Login to access

Want to subscribe?

This article is part of: Executive Briefing Service

To find out more about how to join or access this report please contact us

The UK’s vote to leave the European Union came as a shock to many, and has complex ongoing consequences. We summarise briefly what happened, possible scenarios, and give our initial view on the implications for telcos, their business partners and the innovation ecosystem.

Published here is our outline of what has happened in the UK, what still has to happen, and the near-term consequences.

The full report further outlines scenarios for how the saga may play out, and explores opportunities and threats for operators and technology partners in the UK, the EU and beyond.

Introduction: What actually happened in the UK?

Why was a vote called?

British Prime Minister David Cameron first considered a referendum on European Union membership in 2012, with the idea that it might be a way to generate support from Eurosceptic members of his own Conservative Party. In January 2013, Cameron made a two-fold promise that, should his party win a majority at the 2015 general election, the Government would attempt to negotiate more favourable arrangements for Britain’s EU membership, and subsequently hold a referendum to decide whether the UK should leave or remain part of the EU.

In May 2015, the Conservative Party won the general election, and David Cameron reaffirmed his pledge. By February this year, Cameron had announced the outcome of a renegotiation of the UK’s EU membership, and confirmed that a referendum would take place on 23 June. The question chosen to appear on the ballot paper was: “Should the United Kingdom remain a member of the European Union or leave the European Union?”

