Perspectives 2026: 26 industry predictions for the year ahead

STL Partners’ 26 predictions for 2026, focusing on change and growth in the telco industry

STL Partners’ 26 predictions for 2026, focusing on change and growth in the telco industry

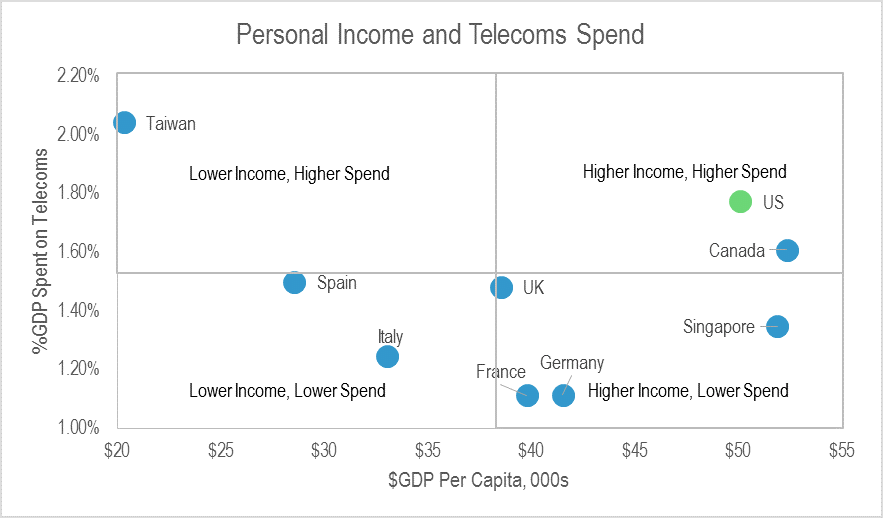

Disruptors from other industries are turning their attention to the mobile market. They can learn from the vibrant UK MVNO market.

DTW24 showed a telecoms industry ready to face reality and making quiet progress. This progress may not go far or fast enough to change the future of the industry, but either way AI will play a big role.

Telcos (and others) have had mixed results from their experience of ecosystems. We look at AT&T Community, DTAG’s Qivicon, GSMA Mobile Connect, TIP and Android to analyse success factors and approaches to maximise the potential of future ecosystem initiatives.

Passive network sharing is a well-established practice, but 5G may force telcos to consider more active network sharing to overcome financial,

technological and physical constraints. We explore 5G network sharing options and cost structures, drawing lessons from existing agreements.

Building a telco based on ‘free’ open source software is theoretically highly attractive to telcos, particularly those looking to increase their control over innovation and differentiation, and/or where cost reduction is critical. This report looks at how to address the challenges, identifies practical options and choices, and how, when and why to go about open source transformation in the real world.

T-Mobile USA’s ‘uncarrier’ strategy has delivered significant net additions, but is it a good strategy – and is the disruption promised by Softbank CEO Masayoshi Son already underway? We compare it to Free Mobile’s disruptive approach in France, and the results of its competitors’ responses.

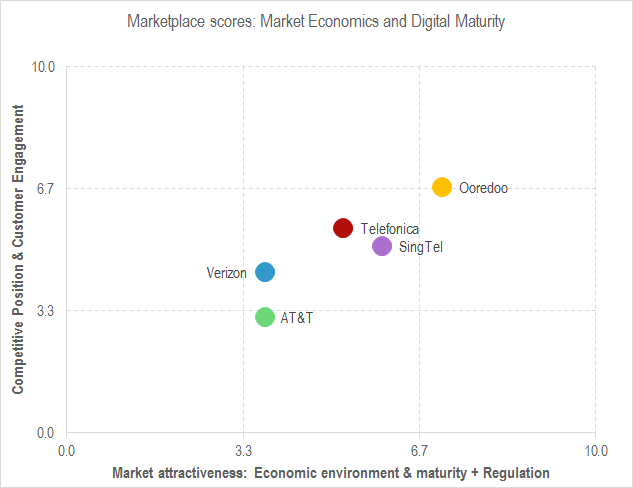

Operators face difficult choices on the best way to change their business models. In this note we analyse the approaches taken by AT&T, Verizon, Ooredoo, Singtel and Telefonica, extrapolate the options for all carriers, and offer a framework to help managers define the right new business model goal for their organisation.