New MVNOs: Challenger brands and lessons from the UK market

Disruptors from other industries are turning their attention to the mobile market. They can learn from the vibrant UK MVNO market.

Disruptors from other industries are turning their attention to the mobile market. They can learn from the vibrant UK MVNO market.

Industry-leading telcos have captured much of the lower hanging fruit in their progress to net-zero and must now find the incremental gains. This requires integrating sustainability as a priority across all parts of the organisation. What actions and associated KPIs must individual business units within a telco take on to prioritise sustainability day-to-day?

As analytics, AI and automation (A3) technologies mature, we explore nine potential A3 capabilities telcos could offer to their enterprise customers. We identify the sweet spots for telcos by assessing the importance of each of the nine capabilities across 14 industry verticals and mapping them against telcos’ existing levels of expertise.

It has been six years since telcos began introducing data and analytics products into their portfolio of enterprise services. This report assesses the potential value of data monetisation across 13 verticals, and by type of data analytics product.

We outline three potential roles for telcos in the IoT, describing twelve potential application areas and forty use cases, as well as the structure and trends driving change. Looking beyond this we ask which market areas are most attractive, and what should telcos do within them?

The early high hopes for SDN and NFV have given way to the realization that the road to cloud-telco ‘heaven’ is strewn with ‘infernal’ rocks and pitfalls. We present the “devil’s advocate’s” (i.e. an extremely sceptical) view of NFV set out in eight indictments. We then examine the argument for the defence.

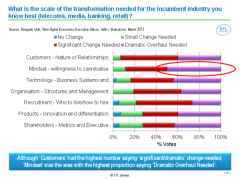

Value is squeezed out of industries as they become increasingly digital – i.e. accessed by mobile and online, driven by data and defined by software. We call the collective economic impact of this pressure ‘The Great Compression’. But which companies will survive and prosper – and how? 90% of the Execs at our Silicon Valley brainstorm identified ‘management mindset’ as a key factor in Telecoms, Media, Finance and Retail. Our analysis and a detailed report of the findings of the Digital Economy session at the NDE Executive Brainstorm, Silicon Valley, held at the InterContinental Hotel, San Francisco on the 19th March 2013. (May 2013, Executive Briefing Service, Transformation Stream).

Scale of Transformation Needed April 2013

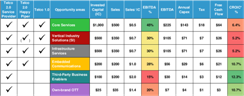

Structuring finances is key for the success of innovations in general and Telco 2.0 projects in particular. In this detailed extract from our new strategy report ‘A Practical Guide to Implementing Telco 2.0’, we describe the best ways to approach the management of revenues and costs of new business models, and how to get the CFO and finance department onside with the new approaches required (February 2013, Executive Briefing Service, Transformation Stream).

Small table on finances

First of a series on the ‘credit crunch’: how the liquidity crisis in the financial markets may provide telcos with opportunities for enhancement and transformation of business models. (October 2008)