in cash, and WhatsApp is launching a voice service. Why, and what are the consequences and lessons for telcos and others?

So Facebook is buying the mobile IM app WhatsApp for $19bn including $4bn in cash, and WhatsApp is launching a voice service. Why, and what are the consequences and lessons for telcos and others?

Our new research shows how telcos can slow the decline of voice and messaging revenues and build new communications services to maximise revenues and relevance with both consumer and enterprise customers. It includes detailed forecasts for 9 markets, in which the total decline is forecast between -25% and -46% on a $375bn base between 2012 and 2018, giving telcos an $80bn opportunity to fight for. It also shows impacts and implications for other technology players including vendors and partners, and general lessons for competing with disruptive players in all markets. It looks at the impact of so-called OTT competition, market trends and drivers, bundling strategies, operators developing their own Telco-OTT apps, advanced Enterprise Communications services, and the opportunities to exploit new standards such as RCS, WebRTC and VoLTE. (November 2013, Executive Briefing Service). Future Value of Voice and Messaging Cover Small

150 senior execs from Vodafone, Telefonica, Etisalat, Ooredoo (formerly Qtel), Axiata and Singtel supported our technology survey for the Telco 2.0 Transformation Index. This analysis of the results includes findings on prioritisation, alignment, accountability, speed of change, skills, partners, projects and approaches to transformation. It shows that there are common issues around urgency, accountability and skills, and interesting differences in priorities and overall approach to technology as an enabler of transformation. (November 2013, Executive Briefing Service, Transformation Stream.) Telco 2.0 Transformation Index Tech Survey Cover Small

The Cloud market is on the verge of the next wave of market penetration, yet it’s likely that only one in five Cloud Service Providers (CSPs) in today’s marketplace will still be around by 2018, as providers fail or are swallowed up by aggressive competitors. So what do CSPs need to do to survive and prosper? (October 2013, Foundation 2.0, Executive Briefing Service, Cloud & Enterprise ICT Stream.)

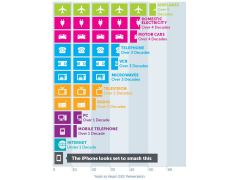

Technology adoption rates Sept 2013

A step-by-step guide for telecoms executives seeking to innovate and develop compelling new services to compete in the ‘services layer’, and develop a new telecoms business models to replace the contracting voice and messaging revenue streams with new revenues from new products and services and customers. (September 2013, Executive Briefing Service, Transformation Stream.)

Finding the Next Golden Egg

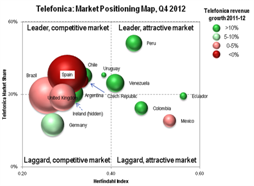

This extract from the Telco 2.0 Transformation Index shows our analysis of Telefonica’s markets and market position, including economic and digital market maturity, regulation, customers, competition and pricing. It is one part of our overall analysis of Telefonica’s progress towards transformation to the Telco 2.0 business model. The other parts of the Telefonica analysis are: Service Proposition, Finances, Technology, Value Network, and an overall summary. Telefonica is one of the companies analysed and compared in the first tranche of analysis that also addresses Vodafone, AT&T, Verizon, Axiata, SingTel, Etisalat and Ooredoo (formerly Qtel). (August 2013, Executive Briefing Service, Transformation Stream.) Telefonica Telco 2.0 Transformation Index Small

