Download

This article explores the emerging possibility of an AI bubble, drawing comparisons between the contemporary AI landscape and the dot-com bubble of the early 2000s. We aim to guide enterprises on how to leverage AI’s potential while remaining wary of the surrounding hype.

Murmurings of a potential AI bubble came to a head when OpenAI CEO Sam Altman suggested so himself. In a report published by The Verge on 15th August 2025, Altman was quoted as suggesting that “investors as a whole are overexcited about AI” accompanied by the important caveat that, nonetheless, “AI is the most important thing to happen in a very long time.” Unsurprisingly, this led to a flurry of press scrutinising the possibility of an ‘AI hype bubble’ along with comparisons to the dot-com bubble of the early 2000s. But what does an ‘AI bubble’ mean? Where’s the evidence? And if we’re in one, what should we do about it?

Are we in an AI bubble?

An economic bubble is defined as a rapid escalation in asset prices, often due to speculative behaviour, followed by a sharp contraction. In the context of AI, this translates as a period where investment, valuations and public expectations for AI’s near-term economic impact outrun what the technology can plausibly deliver at scale. This would imply, in Altman’s words that “investors are likely to lose a lot of money.” Discrepancy between AI’s ‘near-term economic impact’ and what the technology ‘can plausibly deliver at scale’ can be distilled into two simpler questions: is there a fundamental mismatch between AI expectation and reality, and if so, is it comparable to the dot-com bubble? Evidently, there are many ways to assess the expected economic impact of AI. In this article, we’ll look specifically at two metrics: capital markets activity and investment into infrastructure.

