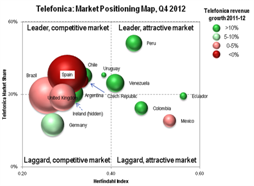

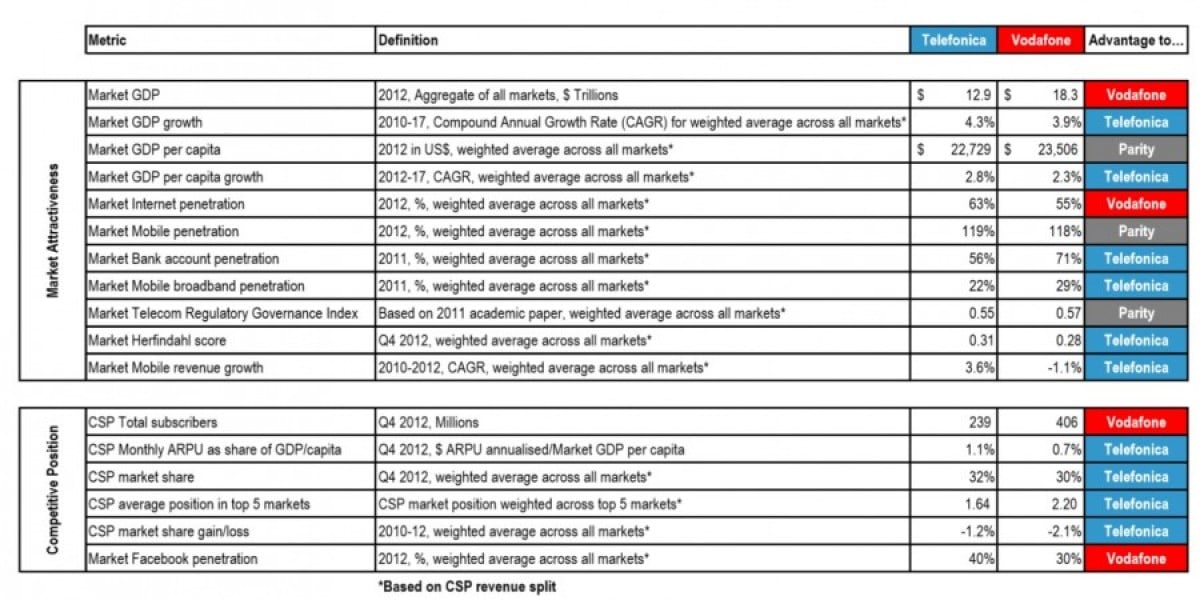

Telefonica leads Vodafone in more attractive markets

In this new report based on Telco 2.0 Transformation Index analysis we compare Vodafone’s competitive positioning with another European-centric multi-national, Telefonica. The results are surprising and instructive, showing that Vodafone faces substantial challenges if it is to grow in the foreseeable future.