Login to access

Want to subscribe?

This article is part of: Network Innovation

To find out more about how to join or access this report please contact us

Cloud native networking offers operators a promise of efficiency, automation and innovation to underpin their future in the coordination age. But it should also mean a new operating model, new skills and organisation that few feel they are ready for.

Cloud native networking: Telecoms’ latest adventure

As a term, cloud native has currency in telecoms networking. 5G has contributed to the recent industry-wide interest in adopting cloud native applications for networks. This is because the 5G standalone core networks (5G SA) that operators are now planning (and some have started deploying) are intended to run as software that is specified and architected following cloud native principles.

Within telecoms, thinking about cloud native tends to centre on the next phase of moving network functions into a software environment, building on lessons learned with NFV/SDN. Viewed from this perspective, cloud native is the next step in the telecoms industry technology evolution: from analogue to digital circuit-switched to digital IP to virtualised to cloud native.

Telcos’ business model is reaching end-of-life

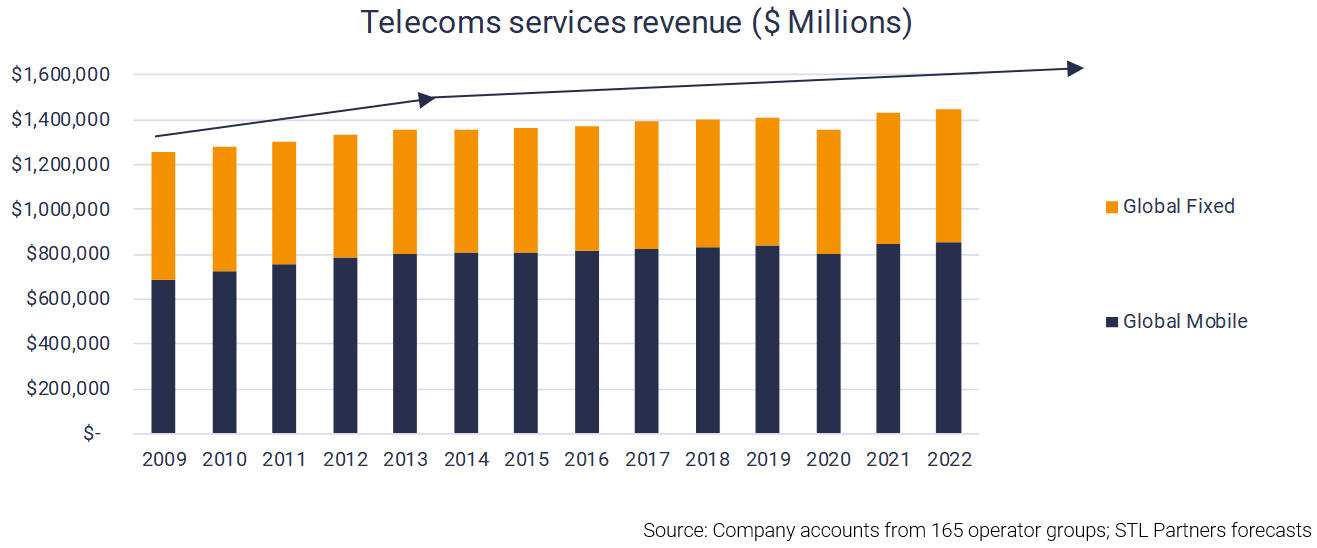

The rise of mobile telephony and fixed and mobile broadband means that telecoms operators have enjoyed 20 years of strong growth in all major markets. That growth has stalled. It happened in Japan and South Korea as early as 2005, in Europe from 2012 or so and, market by market, others have followed. STL Partners forecasts that, apart from Africa, all regions will see a compound annual growth rate (CAGR) below 3% for both fixed and mobile services for the next three years. Ignoring pandemic ‘blips’, we forecast a CAGR of less than 1% per annum globally. This amounts to a decline in real terms.