The result

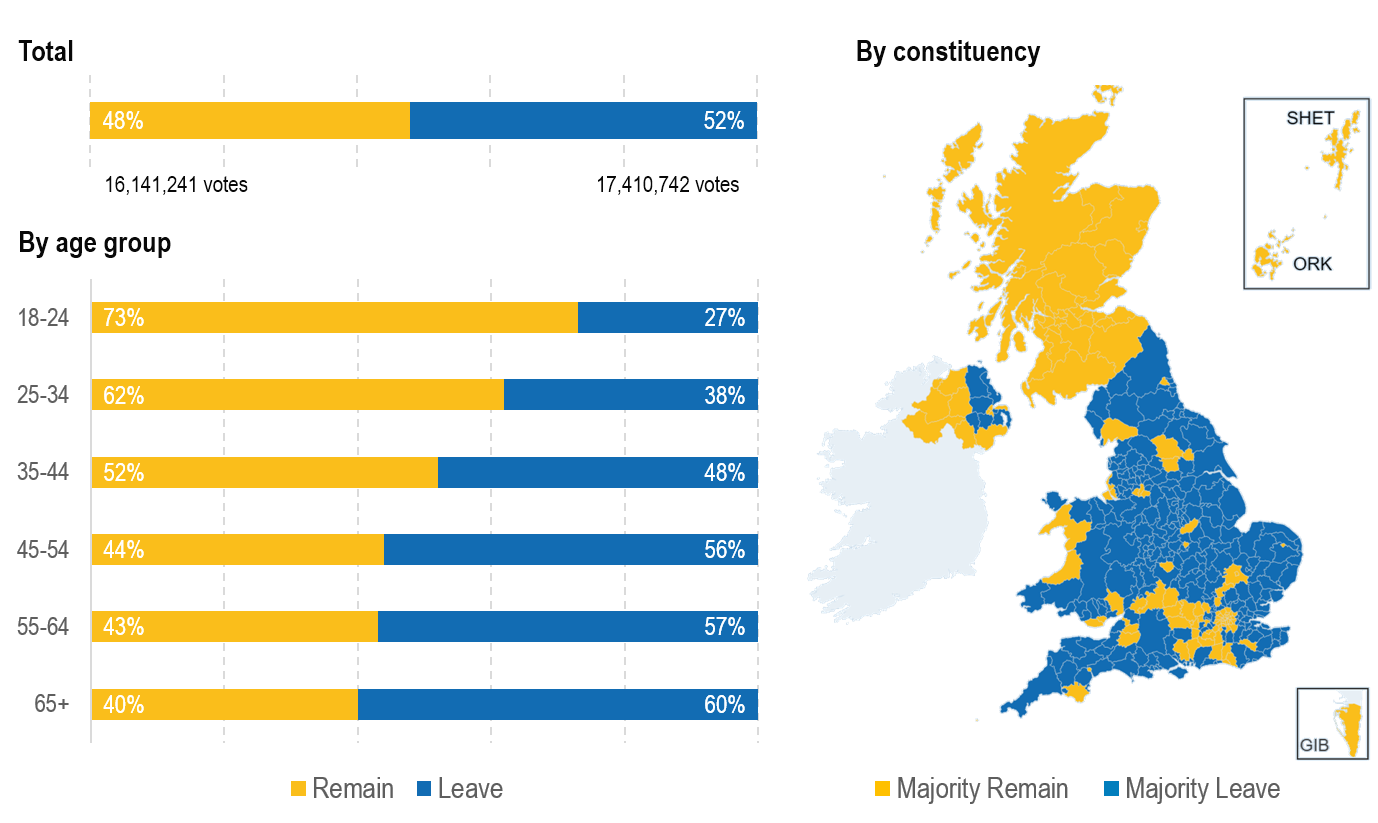

Figure 2: The EU referendum – how Britain voted

Source: Lord Ashcroft Polls, BBC

46.5 million voters were eligible to vote in the referendum, of which 33.6 million voted. At 72%, this represents a high turnout.

Of those voting, 17.41 million (52%) voted to ‘Leave’ and 16.14m (48%) voted to ‘Remain’ in the European Union, a majority of 1.27m in favour of leaving. Immediately after the result, Prime Minister David Cameron announced his resignation, to be effective once a new Conservative party leader was chosen.

Polling reports by voting constituency show a relatively consistent pattern of a ‘Leave’ majority in most of England and Wales, with a ‘Remain’ majority in London, Scotland, major university cities, and Northern Ireland. Surveys suggest that the ‘Remain’ voters were on average younger and better educated.

Why did the UK ‘Leave’ campaign win?

The reasons behind the victory of the ‘Leave’ campaign are complex and probably not yet fully understood – the result was as much of a shock in the UK as the rest of the world.

Nonetheless, to help set the outcome in context, we shall carefully try to piece together some insight into the main drivers combining our understanding of the events, supported by findings from one published post-vote survey, hopefully without touching still sensitive nerves in the UK and elsewhere.

The primary reason given by ‘Leave’ voters was “the principle that decisions about the UK should be made in the UK”. More qualitatively, there are concerns too about the future intent of the EU to integrate even more deeply, and even many ‘Remain’ voters dislike the perceived distance and inefficiency of the EU itself.

Migration was also cited as the second most important reason to vote ‘Leave’, and there has recently been a significant increase in EU migrants coming to work in the UK. While some areas have felt the impact of the inflow of migrants more than others, net EU immigration amounted to 0.3% of the population last year. The voters’ concern was of ‘uncontrolled’ future migration.

The ‘Leave’ campaign tapped into and amplified into both democratic and migration concerns deftly with the clear and emotional central promise to ‘take back control’, and spoke in everyday language. Boris Johnson, the former Mayor of London joined the campaign in February, and gave it a better known and well liked face.

In contrast, the ‘Remain’ campaign lacked clarity and cohesion among its leaders and messages, particularly around controlling immigration. It was also neutralised on the issue of the likely economic damage of Brexit by the accusation of running ‘Project Fear’ – claims of impending disaster to scare voters onto its side.

The Labour half of the ‘Remain’ campaign was accused of lacking conviction. The Labour party leader, Jeremy Corbyn is now facing his own “Jexit”, as 172 Labour Members of Parliament (c.75%) delivered a non-binding “no confidence” vote on his leadership. It has even been suggested that Mr Corbyn voted for Leave. (Ironically, a similar rumour suggests Boris Johnson voted ‘Remain’.)

While the overall tone of the campaign became rather toxic and facts became a casualty to both sides, the ‘Leave’ campaign cut through with its clearer message, emotional appeal, and better-worked rhetoric.

Many surveyed said they had come to the decision to support ‘Leave’ before all the campaigning of the last few weeks, based on the view that the benefits of taking back control of decisions and migration would be worth the (hotly disputed) risks of whatever economic consequences there may be. The argument is that in the medium term, the UK will be able to negotiate better trade deals outside Europe, no longer held back by the less agile EU, with its 27 different national interests to complicate every deal.