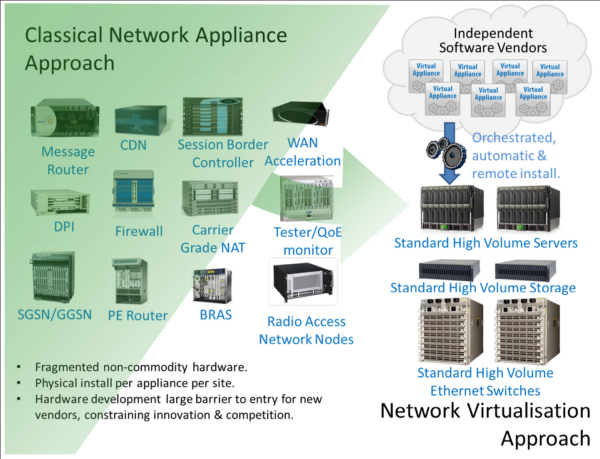

This extract from our recent Executive Briefing on Software Defined Networking (SDN), describes ‘Network Functions Virtualisation’ (NFV), the problems it solves, and how it relates to SDN. (June 2013, Foundation 2.0, Executive Briefing Service, Cloud & Enterprise ICT Stream.)

Network Functions Virtualisation (NFV) Approach June 2013

The ‘Mobile/Digital Wallet’ needs to evolve to support authentication, search and discovery, as well as payments, vouchers, tickets and loyalty programmes. Moreover, consumers will want to be able to tailor the functionality of this “commerce assistant” or “commerce agent” to fit with their own interests and preferences. Our report and analysis of the Digital Commerce 2.0 Executive Brainstorm, 20 March 2013, part of the New Digital Economics Silicon Valley event. (April 2013, Executive Briefing Service, Dealing with Disruption Stream.)

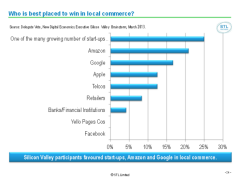

Who is best placed to win in local commerce April 2013

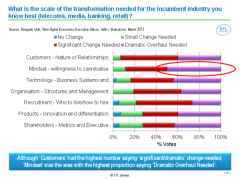

Value is squeezed out of industries as they become increasingly digital – i.e. accessed by mobile and online, driven by data and defined by software. We call the collective economic impact of this pressure ‘The Great Compression’. But which companies will survive and prosper – and how? 90% of the Execs at our Silicon Valley brainstorm identified ‘management mindset’ as a key factor in Telecoms, Media, Finance and Retail. Our analysis and a detailed report of the findings of the Digital Economy session at the NDE Executive Brainstorm, Silicon Valley, held at the InterContinental Hotel, San Francisco on the 19th March 2013. (May 2013, Executive Briefing Service, Transformation Stream).

Scale of Transformation Needed April 2013

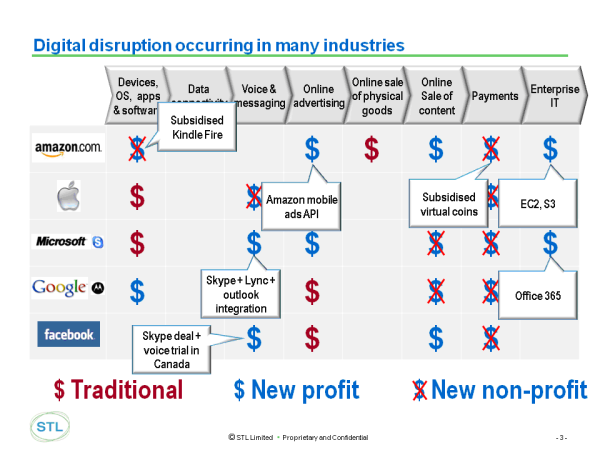

In the next 10 years, many industries face the ‘Great Compression’ in which, in addition to the pressures of ongoing global economic uncertainty, there is also a major digital transformation that is destroying traditional value and moving it ‘disruptively’ to new areas and geographies. For the incumbent industry players we call the near-term results of this disruption ‘The Digital Hunger Gap’ – the widening deficit between past and projected revenues. This is our analysis of the top-level findings of the Silicon Valley Executive Brainstorm. (March 2013, Executive Briefing Service, Transformation Stream.)

