Four strategies for telcos in healthcare

A rocky start for telcos in health

Historically, telcos have found it hard to succeed in the healthcare vertical. We believe this is because they underestimated the complexity of healthcare delivery and patient data, and the slow pace of change in working practices within the sector.

Many telcos initially approached healthcare from the consumer angle, believing that their reach into the consumer market coupled with connectivity made them good candidates to deliver telehealth (video consultations with doctors) or personal health services directly to consumers. However, most telcos abandoned their ventures after initial failure to identify the right payer, and slow take-up of telehealth as doctors, patients and governments are still not convinced that video consultations can replace face to face ones.

On the data complexity side, a couple of examples are BT’s contract to digitise around 50mn patient records in the UK, and Telstra’s contract to develop national cancer registries in Australia. In both cases, the operators underestimated how much patient records varied between GPs, hospitals, and even within departments. This fragmentation means that digitising healthcare data in a way that makes it easy to share across multiple different stakeholders in the sector is a mammoth task, which requires a strong understanding of how the healthcare sector works, and also of how doctors, clinicians, patients and governments want to use it to improve healthcare outcomes in future. While BT has stepped back from the digital health market since then, Telstra has successfully overcome these challenges and is now scaling up its government health solutions.

Although most developed countries’ healthcare providers have made significant progress in digitising patient records and setting up systems to share basic information, a lot of valuable data remains difficult to share securely, interpret and use to develop new services to improve the efficiency and quality of healthcare outcomes.

However, thanks to the increasing sophistication of consumer health propositions from Fitbit, Garmin, Apple, etc., consumers have become far more aware and demanding of digital health solutions.

We believe the combination of improving health IT systems, more demanding patients, the growing maturity of analytics and AI, and rising cost pressures on healthcare systems together are creating a tipping point for growth in digital health.

So what’s the opportunity for telcos?

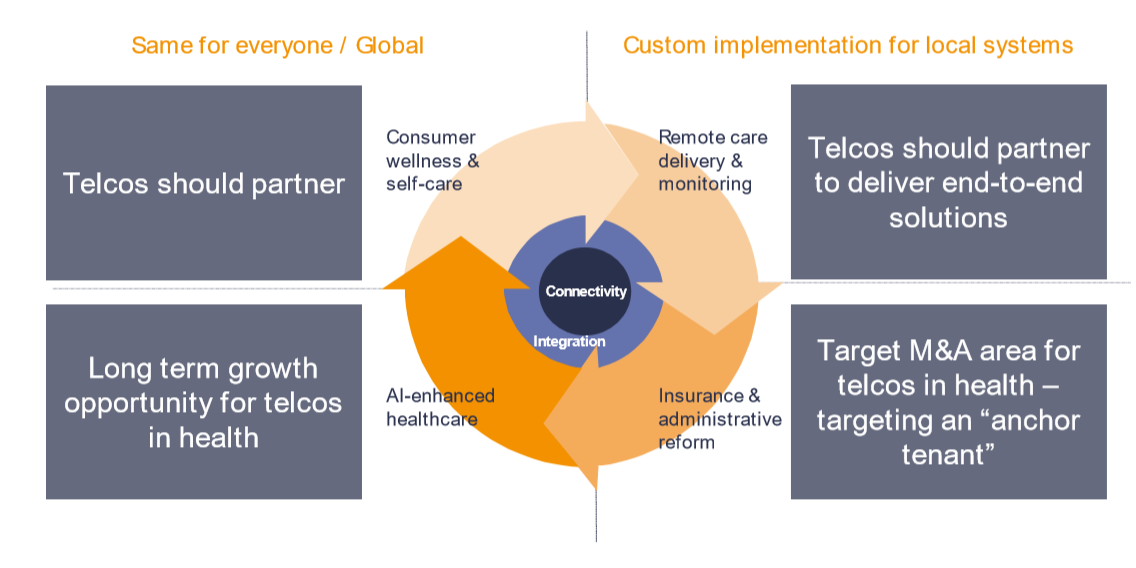

Based on our in-depth research of more than ten telcos’ development of digital health businesses, including TELUS, Telstra, Swisscom and KPN, we believe operators should take different strategies in different parts of the digital health market.

- Consumer wellness and self-care: This part of the market includes consumer facing applications and devices to help improve fitness, monitor health KPIs and conditions, etc. This is a highly competitive, global market where leading players are already well established, and we are even beginning to see consolidation, e.g. through Google’s acquisition of Fitbit. It is not well suited to telcos’ strengths, although telcos with a presence in their local healthcare markets may be attractive partners for global consumer wellness players seeking to link into the formal healthcare market.

- Remote care delivery & monitoring: Many of the devices and applications used in this segment are similar to the consumer wellness market – but the difference is they are provided by, paid for, and prescribed by healthcare providers (doctors, nurses, clinicians, etc.). These include services to manage chronic conditions, as well as to improve access to health services, such as online appointment bookings, prescription management, video consultations and personal health records. Developing services that fit into healthcare providers’ workflow, are easy for patients to use, and adaptable to different users’ needs takes significant time and effort, but healthcare providers lack the resources to pull all the pieces together themselves. For this reason, we believe that in most cases telcos should partner to deliver end-to-end services in this category. Depending on a telco’s strategy, they may also develop or acquire a small number of solutions in this area.

- Insurance and administrative reform: This is the biggest segment of the digital health market today, covering all the IT systems that help hospitals, GPs, labs, insurance companies etc. manage patient records and day to day activities. These systems are crucial for enabling improved data sharing across the industry and development of more sophisticated remote care and delivery solutions. In the hospital market, there are some large global players, but in most cases healthcare providers’ needs are dependent on the structure of the local market so most software providers tend to be locally based. This has been the main entry point for telcos seeking to build their presence in the healthcare market, and an important area to have a foothold in to play a coordination role.

- AI-enhanced healthcare delivery: As the digital health solutions across the first three categories become more sophisticated, it will become possible to apply advanced analytics to improve nearly all aspects of healthcare delivery. In many cases, AI models will work well across multiple geographies – for instance Google’s AI breast cancer screening tool delivered similar results in the US and the UK (in both countries it was more accurate than human radiologists). As in any application of analytics, access to data is the fundamental requirement, so this opportunity will be more accessible to telcos that are managing data through other solutions (this doesn’t necessarily have to be patient records, it could be operational information about how healthcare services are used or delivered).

Note that this view of the digital health market is built around the potential opportunities for telcos, so it excludes areas that are less relevant for them, such as drug discovery and development.

Digital health insights pack

This 24-page document will provide you with a summary of insights from our healthcare research and consulting work:

- Key trends in the healthcare industry

- The role for telecoms: applications and business models

- Strategies for success: where to start

- How STL Partners can support you

Request the free digital health insights pack by clicking on button below:

![]()

Read more about Virtualisation, SD-WAN & NFV

Webinar

Telcos in health webinar

In this session Amy Cameron and Yesmean Luk looked at the opportunities for telcos in health. As a growing industry, with a national focus and significant digitisation challenges, healthcare is an attractive vertical for telcos seeking to build new revenues beyond core communications services.

Research

TELUS Health: Innovation leader case study

Healthcare is an attractive vertical for telcos to address with digital solutions. Although many telcos have made attempts to capture this opportunity, TELUS stands out as an example of the value of a long-term commitment to healthcare. In this case study, we examine TELUS’ strategy in health, evidence of its success, and draw out lessons for other telcos