The telecoms industry is reaching the end of its last growth cycle

The telecoms industry’s response to this slowdown has been to continue to invest capital in better networks – fibre, 4G, 5G – to secure more customers by offering more for less. Unfortunately, as competitors also upgrade their networks, connectivity has become commoditised as value has shifted to the network-independent services that run over them.

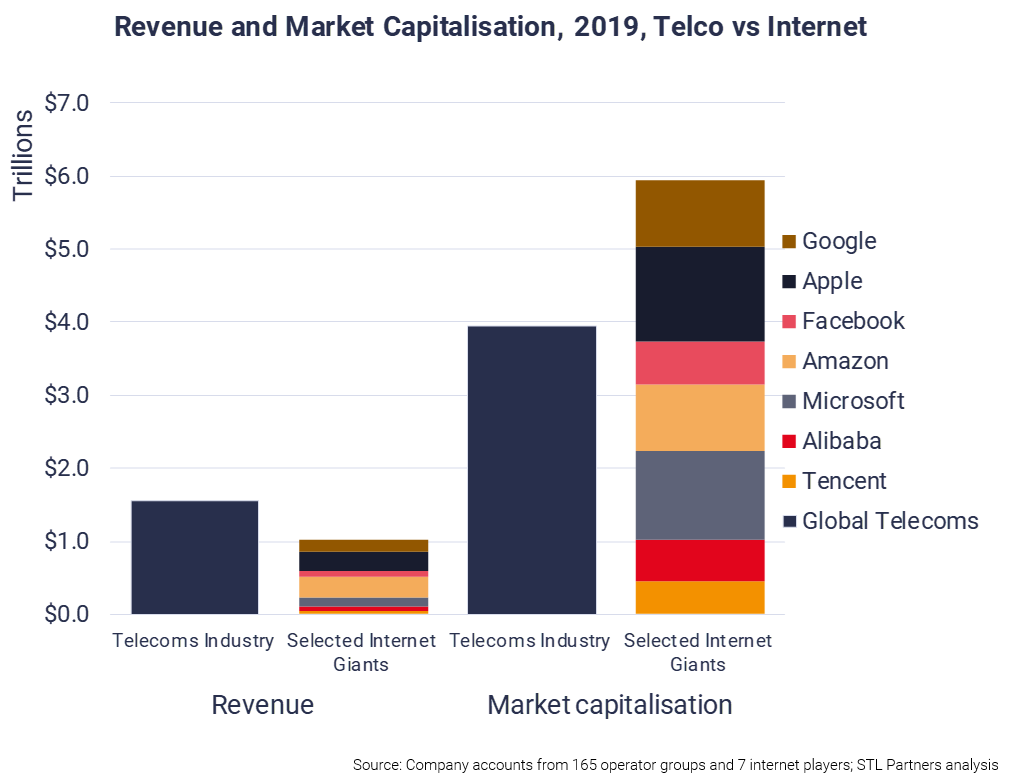

In other words, the advantage that telcos had when only telecoms services could run on telecoms networks has gone: the defensive moat from owning fibre or spectrum has been breached. Future value comes from service innovation not from capital expenditure. The chart below sums the problem up: seven internet players generate around 65% of the revenue generated by 165 operators globally, but have a c. 50% bigger combined market capitalisation. This is because the capital markets believe that revenue and profit growth will accrue to these service innovators rather than telecoms operators.

