How to identify and meet new customer needs

This report outlines best practice in identifying and scaling new business opportunities, in terms of how to organise, the necessary culture, where to start, who to involve, and how to exit.

This report outlines best practice in identifying and scaling new business opportunities, in terms of how to organise, the necessary culture, where to start, who to involve, and how to exit.

2011 sees the introduction of the UltraViolet digital locker platform by DECE, a consortium led by 6 of the 7 top Hollywood studios and backed by 50 cross-industry heavyweights, to support the transition of film and TV to online distribution. What opportunities will telcos miss if they fail to engage? (March 2011, Executive Briefing Service)

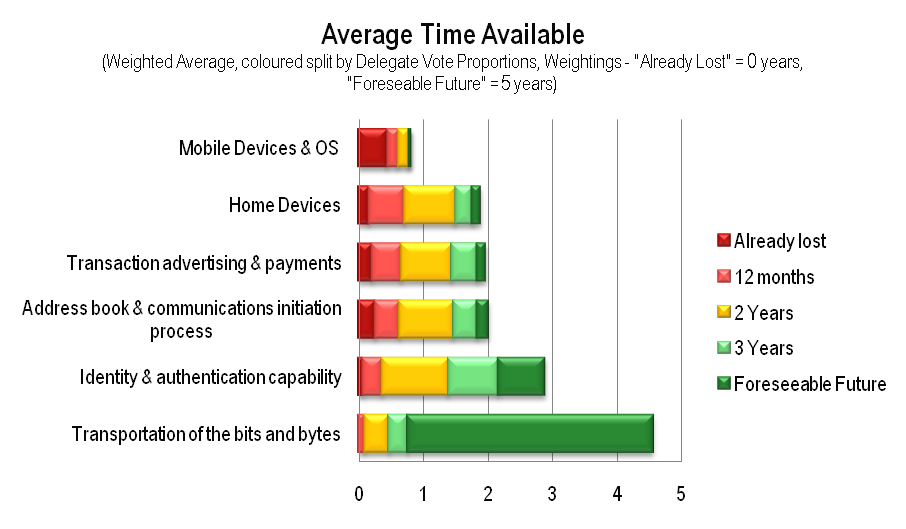

There’s less than 3 years for telcos to take advantage of key strategic ‘control points’ in their battle for sustainable growth in the communications and e-commerce markets, concluded delegates at the Telco 2.0 EMEA Brainstorm in November. How should they think differently about their value and where do they need to (re)focus their attention? Full report from the Brainstorm. (December 2010, Executive Briefing Service, Dealing with Disruption Stream, Executive Briefing Service)

A write up and analysis of new research plus participants’ and speakers’ views at the May 2009 Telco 2.0 Executive Brainstorm exploring the challenges of piloting Telco 2.0. (May 2009)

A write up and analysis of new research plus participants’ and speakers’ views at the May 2009 Telco 2.0 Executive Brainstorm exploring the challenges of new technology. (May 2009)

A write up and analysis of new research plus participants’ and speakers’ views at the May 2009 Telco 2.0 Executive Brainstorm exploring the challenges of making telcos better retailers. (May 2009)