Login to access

Want to subscribe?

This article is part of: Consumer

To find out more about how to join or access this report please contact us

Physical retail was under pressure which COVID-19 exacerbated. However, it is not just a matter of decline: telcos are finding new models of hybrid retail that create new solutions that their customers need and embody the Coordination Age.

Evolving retail store footprint

This report looks at how MNO retail stores and the store footprint has evolved over the last three to four years as operators have progressed with developing a digital first and omni-channel approach that has moved customer service and sales online. It looks at the importance of delivery fulfilment and how operators are utilising physical retail stores to complement the online channel with fulfilment that gives customers near instant gratification on device purchases. While some believe physical stores might eventually be swallowed by the metaverse, telecoms operators for the moment are maintaining a store footprint, which despite reduced in size and in some markets shifted to franchise status, is being used to introduce new product and service lines.

Enter your details below to request an extract of the report

Impact of online on the high street

Consumer shift towards online shopping was evident for some time prior to COVID-19. However, 2020 and 2021 saw accelerated consumer adoption of e-commerce across the world.

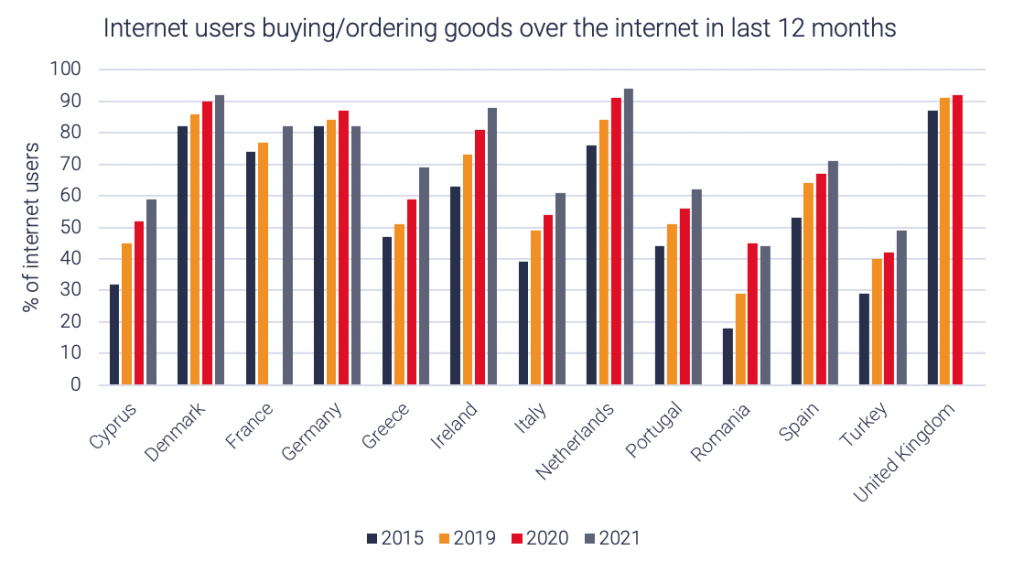

In the EU, for example, Eurostat shows online shopping increased by 4%compared to 2019, and as economies began to re-open in 2021 online shopping increased by a further 1% from 2020. Adoption of e-commerce across European markets varies. In the Netherlands, Denmark, Germany, Sweden, Ireland and the UK over 80%of the internet users buy goods and services online. Whereas in Italy for example, adoption is lower where 61% of internet users bought online in 2021, although adoption is significantly up from 49% in 2019.

E-commerce uptake is strong but still varies by market

Source: Eurostat, STL Partners

The most common categories purchased online tend to be:

- Clothing (including sports clothes) shoes and accessories (ordered by 68% of online shoppers);

- Followed by deliveries from restaurants and fast-food chains (31% of online shoppers);

- Electronics such as computers, tablets, mobile phones or their accessories were purchased by 23% of online shoppers.

The categories represent a blended EU figure and likely to be higher (or lower) across individual markets.

