Digital Health Market Trends: Modelling Post-COVID Impact

Exploring COVID’s impact on the digital health market and digital health trends

Introduction

For the last five years STL Partners has researched the opportunity for telecoms operators in healthcare. We have produced in-depth case studies on leading operators such as TELUS in Canada and Telstra in Australia, and conducted rigorous analysis of the market landscape and key digital health trends, to understand where operators can play across the value chain and in specific application areas.

Our conversations with many other operators globally show that most telcos with an interest in healthcare are sitting hesitantly on the side-lines. They can see the opportunities but are uncertain of the scale and their own ability to grasp them.

STL Partners believes that with the right level of commitment, telcos can leverage their reach and capabilities to help solve the challenges in healthcare in their markets. But the window of opportunity is closing fast.

This new sizing model for digital healthcare reflects the recent impact of the COVID pandemic on the sector, with the goal of identifying the key trends in digital health and the new opportunities presented to operators and others attempting or considering investment in the market.

The COVID digital health dividend

The first digital health trend from our analysis is that a four-year acceleration in adoption of digital health solutions during the pandemic will deliver a hidden dividend of $300bn globally by 2030. In the chart below you can compare forecasted global costs across our four modelled scenarios.

- No COVID: Total costs of delivering healthcare services, assuming COVID had no impact on adoption of digital health services. The “No COVID” case therefore predicts increased adoption of digital health services out to 2030 as if COVID had not happened.

- Flat digital health: Total costs with no change in adoption rate of digital health from 2019. This flat lines growth in adoption of digital health services, assuming adoption is the same in 2030 as it was in 2019. This is used primarily as a control variable.

- With COVID (real world): Total costs with accelerated adoption of digital health in 2020 due to COVID, including deferred use of healthcare services to maintain social distancing or reduce burden on healthcare providers. Because many of the cost savings from digital health solutions stem from fewer primary and urgent care consultations, real world data showing lower usage of these healthcare services resulted in lower costs of healthcare delivery across the 12 use cases between 2020 and 2022, when we expect “normal” healthcare services to resume.

- With COVID (digital health impact only): Total costs with accelerated adoption of digital health in 2020 due to COVID, excluding the COVID-related dip in use of healthcare services (see With COVID (real world)) to isolate the impact of higher adoption of digital health solutions.