There is also a sizeable body of disaffected and disenfranchised voters in the UK, more typically (but not exclusively) less affluent and living in rural areas and small towns, who feel they have been talked down to and left behind by the metropolitan, educated elite, including politicians, business leaders, economists and other experts. The EU vote was an opportunity to protest, and the warnings of economic ruin by ‘the elite’ simply strengthened their resolve to give ‘the establishment’ – and ‘the elite’ – a metaphorical ‘kick’.

What are the consequences – in the UK and beyond?

UK politics will be in a muddle for a while, and it is far from clear what will happen

You might think that the vote has been cast, and that would be that: the UK is out of the EU. This is far from the case. There is considerable opposition to leaving, and many procedural opportunities for further twists and turns which we outline in this section. Our aim is to help explain why there may be a long delay before anything much more tangible happens, and some of the factors that might drive the emergence of different scenarios.

Before anything much more can be resolved, Britain needs a prime minister. Constitutionally, David Cameron remains in office until his successor takes over, but there are obvious limits to his authority as a ‘lame duck’. The logic of the constitution is such that the Conservative Party first needs to choose a new leader, who would automatically become prime minister by virtue of the Conservative majority in the House of Commons.

For exit to actually happen, the UK government must send the European Council a notification under Article 50 of the Lisbon Treaty. Once the notification is received, a clock is set running on the withdrawal process – the parties then have 2 years to negotiate terms. If there is no agreement within that time, the European treaties cease to apply to the withdrawing state in a so-called “hard exit”.

Cameron has stated that he will not give this notification, leaving this for his successor on the grounds that having resigned, he no longer has the legitimacy to take such a historic step. This means that the situation is currently on hold. Some lawyers argue that the Article 50 notification would need a vote in the House of Commons, which has a substantial majority in favour of remaining in the European Union, in a further complication. It may also be covered by the principle that the Westminster parliament only acts on Scottish affairs with the Scottish government’s consent, which is very unlikely to be given. This interpretation, however, is controversial.

Meanwhile, the opposition Labour Party is in a similar state of crisis, as its MPs try to remove the party leader. Because that party’s rules require a full party conference to sack the leader, and then an election by the members, it is possible that they might not be able to remove him before the conference in September, unless he chooses to resign. Even then, he might stand for election as his own successor.

As a result, it is unlikely that much can be decided until the parties have resolved their own internal crises. Once this has happened, though, the UK will have an unelected prime minister and a parliament largely elected on a platform of staying in the EU. Therefore, it may be necessary to call a general election (since 2011, this needs a 2/3 majority of Parliament, so could be problematic in itself).

A prime minister unwilling to leave the EU might use this as a way to back down from the referendum, on the basis that the electorate had spoken once again and had evidently changed its mind. Alternatively, he or she could use it to seek a mandate to implement their chosen version of Brexit. In the event that the Article 50 notification is issued, it is almost certain that the Scottish Nationalist Party would seek a second referendum on independence from the UK.

The UK in general: a state of shock

It is hard to gauge the knock-on impact of the vote on the wider population, other than to say that the STL Partners team has never experienced such an emotive and divisive political issue. There are disagreements within families, between friends, within communities, and across the nation.

There have been increases in reported racist crimes and confrontations, and the vote and its political fall-out dominates the news coverage.

There is not rioting on the streets, but there is a sense of shock, anger and disbelief among many on all sides. Perhaps the ongoing drama of the political fall-out in Westminster and Brussels, and a general weariness with the whole situation, are diverting the tensions.

We hope that things will calm down quickly, but there may well be months of more stress ahead. In the long term, the divisions between the predominantly ‘Remain’ areas like London and Scotland, and strongly ‘Leave’ rural areas and towns need to be addressed, but the solutions are not obvious. This vote has merely highlighted and amplified the differences, and Brexit itself does not offer a solution.

Economic Uncertainty: threat and opportunity

The primary macro-economic impact so far has been a deep devaluation in sterling. This will move the balance of payments on current account, heavily in deficit (i.e. imports exceed exports) at the moment, towards balance, as UK exports get cheaper and imports dearer. The consequences of moving towards balance will depend on how this happens.

One possibility is that British exports might be quite price-elastic. In this case, export volumes would rise more than import prices, and the devaluation would therefore increase aggregate demand and GDP. However, if they are less price-elastic, the increase in export volumes might not be enough to outweigh the rise in import prices, and the impact would be negative.