Tech companies are more highly valued than telcos

Understand, then emulate the operating model

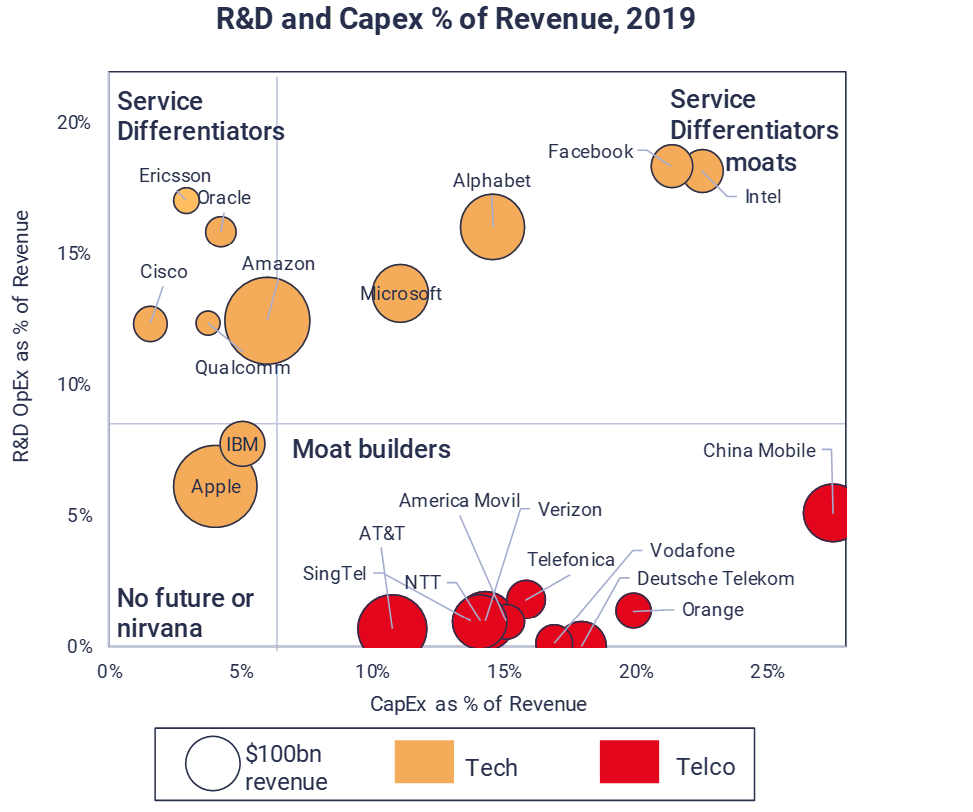

Operators have been aspiring to learn from technology firms so they can transform their operations and services. But changes have been slow, and it is difficult to point to many ‘poster child’ operators that successfully made a move beyond pure telecommunications. Partly this is due to a mismatch between corporate announcements and their investment policies. Too often we hear CEOs express a desire to change their organisations and that they intend to offer a host of exciting new services, only to see that aspiration not borne out when they allocate resources. Where other tech companies make substantial investments in R&D and product development, operators continue to invest miniscule amounts in service innovation (especially in comparison to what is poured into the network itself).

Telco vs tech-co investment models

STL Partners believes that many of the network-related activities that will enable operators to reduce capital expenditure, such as cloud-native networking, will also enable them to automate and integrate processes and systems so they are more flexible and agile at introducing new services. So, an agile software-oriented infrastructure will enable changes in business processes such as product development and product management, partnering, and customer care – if management prioritises investment and drives change in these areas. Cloud native business practices and software were developed by technology companies (and then widely adopted by enterprise IT functions) as a means to deliver greater innovation at scale whilst reducing the level of capital relative to revenue.

Our belief is that financial and operational developments need to happen in unison and operators need to move quickly and with urgency to a new operating model supported by cloud native practices and technology, or face sharp declines in ROI.

Table of Contents

- Executive Summary

- Table of Figures

- Preface

- Cloud native networking: Telecoms’ latest adventure

- Telcos’ business model is reaching end-of-life

- Understand, then emulate the operating model

- The coordination age – a new role for telcos

- 5G: Just another G?

- Cloud native: Just another technology generation?

- Different perspectives: Internal ability, timing …and what it means to be a network operator

- Organisational readiness, skills and culture

- Target operating model and ecosystem

- Assembly versus Engineering

- Wider perceptions across the business functions

- Operator segment 1: Risk of complacency

- Operator segment 2: Align for action

- Operator segment 3: Urgent re-evaluation

- Operator segment 4: Stay focused and on track

- Appendix 1

- Interviewee overview

- Appendix 2

- Defining Cloud Native

- There is consensus on the meaning of cloud native software and applicability to networks

- Agreement on the benefits: automation at scale for reliability and faster time to market

- …and changing supplier relationships