CBRS has enabled enterprises and services providers to leverage cellular technology for different use cases including private networks. However, as the shared nature of the spectrum continues to attract new players, it has also drawn criticism and started a wider discussion about the efficacy of this framework.

What is CBRS?

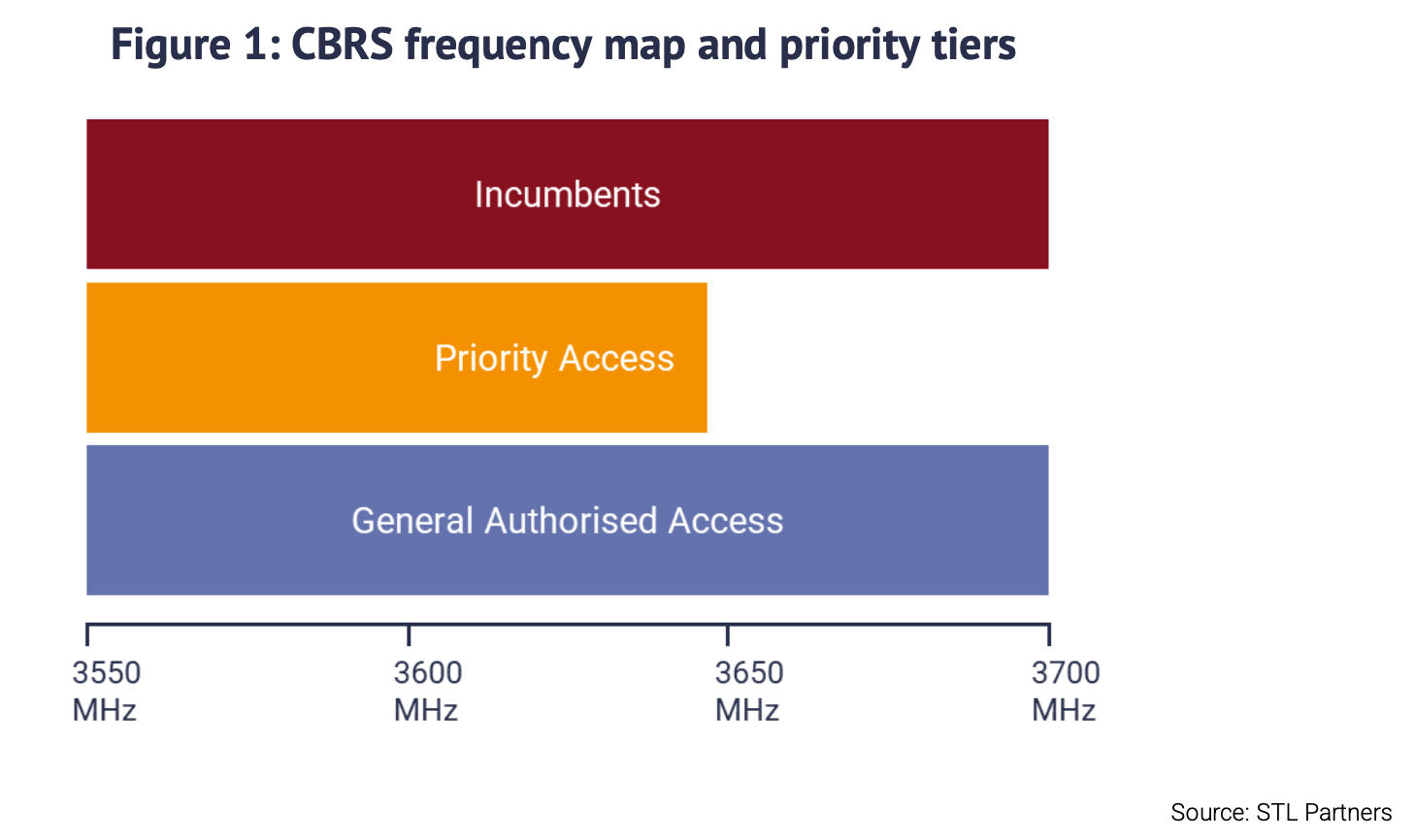

The FCC introduced the Citizens Broadband Radio Service (CBRS) to enable the use of LTE on the unlicensed spectrum of the 3.5Ghz band (3550 – 3700MHz). Industry bodies WinnForum and OnGo Alliance collaborated with the US Navy and other incumbents in the band to define the standards and encourage the adoption of the technology.