Speculative fervour

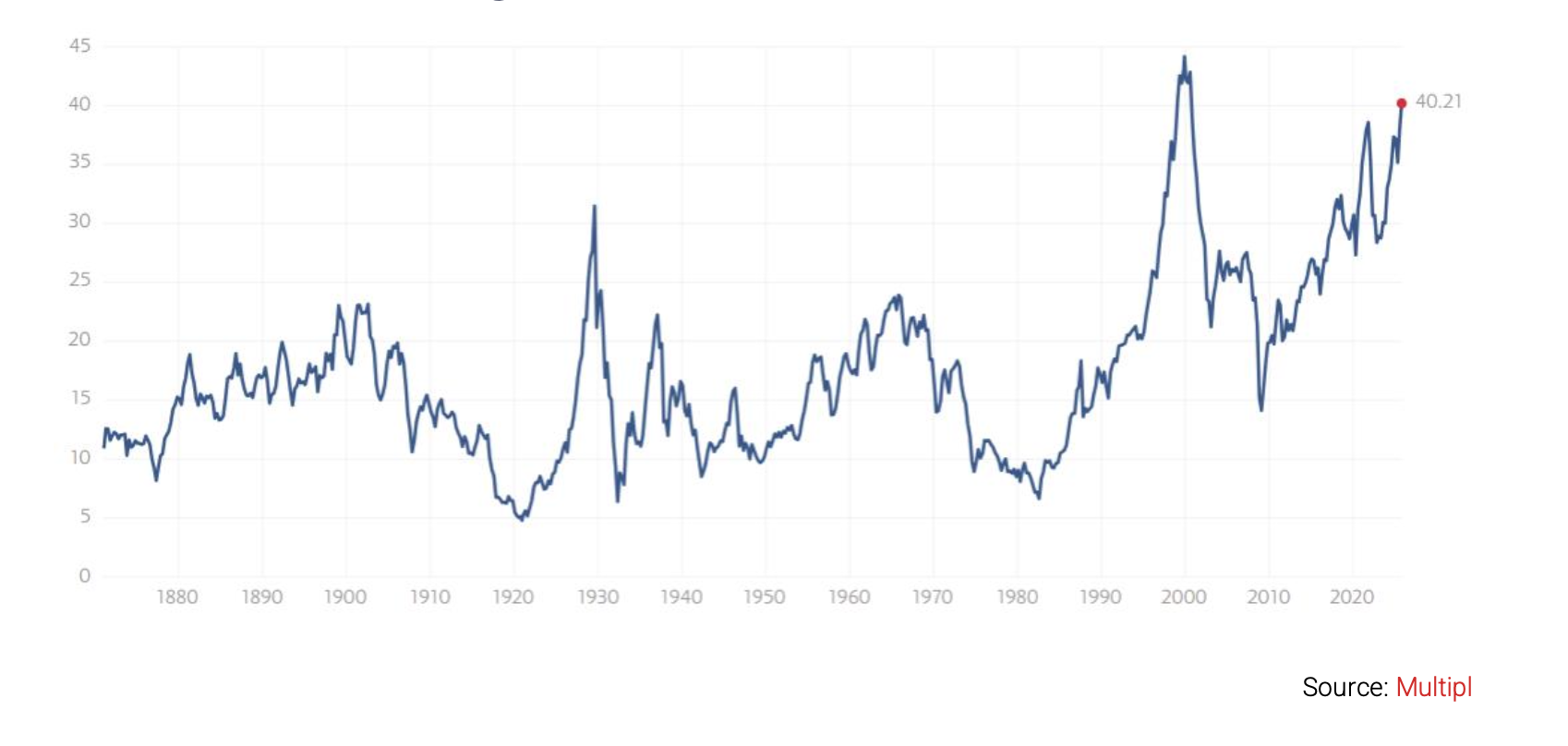

During the dot-com bubble, ‘speculative mania’ drove US technology stock valuations sky-high, epitomised by the Nasdaq composite rising nearly 400% between 1995 and March 2000, only to crash 78% by October 2002. Crucially, this speculation relied on the promise of revenue rather than actual earnings. This price inflation served as a key indicator of the formation of a bubble. Today, however, another indicator that draws parallels to the dot-com bubble is the trajectory of the S&P 500’s Shiller PE ratio, which is nearing the levels reached in the early 2000’s. The Shiller P/E ratio is the ratio of stock price to average inflation-adjusted earnings from the previous 10 years. The Shiller PE ratio helps to avoid the distortion cause by short-term events giving a longer-term view of the market. Historically, the higher the Shiller PE, the more optimism is baked into prices and the lower you should expect the next ten years of returns to be on average.

Figure 1: Shiller PE Ratio of S&P 500

Infrastructure investment

In the dot-com era, telecoms poured billions (>USD500bn) into fibre leaving a glut of largely unused capacity when demand disappointed. Today, investment into data centres equipped to handle AI processing loads echoes and amplifies this investor enthusiasm. Spending on AI-related infrastructure is estimated to exceed USD7tn in the next 10 years with Google, Amazon, Microsoft and Meta anticipating spending more than USD400bn on data centres in 2026. Current demand for AI is undeniable, with 700mn people a week using OpenAI’s ChatGPT, but the question is whether demand and spend will continue to grow at the rate required to justify investments in this infrastructure. Furthermore, modern AI infrastructure is costly from a variety of angles. GPUs (Graphics Processing Units), although a cornerstone of AI processing, are also a quickly depreciating asset. Massed Compute estimates value loss of 20 to 30 per cent a year, with an average lifespan of 3–5 years. In stark contrast, fibre cables last 20–30 years. Ultimately, as observed in the FT, the investment case for an AI data centre hinges on the rental market growing fast enough to cover sunk costs before the hardware is obsolete.

The economic impact of GenAI

It’s difficult to accurately predict what economic impact AI will have in the future. Nonetheless, we can look at AI’s impact today vs the historical precedent of the Internet.

Lack of enterprise ROI

A recent report released by MIT suggests that 95% of organisations are seeing no ROI from AI implementation. This statistic, although significant, is not necessarily surprising when considering the limitations of current AI systems. For example, Large Language Models’ (LLMs) propensity for hallucination can impact the accuracy of information, which can lead to bias and errors. Equally, current GenAI models can struggle with understanding nuance or context, resulting in errors in decision-making that require human intervention. However, enterprise challenges regarding implementation are not exclusively the fault of AI limitations and may also stem from an existing lack of digitisation and technical debt or, equally, a skills gap in AI expertise, as suggested by an IBM survey from 2024.

Although by some indications GenAI is currently generating minimal ROI for enterprises, this is unlikely to remain the case in the long term. New AI systems and approaches, such as Small Language Models (SLMs), and domain-specific models will overcome many of the limitations of current AI systems. However, it will require coordination and hard work to resolve the questions around policy and governance as the path to extracting value from AI evolves. When exactly the value of AI will become tangible and whether we can answer these questions quickly enough remains uncertain.

