Download

Listen

The EU’s €20 billion AI gigafactory initiative will fund up to five large-scale AI compute facilities, each designed to support frontier model training with more than 100,000 advanced AI processors. The programme is intended to strengthen Europe’s domestic AI infrastructure and reduce reliance on non-European hyperscale capacity.

Introduction

The EU’s AI gigafactory programme is the most visible piece of European compute-infrastructure policy in a decade. The Commission is mobilising €20 billion of public and private capital to back up to five very large facilities, each designed to train the next generation of frontier AI models with more than 100,000 advanced AI processors per site. The programme is the centrepiece of the InvestAI initiative announced at the AI Action Summit in Paris in February 2025.

The rationale behind the policy is widely understood. Frontier AI development is currently concentrated in a small number of global labs, primarily outside Europe, including OpenAI, Anthropic, Google DeepMind and DeepSeek. While Europe has world-class AI research, a growing open-source ecosystem and one credible frontier AI player in Mistral, it is lagging in the infrastructure required to train and scale models. European companies needing very large-scale AI compute rely on US hyperscalers, creating exposure to non-European commercial priorities, supply constraints and policy decisions. The policy is therefore intended to address a clear strategic gap: ensuring Europe has the compute capacity and industrial base needed to participate meaningfully in frontier AI, rather than depending on external providers.

What is an AI gigafactory?

AI gigafactories are the tier above Europe’s AI factories. Where AI factories give start-ups, SMBs, researchers and public-sector users shared access to AI-optimised supercomputing, gigafactories tackle a different problem: the raw compute needed to develop, train and run frontier-scale AI models.

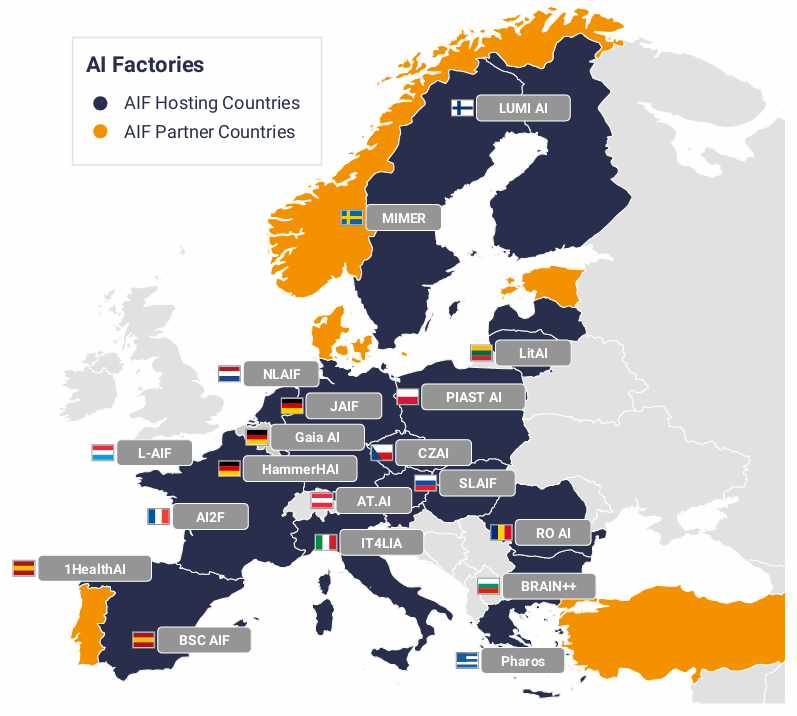

Figure 1: Proposed EU AI factories across Europe

Source: European Commission

The EU defines AI gigafactories as ‘advanced large-scale facilities with sufficient capacity to handle the complete lifecycle of very large AI models and applications, from development to large-scale inference in a single site’. In practice, that means four things in one place: AI-optimised compute at the scale of 100,000+ accelerator chips; a supporting data centre with high-capacity storage and networking; secure data spaces; and the power, cooling and supply chain to keep it all running.