CBRS technology is based on opportunistic access to shared spectrum that is governed by a spectrum access management system. Rights to access the spectrum fall into one of three priority tiers: Incumbent Access, Priority Access, and General Authorised Access. Incumbent access has the highest priority to use the spectrum and it mainly includes the US Navy. In many locations across the country, the incumbents’ utilisation of the band is low and their impact on other users is limited. The Priority Access comes next, and it consists of users with acquired regional priority access licenses (PALs). The General Authorised Access (GAA) has the lowest priority and is only open to unlicensed users if the band is not occupied by the incumbents or PAL users. GAA users have access to 80MHz of the available spectrum, and up to the full 150MHz if the higher priority users are not present in the same location. The spectrum allocation and management among different users is controlled by a spectrum access system (SAS).

Figure 1: CBRS frequency map and priority tiers

Over the last two years, CBRS spectrum has been utilised in different use cases and across industries

By the end of 2020, the FCC concluded the auction of licenses for the PAL tier, awarding 20,625 Priority Access Licenses to 228 users and raising a USD4.4 billion. Each PAL offers 10MHz of unpaired spectrum and the PALs were awarded per county with a total of seven PALs available for every county. Spectrum allocation is generic and does not guarantee specific spectrum ranges for users. However, when deploying the network, users can still request specific ranges from their SAS and may get them if they are not used by incumbent users.

CBRS spectrum has supported many different use-cases, aside from that of private networks for enterprises. Mobile broadband and fixed wireless access (FWA) have been two of the top telco use cases for CBRS spectrum over the last three years. In fact, these use cases were the main drivers for spectrum acquisition by many of the largest license holders, which include mobile operators such as Verizon and T-Mobile, cable operators such as Comcast and Charter, Wireless Internet Service Providers (WISPs) such as Windstream and Nextlink Internet, and utility companies such as Alabama Power and San Diego Gas and Electric.

Remarkably, the CBRS PAL auction did not attract a wide engagement from enterprises looking to deploy private networks. This is primarily because the licenses cover an entire county, which is larger than most enterprises’ needs, and they couldn’t justify the cost premium. Reducing the size of the licenses may have made it easier for more enterprises to participate, however it would have complicated the auction and spectrum acquisition for many service providers, especially smaller and rural operators. Nevertheless, many enterprises are deploying and trialling private networks using the unlicensed GAA part of CBRS. Avoiding the licensing cost altogether has helped smaller enterprises and public services with limited fundings such as in education and healthcare.

As of November 2022, the OnGo Alliance reported that there were more than 285,000 CBRS base station devices (CBSDs) deployed, 187 different CBSD and 496 different end user client devices certified including traditional smartphones, IoT modules, gateways and security cameras. As of December 2022, the OnGO Alliance had more than 180 members representing the extensive CBRS ecosystem.

Figure 2: Examples of CBRS deployments across sectors

The sharing scheme has sparked a debate over the band utilisation

The US mobile industry is calling for more midband spectrum to support the ongoing 5G rollout. As demands for 5G services grow, it is becoming more difficult for regulators to easily find suitable bands, especially given that many mission-critical systems in defence, public safety, and satellite communications already run on such bands (it would be difficult to relocate them). As regulators and policymakers work on a new spectrum pipeline, sharing bands has emerged as a viable option, particularly in the 3.1-3.45 GHz band. The US policymakers are currently discussing the possibility of replicating the CBRS licensing model and repurposing that new band for commercial use.

