We know from looking at examples like TELUS, Telstra, Orange, KPN, Telia, etc. that building a new business in the healthcare vertical is not a quick win for telcos.

It requires significant time and effort to understand where, as a telco, you can bring the best value in your local healthcare market. You have to build these services and capabilities through internal development, acquisitions, and trial and error with customers. Only through this experience can telcos really build up a deep understanding of healthcare organisations’, doctors’, clinicians’ and patients’ pain points. Once you are confident that you understand what customers need, you still need to recruit and train a sales team that can clearly articulate how your solutions solve those problems.

Taking a “wait and see” approach to developing a digital health business, perhaps launching a couple of trials or PoCs and seeing if they deliver value, or investing in a digital health start-up or two, may have been a viable approach before the COVID pandemic hit, but this is no longer the case.

Cost of delivering core healthcare services in the UK across key metrics, comparing the pre-COVID base case vs. post-COVID reality*

*key metrics include ER visits, GP appointments, outpatient appointments, etc.. Source: NHS statisctics, STL Partners analysis

The graph above compares a pre-COVID base case uptake of digital health and the resulting cost savings for the UK healthcare sector against the accelerated uptake in a post-COVID world, which clearly shows significant impact in 2020/2021 as healthcare systems and patients implement social distancing measures. Following the immediate COVID impact, we expect this market to reap the rewards of a step change during COVID and begin to mature rapidly from 2022-2023. Alongside the exponential increase in usage of digital health applications in 2020 – spurred in many countries by changing regulations around usage and reimbursement for digital health services – private investment into digital health companies also skyrocketed last year. Competition is heating up.

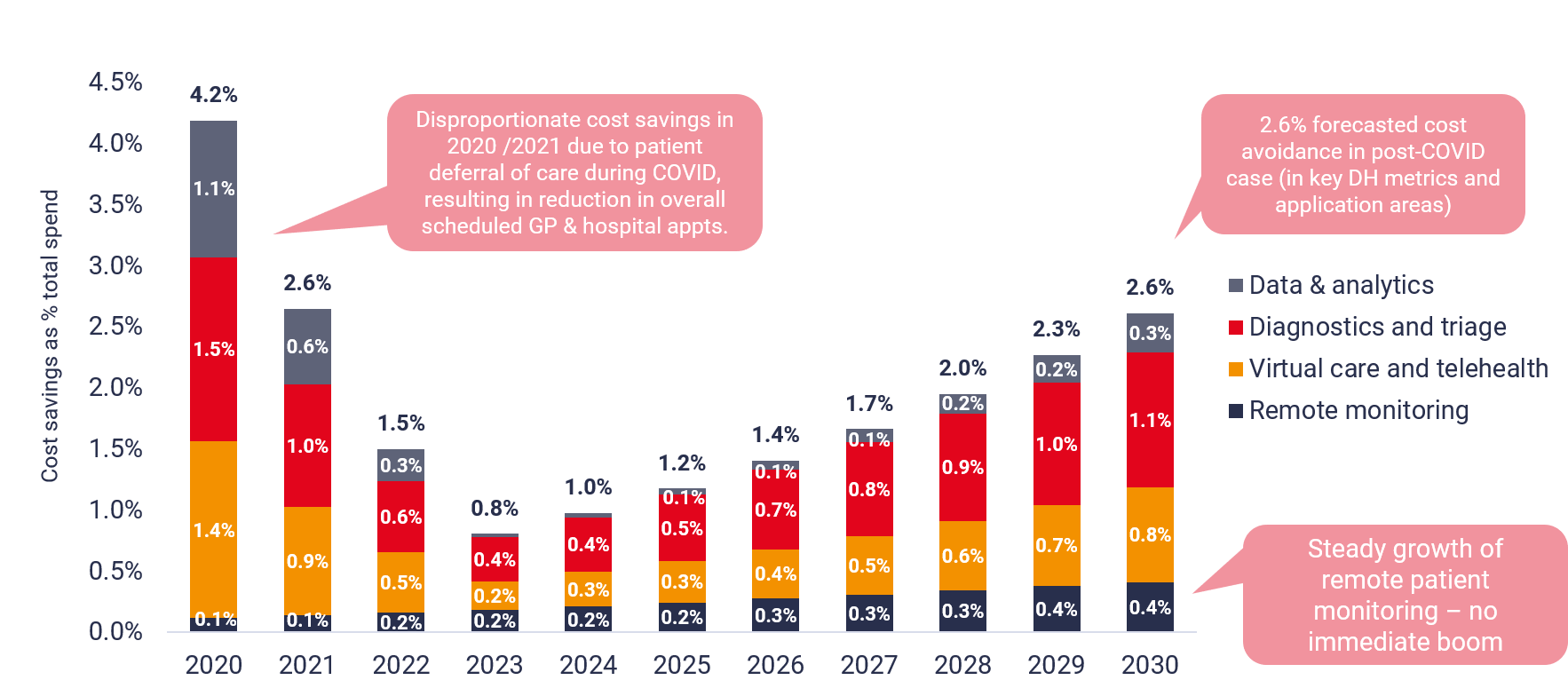

Cost savings by application area, as a percentage of total healthcare spend (UK)

Source: NHS statistics, STL Partners analysis

We are still convinced this is a good market for operators to bring value to: healthcare is an everlasting need, it operates within national economies of scale (even if the technology is global, implementation of that tech requires local knowledge and relationships), it is a big sector that can truly move the needle on revenues, and improving healthcare outcomes is meaningful work that all employees and customers can relate to. But the window is closing. It will still take an operator several years to develop a strong digital health proposition, that is credible with healthcare professionals, and drives revenue growth. So if telcos do want to capture a share of our forecasted 2.6% total cost savings for the healthcare market, the time to commit is now. (Note: UK data is indicative of global forecasts included in forthcoming research.)