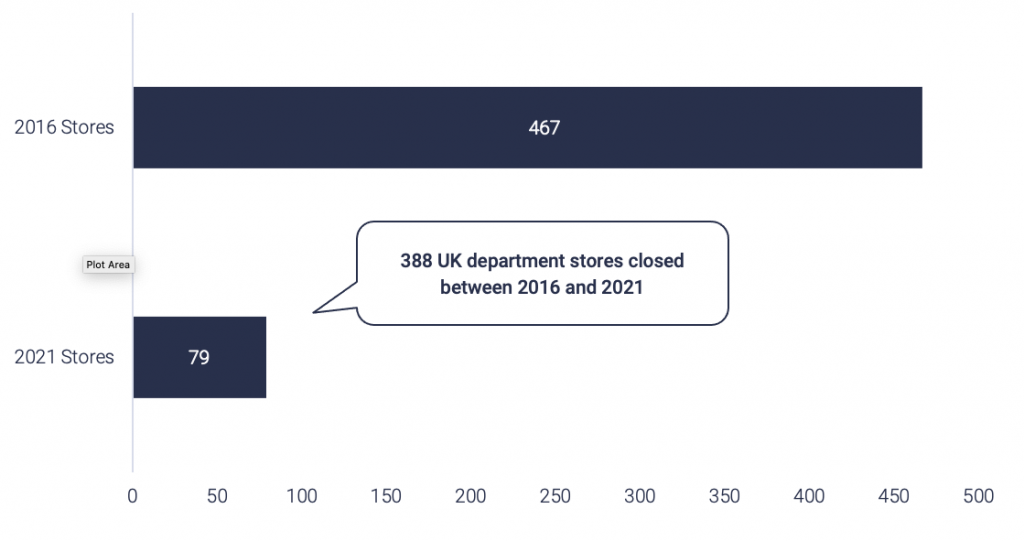

These online trends have taken their toll on the high street and this is most evident in clothing and fashion sector. Tracking the closures of some of the UK’s largest department stores and retail chains such as British Home Stores (BHS), Beales, Debenhams and House of Fraser, commercial property insight firm CoStar Group estimates 388 department stores closed in the UK between 2016 and 2021. However, there are signs (at least in the US) of a slowing in announced store closures according to CoStar, as the economy opens up and consumers adjust to a normality which is transitory in itself.

UK department stores

Source: https://www.bbc.com/news/business-58331168

Telco retail transition was already underway

Over the last five years at least, telecoms operators in the midst of transitioning to an omni-channel and digital-first consumer footing have been thinking about what to do with their retail commercial real estate, particularly given the trend of consumers towards online and SIM-only / digital only service propositions. Many Apple iPhone customers today purchase direct from Apple online, while marketplaces such as Amazon are popular destinations to purchase SIM-free devices.

- According to the GSMA, before COVID-19 operators were already forecasting that 52% of their smartphones would be purchased online.

The young consumer segment can be a difficult group to entice into stores. In recent years operators have found common ground with this segment through digital only brands which don’t require a store visit in order to purchase a SIM connection or verify identity, as these activities which can all be handled remotely over a video call and in-App.

- Verizon’s Visible brand claims it has “cut out stores (and the salespeople that come with them)” to create its digital only low-cost customer value proposition with a 24/7 customer care team”.

However, some operators opt to promote their low-cost brand in-store alongside their main premium brand. Vodafone has demonstrated this in Spain by offering its Lowi brand in Spanish Vodafone stores and in the UK by promoting its VOXI brand in store.

Telecom retail specialists NTS told us that some digital-only retail brands can opt to form a physical (albeit still minimum) connection with customers by using kiosks to help customers perform tasks such as SIM collection, payment, or replenishment.

In a bid to move beyond offering just phones, operators provide thematic areas in their stores to promote services and solutions around smart home, office, personal entertainment, and health. These specialised spaces are useful for introducing new products but can be difficult to implement where store space is limited. Smart home products are also most likely to resonate with older customers who own their home or have a more established settled status.

In 2019, leading telecoms operators collaborated on a TM Forum Catalyst project reimaging the role of the retail store in 2025. The outcome of this project envisioned opening up the store to partners and playing a B2B2C role. It also heavily emphasised the store being used as a vehicle to host events, technical demonstrations, workshops and educational sessions. Speaking with a participant in the project, it was felt that perhaps these events have not proved to be a draw in encouraging customers – particularly younger customers – back into the store. The scale of events is also linked to the floor space available. The project did cite issues relating to the level of space allotted to devices and we can already see operators scaling back on device display space as newer thematic zones are added to the store.

Events don’t always draw customers to the store

Source: TM Forum

There are still positive outcomes in providing the public, in particular older customers, with educational resources to improve their digital literacy. A Vodafone UK executive noted that since lockdown customers who realised they were not as tech literate as they thought they were have subsequently come into the store to speak with tech experts.

Operators’ sustainability programmes and adoption of circular economy measures in stores such as handset repair, recycle, refurbishment and re-sale is one potential new use case for telecom stores. Orange’s Re program is an example of this.

Stores still serving a purpose for the moment

Operators are still looking for innovative ways to encourage customers in to the store, and some use promotional offers to stimulate purchase during low footfall periods. For example, in January 2021 Bouygues Telecom in France offered a €50 discount to customers entering the store between 9am and 11am who subsequently purchased a mobile phone and subscription package.

European demographics and aging customer profiles could also mean European customers may prefer to rely on stores to introduce them to new device formats, solutions for the home, or wearables to support personal health.

In Africa and the Middle East, operator stores can also be a destination for paying utility bills such as (water, electricity) and telcos have sought to manage this through self-care kiosks and more ideally electronic and mobile payments. While kiosks are useful in handling low level tasks, they also require regular maintenance resource which must be factored into their deployment.