The CTIA, which represents mobile network operators’ policy interests, has become critical of the CBRS model and the efficacy of spectrum sharing schemes in general in the fear that it will negatively impact telcos’ share of 5G licensed spectrum. The organisation is calling for more exclusively licensed spectrum models, arguing that interference from spectrum sharing results in low utilisation of the band and eventually low market demand. The organisation is also warns that the US risks falling behind in the 5G market without enough licensed midband spectrum.

However, the CTIA’s criticism is being challenged by a wide range of CBRS stakeholders advocating the success of the spectrum sharing technology in driving innovation across the telecoms industry and the positive progress in adoption it has made over the last two years. In November 2022, a letter signed by 25 firms and industry organisations including Amazon, Cox, Comcast and Federated Wireless, requesting a similar framework for the lower 3 GHz band was sent to the FCC and NTIA. The letter cited the rising number of deployments and the opportunities the technology had provided to various industries and stakeholders. Also, the Schools, Hospitals & Libraries Broadband (SHLB) Coalition asked legislators to adopt a balanced strategy that supports unlicensed use which can offer high-speed and low-cost broadband option to users who are underserved by public mobile networks. Similarly, the Wireless Internet Service Providers Association (WISPA) also wrote to regulators in support of the CBRS model and to ask for more shared spectrum bands.

The CBRS power limitation might also be re-examined as the spectrum sharing technology evolves

CBRS has lower transmit power limits than conventional cellular networks, which creates challenges for deploying outdoor and large area coverage. Many players including Dish, the second-largest bidder in the CBRS auction, has been advocating for higher-power operations in the CBRS band. Dish argues that increasing the power levels would result in a more efficient use of the spectrum and lower costs of deployment. This would also ensure the US’s 5G midband allocations stay similar to the rest of the world where 3.5 GHz is widely deployed for 5G.

On the other hand, certain participants, including T-Mobile, are opposed to raising the power for the CBRS, claiming that doing so will alter the nature CBRS and how it is being used. However, T-Mobile’s objection reflects its attempt to maintain its competitive advantage in 5G rollout as the carrier is holding a substantial share of midband spectrum. The FCC has not indicated a desire to change the power levels of CBRS operations, but the organisation has allowed Dish to test high-power CBRS operations in order to assess how they would affect GAA and PAL operations in terms of coverage, throughput and spectrum efficiency. The test outcomes will enable the discussion around power limits to include some fresh technical knowledge.

Regulators and stakeholders need to balance the risks and rewards of CBRS to push adoption

While CBRS remains a unique spectrum licensing model with some challenges, it is clear that it has indeed attracted a significant engagement from players across the value chain and from different industries, creating a growing and a dynamic ecosystem of stakeholders. The flexibility and the affordability of the technology have also made it accessible to a wider range of entities such schools, libraries, and hospitals either for innovating and solving immediate problems. This is unlike fully licensed models where the cost and process of acquiring spectrum might make it prohibitive for smaller enterprises with limited budgets. However, the model also shows the challenges facing regulators as they open up cellular spectrum to the wider market and attempting to accommodate the conflicting needs of various stakeholders including telcos while dealing with the scarcity of spectrum for 5G.

For spectrum sharing models such as CBRS to take off, regulators and different types of service providers need to work together to find a balanced licensing approach that can lower the cost of deployment and therefore encourage more engagement from enterprises but also maintain the reliability and quality of service guaranteed by licensed services.

Download this article as a PDF

Are you looking for specialist support in private networks?

Read more about private networks

Private networks insights pack

Our pack will provide you with a summary of insights from our private cellular networks practice

What is physical AI? Definitions, examples and implications for private networks

The term physical AI refers to the transition of AI from the mostly digital sphere into more real-world scenarios and physical processes.

Private 5G: Telcos trapped in the trough

The telecom industry seems to think that private 5G is failing as a driver of new growth. But this is more because this opportunity was recently the victim too much hype – growth is happening, and some players are taking advantage. Why are telcos still so frustrated?

The role of private networks in the utilities sector

As utilities companies pursue digital transformation, many are exploring the value of private networks in enhancing their operations