It is historically quite common that economies going through a major devaluation experience both, in the so-called J-curve effect. In the short term, import prices rise immediately, but it takes time to increase export volumes, and there is a recession. In the medium term, exporters adjust to the new exchange rate and there is a recovery. Service exporters – a very important category – cannot simply sell more units (nobody consumes more corporate lawyering because it is cheap), but have to gain new customers or sell more complicated services to existing ones.

If exit itself is disruptive to trade with the EU because of ill-feeling on either side (as might seem likely) or regulatory/non-tariff barrier issues, this would also make for such a scenario. Another, much more negative possibility, would be a recession in the domestic economy that reduces demand for imports and drives the current account into balance that way.

A third, even worse possibility would be a financial markets-driven “sudden stop”, in which the inflow of financing into the UK (the capital account surplus) would slow down dramatically. The current account would move into balance because importers became credit-rationed, resulting in a deep and rapid recession. Much depends on what the actual UK-Europe trade relationship turns out to be, and on the price elasticity of demand for UK exports.

What is very likely is that at least 2 years of intense uncertainty are in prospect, and during this time we expect many UK (and some EU) investment decisions to go on hold. It may be more likely that the UK experiences a classical recession, led by investment decisions in cyclical sectors like construction, and that this leads to a smaller current account deficit, rather than a change in the current account leading to a recession. Heavy selling on the stock market has focused on cyclical and consumer stocks like banks, airlines, housebuilders, and supermarkets. This implies the market is pricing in such a scenario.

In the telecoms sector, the UK would feel the effect on sales of flagship smartphones in mobile and big TV bundles in fixed – i.e. big ticket discretionary spending, the sort of thing that is likely to go first. Virgin Media’s £3bn Project Lightning fibre roll-out is an investment that might be affected, as owners Liberty Global have other markets they could deploy the CAPEX in.

As for investment into the UK, the devaluation renders UK assets significantly cheaper, and permits buyers who finance themselves in the UK to lever up more – a given amount of foreign-denominated equity is now worth more in sterling, so a larger loan can be floated at the same leverage ratio. The fundamental decision is therefore whether this advantage is worth the macro risk. The possibility of a nasty shock – such as the failure of a systemically important financial firm – can’t be ruled out.

For telcos in particular, a crucial issue is that their infrastructure is almost exclusively sourced from markets that trade in dollars or euros, so capital spending will be under significant pressure. Infrastructure sourced from China is paid for in dollars. Ericsson reports significant exchange rate adjustments in its accounts, suggesting that it gets paid in dollars and converts to Swedish kroner, while Nokia (plus ex-Alcatel) is of course in the eurozone. As a result, capital investments in the UK are financed in foreign currency and repaid out of sterling cashflows, so they will be significantly more expensive in future.

Longer-term impact will be overwhelmingly determined by the future shape of UK-European trade. This ranges from neutral – in the case where the UK stays, or shifts to a “Norwegian” relationship under the EEA Treaty – to seriously negative – in the “no deal” case where the UK ends up operating under WTO most-favoured nation tariffs. These are as high as 16% in the automotive sector, one of the biggest UK export lines of business (this Wall Street Journal app is invaluable here). We explore these scenarios in greater detail in the Scenarios section below.

Any upside for the UK is dependent on a substantial re-orientation of trade to extra-European markets; two of the biggest, China and Brazil, have their own problems in the short term.

- Executive summary (not published here)

- Introduction: What happened?

- Why was a vote called?

- The result

- Why did the UK ‘Leave’ campaign win?

- What are the consequences?

- UK politics will be in a muddle for a while

- The UK in general: a state of shock

- Economic Uncertainty: threat and opportunity

- Possible scenarios (not published here)

- Scenario 1 – Hard Exit

- Scenario 2 – Boris Johnson’s Norway

- Scenario 3 – No Exit

- Scenario 4 – Rolling Crisis

- Consequences for telecoms – in the UK, the EU, and beyond (not published here)

- Regulation

- Customers: Finserv

- Customers: Automotive and Industrial

- Customers: Media and TV

- What should TMT leaders do? (not published here)

- Don’t give up on transformation

- It could happen to EU

- The least disruptive possible outcome is a de-escalation

- The danger of a run on the skills bank

- Don’t catch a falling knife

- Figure 1: Summary Scenario Impacts for the Telco Industry

- Figure 2: The EU referendum – how Britain voted

- Figure 3: BT slides, Equinix soars