Strategy 2.0: Google’s Strategic Identity Crisis

Google’s shares have made little headway recently despite its dominance in search and advertising, and it faces increasing regulatory threats in this area. It either needs to find new sources of value growth or start paying out dividends, like Microsoft, Apple (or indeed, a telco). Overall, this is resulting in something of a strategic identity crisis. A review of Google’s strategy and implications for Telcos. (March 2012, Executive Briefing Service, Dealing with Disruption Stream).

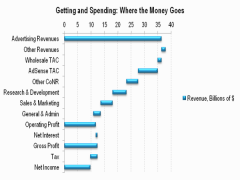

Google’s Advertising Revenues Cascade