Digital Commerce: Time to redefine the Mobile Wallet

The ‘Mobile/Digital Wallet’ needs to evolve to support authentication, search and discovery, as well as payments, vouchers, tickets and loyalty programmes. Moreover, consumers will want to be able to tailor the functionality of this “commerce assistant” or “commerce agent” to fit with their own interests and preferences. Our report and analysis of the Digital Commerce 2.0 Executive Brainstorm, 20 March 2013, part of the New Digital Economics Silicon Valley event. (April 2013, Executive Briefing Service, Dealing with Disruption Stream.)

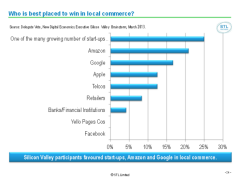

Who is best placed to win in local commerce April 2013