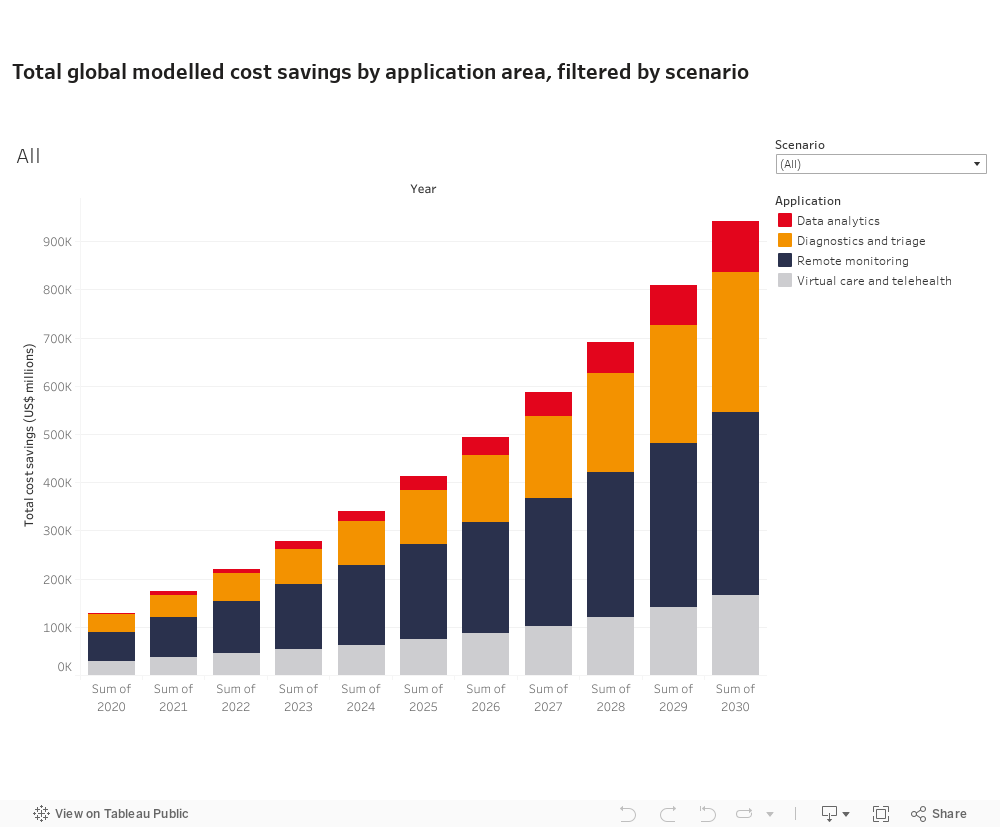

Breaking down cost savings by digital health application

Our digital health market model also breaks down the value across four digital health application areas, focusing on areas that we believe are of greatest strategic importance to telecoms operators. The objective of this analysis is to identify the trends across digital health use cases and identify growth trajectories for different applications

- Remote monitoring: Use of smartphone applications and IoT sensors to track patient vital signs, habits and other healthcare information/equipment

- Virtual care & telehealth: Use of digital tools such as video consultations and smartphone apps to overcome time and geographical barriers to delivering healthcare services in primary and secondary care

- Diagnostics & triage: Use of smartphone applications and AI-enabled tools to assess patient needs and diagnose health conditions more efficiently and accurately

- Population data & analytics: Use of big data analytics and AI with large national, regional, or cross-provider healthcare data sets to identify at risk patient groups, develop personalised medicine and inform healthcare policy

The chart below illustrates the difference between the With COVID (digital health impact only) scenario with the No COVID and Flat digital health scenarios to illustrate the COVID-triggered cost savings, broken down by application area. While virtual care has probably been the most discussed digital health solution during the pandemic, as healthcare providers and patients all sought to avoid in-person contact, it is not necessarily a big cost saver for all healthcare markets. Virtual consultations don’t eliminate the biggest cost in healthcare delivery – doctors’ time – although in countries with limited access it will drastically improve access to healthcare.

The full version of our model breaks down these application areas into 12 specific use cases, and includes data for 217 countries globally. Get in touch to dig into the data in more detail.

Want to learn more about our modelling of the digital health market trends?

The $300bn COVID digital health dividend report

This detailed analytical model of 217 digital healthcare markets shows that the COVID pandemic has accelerated the global market four years ahead of its prior trajectory. Key questions we address in this analysis are:

- How much has COVID accelerated adoption of digital health applications?

- What is the value of accelerated uptake of digital health following COVID?

- Which digital health application areas have been most affected by COVID?

- Beyond the COVID impact, what is the total potential value of digital health applications for

healthcare providers? - Which digital health application areas will deliver the biggest cost savings, globally and within

specific markets?

Enter your details below and we’ll send you a free extract of the report.

Read more about digital health

Webinar

Telcos in health webinar

In this session Amy Cameron and Yesmean Luk looked at the opportunities for telcos in health. As a growing industry, with a national focus and significant digitisation challenges, healthcare is an attractive vertical for telcos seeking to build new revenues beyond core communications services.

Research

TELUS Health: Innovation leader case study

Healthcare is an attractive vertical for telcos to address with digital solutions. Although many telcos have made attempts to capture this opportunity, TELUS stands out as an example of the value of a long-term commitment to healthcare. In this case study, we examine TELUS’ strategy in health, evidence of its success, and draw out lessons for other telcos