Pursuing hyperscale economics

We evaluate the role of disaggregation and cloud native infrastructure and key breakthrough opportunities for network operators.

We evaluate the role of disaggregation and cloud native infrastructure and key breakthrough opportunities for network operators.

The success of digital economies is underpinned by the growth of the Internet. Our analysis of a number of economies shows that enlightened policy is more important than the wealth of the populace or any other measure. What are the key lessons?

Telcos, Internet and technology players, banks and payment networks have disruptive $billion opportunities to act as intermediaries / enablers in mobile commerce and personal cloud services, based on the appropriate use of customer data. This report is a unique and comprehensive strategic guide for success in these roles. It analyses the strategies of the main and cutting-edge players, and outlines key success factors in designing and delivering customer propositions, technology, organisation and value network strategies. It also includes evaluations of the related strategic opportunities of ‘raw big data’, professional data services, and internal data use, and a business model showing how one type of candidate for the intermediary role, a telco, could grow profitable new revenues equivalent to c.$50Bn (5% of existing core revenues) within five years. (October 2013, Dealing with Dsiruption Stream). Telco 2.0 Transformation Index Small

‘The Internet of Things’ (IoT) is one of the big ideas of the moment. But what are the areas in which value is being created now, and what is still technological hype? A summary of the findings of the Digital Things session at the NDE Executive Brainstorm, Silicon Valley, held at the InterContinental Hotel, San Francisco on the 20th March 2013. (April 2013)

Building Blocks Urgently Needed for IoT April 2013

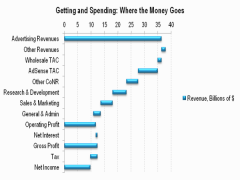

Google’s shares have made little headway recently despite its dominance in search and advertising, and it faces increasing regulatory threats in this area. It either needs to find new sources of value growth or start paying out dividends, like Microsoft, Apple (or indeed, a telco). Overall, this is resulting in something of a strategic identity crisis. A review of Google’s strategy and implications for Telcos. (March 2012, Executive Briefing Service, Dealing with Disruption Stream).

Google’s Advertising Revenues Cascade

As online video challenges traditional distribution models, both old and new suppliers are pushing into the value chain in the hope of grabbing a share of the emerging global market. But how will the market develop and which companies will be the ultimate winners?

STL Partners has analysed the potential of online video, identified possible market winners and losers, and set out three interlocking scenarios depicting the evolution of the market. In each scenario, the role of distributors is examined, possible threats and opportunities revealed, and strategic options are discussed. (March 2009)

There is incontrovertible evidence that “intelligence” always moves towards the edge of telecom networks. What can telcos do about it? (Mar 2009)

A review of key business opportunity and future business model scenarios in the core voice and messaging business. (November 2008)

Summary: This report examines future retail and wholesale business models for fixed and mobile operators offering high speed packet data services. This includes – but is not limited to – providing Internet access.

The report charts the next 10 years for fixed and mobile telecoms network operators as the viability of the current broadband business model is threatened by intense competition and falling prices in maturing markets, changing usage patterns, and the adaptation of new technologies. The report identifies and profiles a new $250Bn content delivery market opportunity. (April 2008)

An edited version of a keynote presentation of results of our Broadband Business Models survey into the industry’s future (November 2007, Executive Briefing Service, Future of the Networks Stream).