Inside the cloud-native telco

Telcos are getting moving with cloud-native. We have asked executives at seven such telcos about the process and what it has meant for their organisations, skills requirements and ways of working.

Telcos are getting moving with cloud-native. We have asked executives at seven such telcos about the process and what it has meant for their organisations, skills requirements and ways of working.

Telcos are investing in edge to grow revenues and monetise their networks. Edge orchestration will be a key tool for these telcos to manage their infrastructure easily and cost-effectively, whilst ensuring that they can meet the strict performance requirements of dynamic edge applications.

With Multi-Access Edge Computing (MEC), telcos can move workloads and applications closer to customers, potentially enhancing experiences and enabling a plethora of new use cases. But with competition looming from other players, telcos need to start commercialising MEC. We have identified and modelled five viable telco business models.

Service providers need to grow new revenues. The cloud market looks potentially attractive, and is growing at about 30% CAGR, but it is dominated in many areas by Amazon, Google and Microsoft. So is Cloud part of the answer for telcos, and if so how? This report looks at the role of the service provider in the cloud market and products that service providers might offer in 2015.

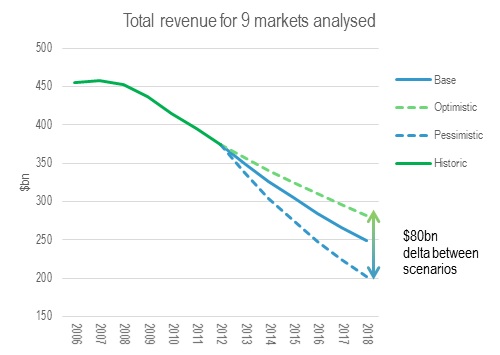

Telco 2.0 presents a new strategy report examining the evolution of cloud services; the current opportunities for vendors and Telcos in the Cloud market, plus a penetrating analysis on the positioning Telcos need to adapt in order to take advantage of the potential $200Bn global Cloud services market. This report offers over 140 pages of insightful commentary from those who’ve been working at the cutting edge, and includes an introduction to the sector’s key technologies and emerging trends, as well as detailed recommendations for Telcos and vendors. (December 2012, Strategy Report, Cloud and Enterprise ICT Stream.)

Cloud Strategy Report Image

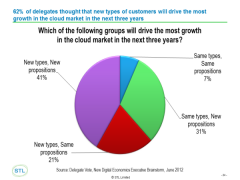

The fight for the Cloud Services market is about to move into new segments and territories. In the build up to the launch of our new strategy report, ‘Telco strategies in the Cloud’, we review perspectives on this shared at the 2012 EMEA and Silicon Valley Executive Brainstorms by strategists from major telcos and tech players, including: Orange, Telefonica, Verizon, Vodafone, Amazon, Bain, Cisco, and Ericsson (September 2012, Executive Briefing Service, Cloud & Enterprise ICT Stream).

Cloud Growth Groups September 2012

Enterprise cloud computing services need great connectivity to work, but there are opportunities for telcos to participate beyond the connectivity. What are the opportunities, how are telcos approaching them, and what are the key strategies? Includes forecasts for telcos’ shares of VPC, IaaS, PaaS and SaaS. (September 2011, Executive Briefing Service, Cloud & Enterprise ICT Stream)

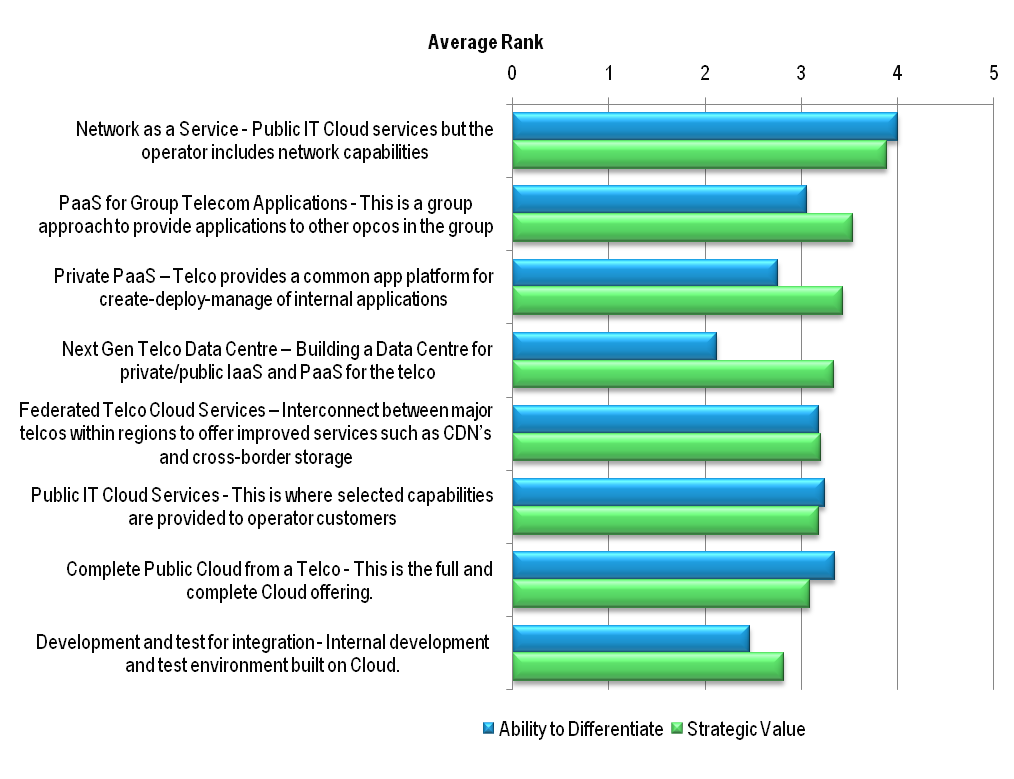

Apps & Telco APIs Figure 1 Drivers of the App Market Telco 2.0 Sept 2011

Telcos should grow Cloud Services revenues nine-fold and triple their overall market share in the next three years according to delegates at the May 2011 EMEA Executive Brainstorm. But which are the best opportunities and strategies? (June 2011, Executive Briefing Service, Cloud & Enterprise ICT Stream)

Cloud Forecast 2014

Telco 2.0’s analysis of operators’ potential role and opportunity in ‘Cloud Services’, a set of new business model opportunities that are still in an early stage of development – although players such as Amazon have already blazed a substantial trail. (December 2010, , Executive Briefing Service, Cloud & Enterprise ICT Stream & Foundation 2.0)

The early stage of development of the market means there is some confusion on the telco Cloud opportunity, yet clarity is starting to emerge, and the concept of ‘Network-as-a-Service’ found particular favour with Telco 2.0 delegates at our recent Brainstorms. (December 2010, Executive Briefing Service, Cloud & Enterprise ICT Stream)

IBM say that telcos are well positioned to provide cloud services, and forecast an $89Bn opportunity over 5 years globally. Video presentation and slides including forecast, case studies, and lessons for future competitiveness. (December 2010, Executive Briefing Service, Cloud & Enterprise ICT Stream).