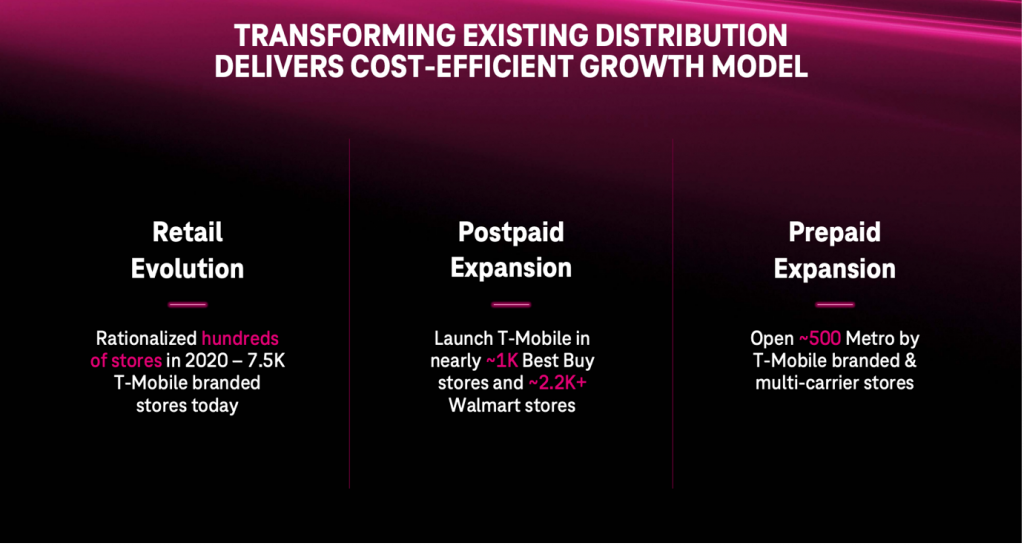

At an in-market competition level, as new players enter the market or territories, they may require retail real estate to establish their presence. For example, T-Mobile USA is now targeting smaller rural markets where it is underrepresented but which (according to the operator) account for 50 million households or 40% of all households in the US. Speaking at Deutsche Telekom’s capital markets day in May 2021, CEO Michael Sievert said the operator would be smart about how it will expand its physical footprint over the next five years, building hundreds of new stores in small towns and rural areas but also using partners such as Best Buy and Walmart to expand its retail distribution presence.

In towns too small to support a retail store, Sievert spoke of using Hometown Experts or individuals dedicated to supporting smaller communities. The operator aims to grow its small and rural market share to 20% over the next five years.

Vodafone CEO Nick Read has spoken of a similar model in Spain for promoting fixed broadband. Similarly in Thailand, AIS deploys direct sales teams to smaller markets or temporary sites providing them with a mobile app to transact sales of devices, airtime and register new customers.

T-Mobile USA expansion to smaller rural markets

Source: Deutsche Telekom, Capital Markets Day – May 2021

Even Tesla re-thought its store model

In 2019, Tesla reversed its decision to close the majority of its 378 stores and instead opted to close half of the stores the car maker originally had planned to close. With electric cars cost is a fundamental barrier to customer adoption and the company initially believed the closure of most of the stores would achieve a 6% reduction in the price of a Telsa car. Stores slated for closure included those with less foot traffic, even if they had a high proportion of in-store sales. However, given most customers like to sit in a car and get a feel it, this may have been a step too far even with Tesla’s seven-day return policy – a policy they felt made the store visit less necessary. The decision to reverse the closure of almost half the stores resulted in a 3% reduction in price of the Tesla car – instead of the 6% reduction under the initial planned closures.

Stores in high visibility locations initially closed due to “low throughput” were reopened, highlighting the usefulness of the store as a billboard for the brand. Tesla reiterated that sales would continue online worldwide and prospective customers entering the store would be “shown how to order a Tesla on their phone in a few minutes.” Tesla believes its seven-day or 1,000 miles returns policy is enough to remove the need for a test drive (effectively a store visit), however cars would still be available for test drive onsite and a small car inventory (stock) level would be maintained to serve customers who want to purchase and drive away immediately.

Table of Contents

- Executive Summary

- Table of Figures

- Introduction

- Impact of online on the high street

- Target: Innovation in fulfilment

- AIS Thailand: Building experiences

- Expanding into virtual shopping

- AIS experiments in physical retail

- My AIS app becomes a super app

- South Korea’s unmanned stores

- LG Uplus

- SK Telcom’s retail network and unmanned store

- Vodafone: Focusing on efficiencies

- Vodafone Digital First

- Vodafone experience store: Billboards aligned to be digital first

- UK franchising partner model: Local, smaller towns

- COVID-19 and Vodafone store re-format continues

- Orange France: How to leverage pop-ups

- Moving from physical to digital sales

- New digital skill sets and KPIs

- La Petite Boutique stores: Promoting suburban and rural fibre broadband take up

- Altice Portugal: MEO proximity stores

- Live streaming video chat

- Safaricom: Working with dealers

- Balancing digital first and a dealer network

- Experience stores

- US: AT&T and Verizon’s hybrid approaches

- AT&T restructures its corporate store footprint

- Verizon: Touchless Retail

- Three Ireland: Connected lifestyle stores

- Conclusions and recommendations

- Recommendations