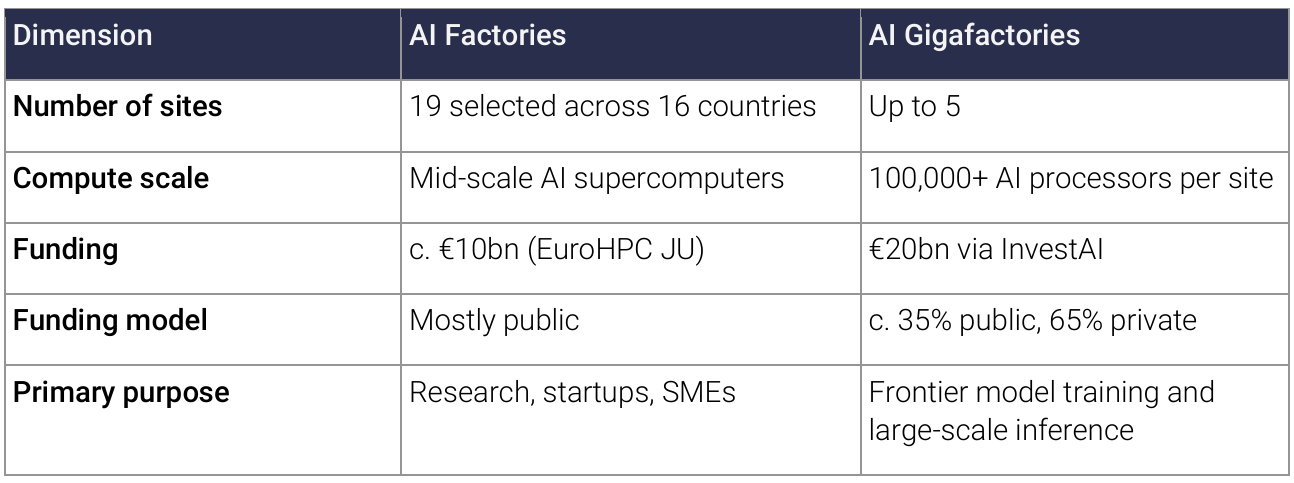

Figure 2: EU AI factories vs EU Gigafactories

Source: STL Partners

EU programme is moving towards procurement

The gigafactory programme is a central part of the EU’s AI Continent agenda and is being taken forward through InvestAI. Brussels has set a broader target to mobilise €200 billion of AI investment across the EU, with the €20 billion AI gigafactory facility acting as one of the anchor commitments.

The financing model is designed to crowd in private capital rather than rely solely on public funding. Under Council Regulation (EU) 2026/150, the Union contribution can cover up to 17% of the capital expenditure of the overall computing infrastructure of an AI gigafactory. Participating Member States must at least match the Union contribution, while the remaining investment and operational expenditure covered by the AI gigafactory consortium.

Demand for the programme has been strong on paper. The Commission’s informal call for expressions of interest closed on 20th June 2025 and attracted 76 submissions, covering 60 sites across 16 EU Member States, with proposed investments totalling more than €230 billion. The formal call for proposals has been delayed twice and is now expected in Q2 2026 (although as of May 2026 there has been no official update on timing), with selection decisions and construction commitments to follow later in the year.

Public reporting has confirmed several consortia are in contention, including Deutsche Telekom and Brookfield in Germany, Scaleway’s AION consortium in France, a Portuguese public-private bid involving Altice Portugal and NOS, Nokia’s Finnish proposal around the existing Lumi supercomputer, and Romania’s planned multi-site Black Sea AI Gigafactory at Cernavodă and Doiceşti.

Commerical AI gigafactories are already breaking ground

While Brussels finalises its programme, commercial AI gigafactories are already being built on European soil. The most prominent example is Stargate Norway: a 100,000-GPU facility in Narvik backed by OpenAI, Nscale, and Aker, with an initial $1 billion phase, targeting 230 MW of capacity rising to 520 MW. Construction is underway and first GPUs are due online by the end of 2026. The site runs on Norwegian hydropower, uses direct-to-chip liquid cooling, and recycles waste heat to local industry.

Other commercial gigafactory-scale projects are following a similar trajectory. In Portugal, Microsoft and Nscale are expanding the Start Campus site in Sines, starting with 12,600 NVIDIA Blackwell Ultra GPUs from early 2026 and scaling to more than 66,000 Rubin GPUs from late 2027 on a campus permitted for 1.2GW. In Germany, NVIDIA and Deutsche Telekom have announced a 10,000-GPU “industrial AI cloud”, positioned explicitly as a precursor to a future German gigafactory.

This sets an important precedent. Europe’s earliest gigafactory-scale AI facilities are unlikely to be EU-funded, EU-owned or primarily oriented around European frontier-model developers. This shifts the EU’s challenge from building sovereign compute capacity in isolation to shaping the terms on which large-scale AI infrastructure is developed, financed, accessed and governed in Europe.

