STL Partners believes that healthcare is a vertical that is well suited to telecoms operators’ strategic scope:

- Healthcare is a consistently growing need in every country in the world

- It is a big sector that can truly move the needle on telcos’ revenues, accounting for nearly 10% of GDP globally in 2018, up from 8.6% of GDP in 2000 according to WHO data

- It operates within national economies of scale (even if the technology is global, implementation of that technology requires local knowledge and relationships)

- The sector has historically been slower than others in its adoption of new technologies, partly due to quality and regulatory demands, factors that telcos are used to dealing with

- Improving healthcare outcomes is meaningful work that all employees and stakeholders can relate to.

Many telcos also believe that healthcare is a vertical with significant opportunity, as demonstrated by operators’ such as TELUS and Telstra’s big investments into building health IT businesses, and smaller but ongoing efforts from many others. See STL Partners’ report How to crack the healthcare opportunity for profiles of nine telecoms operators’ strategies in the healthcare vertical.

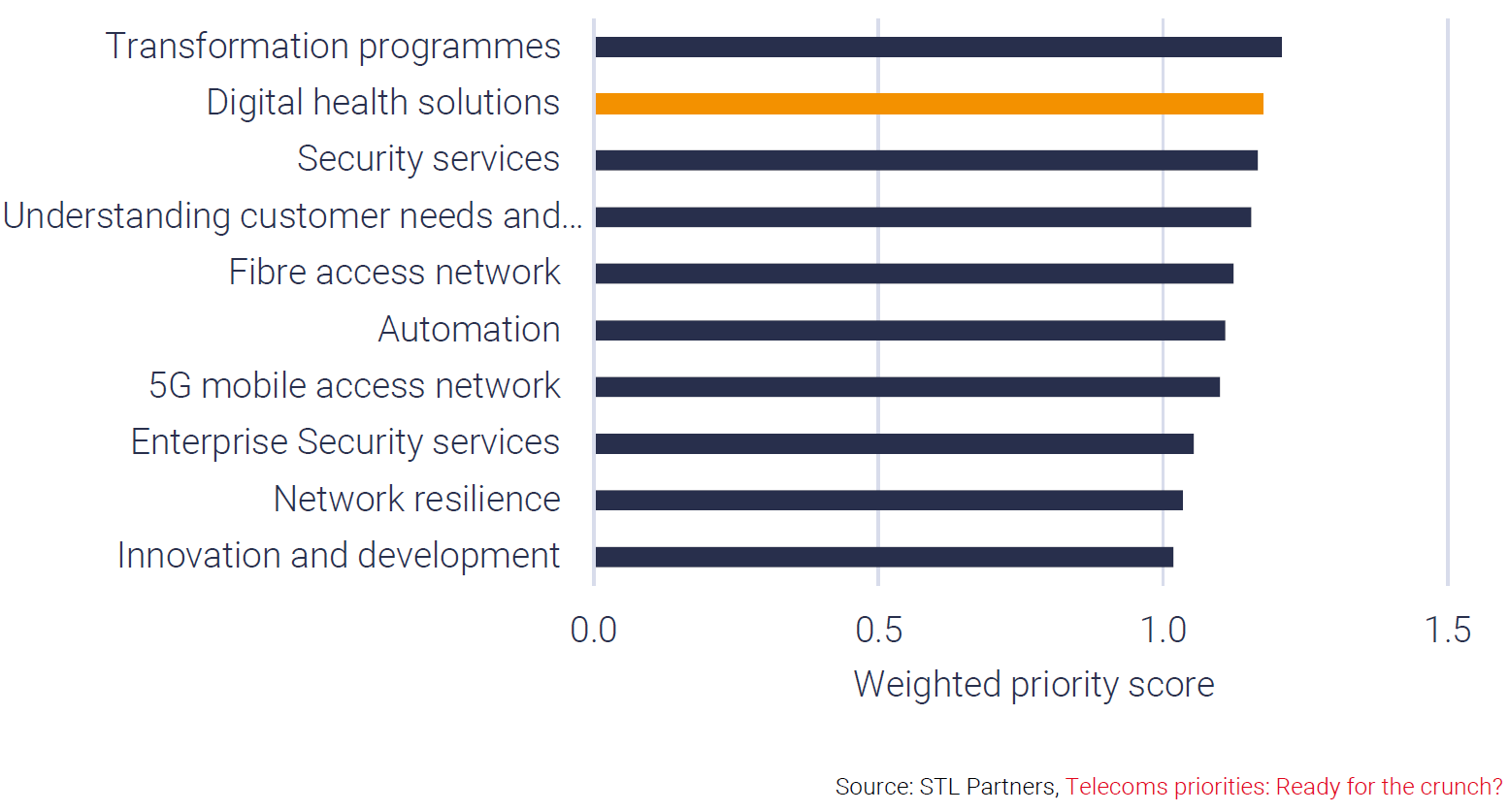

Our research into the telecoms industry’s investment priorities in 2021 shows that the accelerated uptake of digital health solutions throughout the COVID pandemic has only shifted health further up the priority list for operators.

See our other in-depth research on digital healthcare: