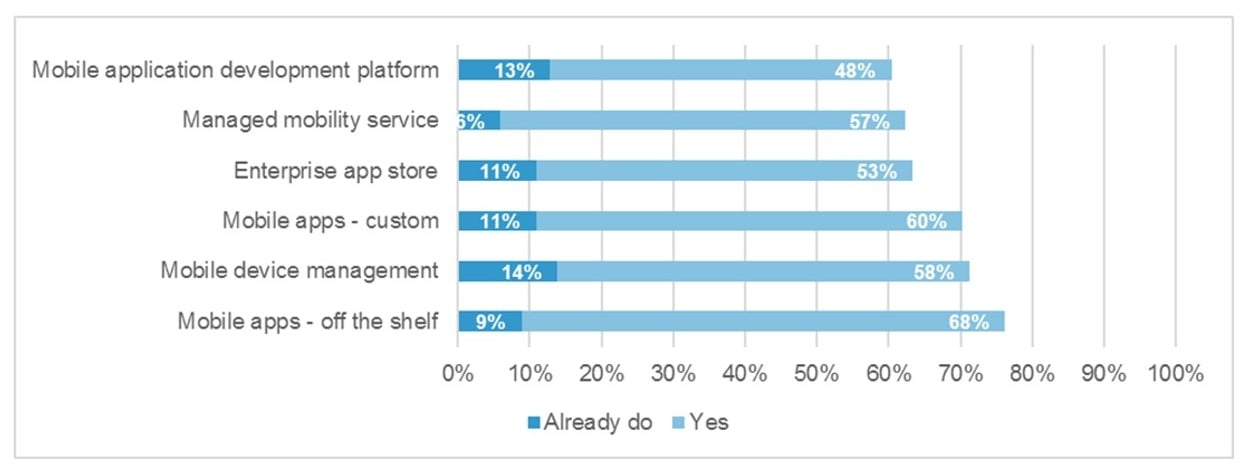

Enterprises are turning to mobility to transform their operations, creating a c.$50bn ‘Enterprise Mobility’ opportunity globally. There are four levels of engagement that telcos can adopt to start to capture a share of this market, and upgrade and repurpose their internal capabilities to deliver repeatable, high volume, customer-facing growth initiatives. They need tools, technologies and partnerships to provide the deep industry knowledge and mobile workforce expertise. This will allow them to take a defined proposition to market and evolve from being “just another channel” to originators and owners of intellectual property. (December 2013, Foundation 2.0, Executive Briefing Service, Cloud and Enterprise ICT Stream).

Enterprise Mobility Framework December 2013