Figure 2 estimates that the combined capital expenditure (capex) of Alphabet, Amazon, Microsoft, and Meta will rise from roughly USD210 billion in 2024 to USD520 billion by 2030, a CAGR of around 16%. For revenues to keep pace with this increase in investment, the collective revenues of these four firms would need to grow from approximately USD1.4 trillion in 2024 to nearly USD3 trillion by 2030.

This isn’t inconceivable; between 2019 and 2024, their combined revenues rose from USD650 billion to USD1.4 trillion, a CAGR of 14%, close to the rate required to match future capex growth. However, the macroeconomic environment over 2019–2024 was unusually favourable: pandemic-driven digitisation, elevated demand for digital services, and inflation all boosted revenues.

The key question, therefore, is whether AI will cause similar revenue growth between 2024 and 2030.

Comparing AI trends with the emergence of the internet

The internet has, without question, revolutionised the world. The Magnificent 7 (Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia and Tesla), incidentally also those that are betting on AI’s success, would not exist without it. Nonetheless, the changes this technology promised took longer than expected to materialise. ITU estimates that approximately 5.5 billion people – or 68% of the world’s population – regularly use the Internet in 2024. This represents an increase from only 53% in 2019, with 1.3 billion people estimated to have come online during that period. However, this leaves 2.6 billion people still offline. Unsurprisingly, this timeline may be indicative for AI. Businesses must therefore still seek to embed good practice and identify genuine business cases while remaining wary of the AI wave. An article from the Harvard Business Review written in 2001 encapsulates contemporary attitudes towards the internet. Here, ‘the Internet’ might well be considered synonymous with ‘AI’, doubly reflecting attitudes from then (and now):

Looking backwards, moving forwards

The dot-com era offers valuable lessons for enterprises looking to navigate this technological step change. Despite the collapse of numerous enterprises in the early 2000s, including Pets.com and Webvan, players like eBay and Amazon successfully weathered the storm. Although they endured huge drawdowns, these companies bounced back due to real customer adoption. Companies that went into administration fell foul of the “build it and they will come” mindset, investing heavily in advertising without having viable business models to fall back on. These examples demonstrate that enterprise responsibility for addressing customer needs must become more important, rather than less so. Enterprises can begin addressing this challenge by answering a fundamental question around the role of AI in their business: what problem does this solve for my business, my customers, my people? If history is to repeat itself, the companies that succeed will be those whose leaders combine vision with discipline, using AI where it creates a measurable advantage. In parallel, companies should exploit the technological advances enabled by AI while remaining agile and flexible as this technology evolves. Ultimately, those that will come out on top will rationally stick to the fundamentals while extracting value from this emerging technology.

Looking for advisory services in AI? Schedule a call.

Download the AI insights pack

Download the data centre insights overview pack

Our overview explores the evolving role of telcos in the AI ecosystem—examining how they act as consumers of AI, as enablers of AI adoption across industries, and as providers of AI-driven solutions to others.

The Rise of AI-as-a-Service: Top 3 Enterprise Use Cases by Telcos

As enterprise deployments now account for nearly 40% of telco GenAI initiatives, the shift toward AI-as-a-service is accelerating

Building networks of trust: How creating a human–AI partnership can help redefine network operations

How a new, cross-domain AI approach leveraging the latest AI techniques can help elevate employee roles and responsibilities in network operations teams.

From GenAI Experiments to Experiences: Top3 Consumer Use Cases by Telcos

Telcos are starting to turn generative AI from pilot projects into real consumer products.

How AI can accelerate IT and OT convergence to transform customer experience

AI can play a central role in enabling convergence, acting as a unifying intelligence layer across IT and OT.

The Rise of AI-as-a-Service: Top 3 Enterprise Use Cases by Telcos

As enterprise deployments now account for nearly 40% of telco GenAI initiatives, the shift toward AI-as-a-service is accelerating

Lessons from the dot-com bubble for the AI era

We explore the emerging possibility of an AI bubble, drawing comparisons between the contemporary AI landscape and the dot-com bubble.