Where can players capture value?

AI gigafactories sit at the extreme end of the power-led data centre trend already reshaping European infrastructure strategy. These facilities will be anchored by access to bulk low-carbon power, grid capacity, fibre routes, advanced cooling and credible permitting timelines. For telcos and data centre operators, three implications stand out.

1. Gigafactories will be sited where significant power capacity is available: AI gigafactories need 200–500 MW of contracted, low-carbon power and a permitting pathway that can deliver capacity in three to five years. That rules out FLAP-D metros and directs the build-out toward Member States with grid headroom, hydropower or nuclear capacity e.g. the Nordics, Spain and parts of central Europe. Operators with land-banks, substation relationships and grid-adjacent fibre in those geographies will anchor the consortia that win sites.

2. Long-haul interconnect moves from accessory to critical path: Frontier training spans multiple sites, and the resulting models still have to reach end users under EU data-residency rules. That makes deterministic, high-capacity optical links, between gigafactory clusters, hyperscaler regions and edge inference nodes, non-negotiable rather than nice to have. The opportunity for fibre operators is unusually predictable: gigafactory geography points to Nordic-to-FLAP-D and Iberian-to-FLAP-D corridors as the primary new long-haul routes, allowing capacity planning ahead of demand rather than chasing it.

3. Sovereign inference is the most accessible telco play, not the gigafactory itself: A handful of European telcos are in gigafactory consortia (e.g. Deutsche Telekom with Brookfield in Germany, Altice Portugal and NOS in Portugal, Scaleway via the AION consortium in France), but they enter as minority partners alongside industrial, data-centre and energy infrastructure leads.Telcos will likely not own or operate the frontier training layer at scale. The more accessible value sits one tier down, in serving trained models to enterprises and public-sector users under EU data-residency, security, latency and compliance rules. Telcos bring a credible starting point with handistributed infrastructure, enterprise relationships, security credentials, network APIs and edge compute a credible starting hand. However, this is the most contested market in European digital infrastructure: hyperscalers’ sovereign-cloud offerings, GPU clouds (Nscale, CoreWeave), specialist sovereign players (OVH, Scaleway, T-Systems) and Mistral itself are all chasing the same workloads. Telcos that wait for the gigafactory programme to bed in will find the inference customer base already spoken for.

To learn more around how telcos can position around sovereign AI deployment read our latest report: Navigating sovereign AI: Telco strategies, trade-offs and pathways

Conclusion

The EU’s AI gigafactory programme is both a strategic signal and a concrete intervention in Europe’s compute infrastructure market. It will not close the frontier compute gap with the US on its own: €20 billion is substantial by European public-policy standards, but modest compared with the scale of AI infrastructure investment now being deployed by US hyperscalers and frontier model companies. Even so, the programme matters. Frontier-scale AI compute is coming to Europe through a mix of public-backed initiatives and private-sector builds. The EU’s role will be to influence where that capacity is built, who can access it, and how much of the surrounding value chain remains under European control or influence.

Looking for advisory services in data centres? Schedule a call.

Download the data centre insights overview pack

Download the data centre insights overview pack

Get a concise, practical summary of the data centre market: the impact of AI and sovereign strategies, the differentiators that win in a crowded landscape, and proven frameworks for market entry, channel partnerships and customer acquisition—backed by case studies and sample deliverables.

Five things we learned at Datacloud Global Congress 2026

We were at Data Cloud Congress 2026 in Cannes last week to evaluate the key narratives among data centre operators, investors and vendors.

The hidden economics of liquid-cooled data centre retrofits

This article, kindly supported by Airedale, explores when liquid cooling retrofits make commercial sense, showing why the decision depends on HPC pricing, facility fill, market constraints and disciplined execution.

Key takeaways from the launch of the Quantum Infrastructure Council

STL Partners attended the launch of QIC to explore what it will take to deploy

quantum technologies in real-world data-centre environments.

Five things we learned at Datacloud Global Congress 2026

We were at Data Cloud Congress 2026 in Cannes last week to evaluate the key narratives among data centre operators, investors and vendors.

The hidden economics of liquid-cooled data centre retrofits

This article, kindly supported by Airedale, explores when liquid cooling retrofits make commercial sense, showing why the decision depends on HPC pricing, facility fill, market constraints and disciplined execution.

Modular data centres: can prefabricated design speed up construction?

A look at whether modular data-centre design can help operators deliver capacity faster, scale more flexibly and respond to rising demand.