Cloud 2.0: the fight for the next wave of customers

The fight for the Cloud Services market is about to move into new segments and territories. In the build up to the launch of our new strategy report, ‘Telco strategies in the Cloud’, we review perspectives on this shared at the 2012 EMEA and Silicon Valley Executive Brainstorms by strategists from major telcos and tech players, including: Orange, Telefonica, Verizon, Vodafone, Amazon, Bain, Cisco, and Ericsson (September 2012, Executive Briefing Service, Cloud & Enterprise ICT Stream).

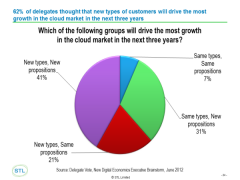

Cloud Growth Groups September 2012