Is the consumer edge opportunity overlooked?

Consumer use cases offer a variety of opportunities for telcos and other stakeholders in the area of distributed edge. This report explores seven such use cases and the implications for telcos.

Consumer use cases offer a variety of opportunities for telcos and other stakeholders in the area of distributed edge. This report explores seven such use cases and the implications for telcos.

Telcos and the major Internet platforms increasingly rely on each other. What kinds of agreements should operators enter into with Amazon, Apple, Facebook and Google and what should they avoid? And what are the strategic implications of supporting players who habitually use their powerful brands and software expertise to disrupt entire industries?

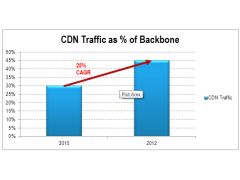

Changing consumer behaviours and the transition to 4G are likely to bring about a fresh surge of video traffic on many networks. Fortunately, mobile content delivery networks (CDNs), which should deliver both better customer experience and lower costs, are now potentially an option for carriers using a combination of technical advances and new strategic approaches to network design. This briefing examines why, how, and what operators should do, and includes lessons from Akamai, Level 3, Amazon, and Google. (May 2013, Executive Briefing Service).

CDN Traffic as Percentage of Backbone May 2013

Content Delivery Networks (CDNs) such as Akamai’s are used to improve the quality and reduce costs of delivering digital content at volume. What role should telcos now play in CDNs? (September 2011, Executive Briefing Service, Future of the Networks Stream).

Should telcos compete with Akamai?