CDN 2.0: Report and analysis of the event

CDN 2.0: Event Summary Analysis. A summary of the findings of the CDN 2.0 session, 10th November 2011, held in the Guoman Hotel, London

CDN 2.0: A Summary of Findings of the CDN 2.0 Session Presentation

CDN 2.0: Event Summary Analysis. A summary of the findings of the CDN 2.0 session, 10th November 2011, held in the Guoman Hotel, London

CDN 2.0: A Summary of Findings of the CDN 2.0 Session Presentation

Customer Experience: Delivering the Product Experience. Tribold VP Ernest Margitta presents a case study of how to defeat “product and service management chaos” at Sky TV. Presentation from EMEA Brainstorm, November 2011 The product defines the experience

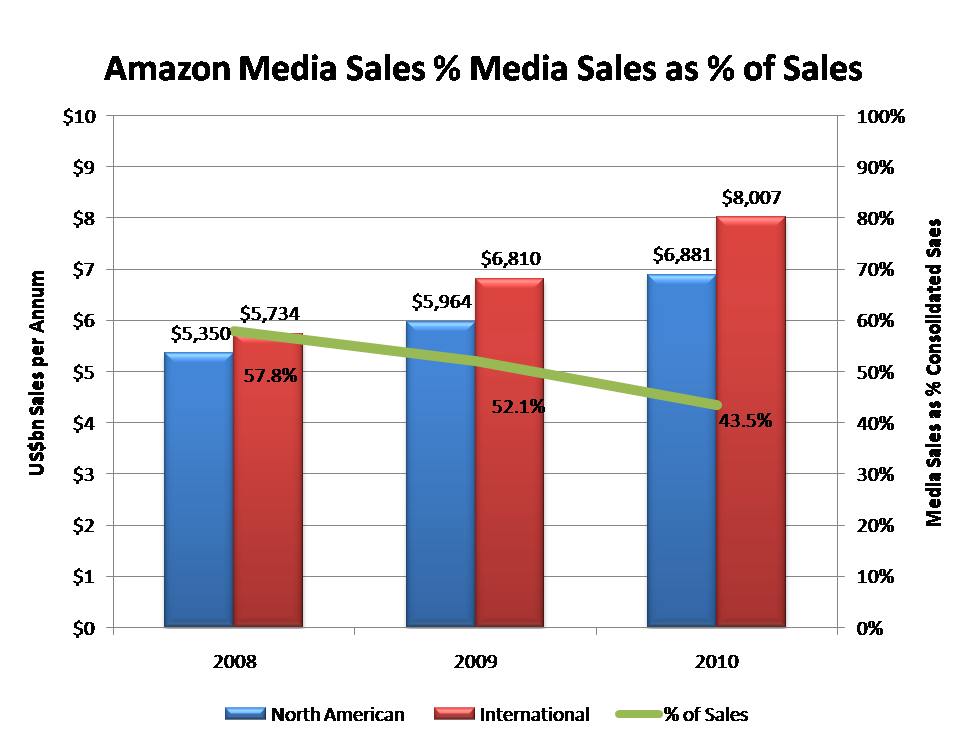

Amazon is probably the Internet’s best retailer. As it launches its own AppStore, we provide a detailed analysis of its digital media business and pick out the key opportunities it offers to content owners, network service providers and manufacturers. (March 2011, Executive Briefing Service, Dealing with Disruption Stream).

2011 sees the introduction of the UltraViolet digital locker platform by DECE, a consortium led by 6 of the 7 top Hollywood studios and backed by 50 cross-industry heavyweights, to support the transition of film and TV to online distribution. What opportunities will telcos miss if they fail to engage? (March 2011, Executive Briefing Service)

The sports network ESPN is a master of the paid content business model, building platform scale and success using premium content. What are the lessons from ESPN’s US and UK strategies for other service providers and content distributors? (September 2009)

As online video challenges traditional distribution models, both old and new suppliers are pushing into the value chain in the hope of grabbing a share of the emerging global market. But how will the market develop and which companies will be the ultimate winners?

STL Partners has analysed the potential of online video, identified possible market winners and losers, and set out three interlocking scenarios depicting the evolution of the market. In each scenario, the role of distributors is examined, possible threats and opportunities revealed, and strategic options are discussed. (March 2009)