10 Year Hunger Gap Mar 2013

Structuring finances is key for the success of innovations in general and Telco 2.0 projects in particular. In this detailed extract from our new strategy report ‘A Practical Guide to Implementing Telco 2.0’, we describe the best ways to approach the management of revenues and costs of new business models, and how to get the CFO and finance department onside with the new approaches required (February 2013, Executive Briefing Service, Transformation Stream).

Small table on finances

The mobile commerce market is going through a critical ‘land-grab’ phase. This report reviews the strategies and tactics of the leading telcos and Internet players in Asia, Europe and North America as they seek to use the mobile medium to become an intermediary between buyers and sellers. It considers the pivotal role of the digital wallet, ‘big data’, the race to acquire merchants and the key alliances between telcos, banks, payment networks and Internet players (December 2012, Executive Briefing Service, Dealing with Disruption Stream)

Digital Commerce Flywheel December 2012

How can communications services providers (CSPs) transform their businesses from Telco 1.0 (infrastructure-led stasis) to Telco 2.0 (sustainable innovation-led growth)? An essential, step-by-step guide to the implementation of new Telco 2.0 business models, providing telecoms executives and their partner companies with a systematic approach to capitalise on new opportunities and neutralise potential threats. The report outlines robust frameworks and methodologies for selecting the right Telco 2.0 strategy for each organization, identifying and implementing the key opportunities, and avoiding expensive and time-consuming mistakes. (December 2012, Telco 2.0 Transformation Stream) Telco 2 Implementation Cover

Telco 2.0 presents a new strategy report examining the evolution of cloud services; the current opportunities for vendors and Telcos in the Cloud market, plus a penetrating analysis on the positioning Telcos need to adapt in order to take advantage of the potential $200Bn global Cloud services market. This report offers over 140 pages of insightful commentary from those who’ve been working at the cutting edge, and includes an introduction to the sector’s key technologies and emerging trends, as well as detailed recommendations for Telcos and vendors. (December 2012, Strategy Report, Cloud and Enterprise ICT Stream.)

Cloud Strategy Report Image

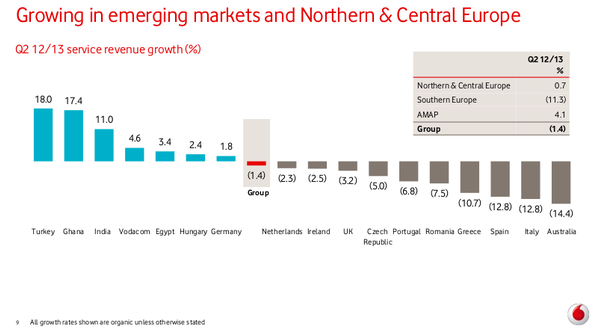

In our recent briefing European Mobile: The Future’s Not Bright, It’s Brutal, we predicted that European operators faced a grim future. New figures from Vodafone and Telefonica suggest that, unfortunately, the grim future is arriving fast. (November 2012, Executive Briefing Service, Transformation Stream.)

Vodafone results Nov 2012

Telcos traditionally think of every new service as a profitable new revenue source, and create services in silos with little thought for the total customer experience and overall creation of value. In contrast, the big internet and tech players typically build their future offerings as part of an integrated strategy to raise the overall value of their platforms. This extract from ‘A Practical Guide to Implementing Telco 2.0’ shows key lessons for telcos. (September 2012, Executive Briefing Service, Dealing with Disruption Stream.)

.

Generic Telco Strategies September 2012

Telefonica and Vodafone are both European-based tier 1 CSPs with substantial revenues, cash flows and subscribers. They have both expanded beyond Europe – Vodafone into Africa and Asia and Telefonica into Latin America. However, their Telco 2.0 strategies are rather different. In this extract from our forthcoming report, A Practical Guide to Implementing Telco 2.0, we outline their Telco 2.0 strategies and their benefits and risks. (September 2012, Executive Briefing Service, Transformation Stream.)

Telefonica Strategy 2.0 Chart