Telecom traffic: Heading for the fast lane?

Will artificial intelligence, immersive services, automated transportation and robotics drive a substantial increase in telecom traffic between now and 2032?

Will artificial intelligence, immersive services, automated transportation and robotics drive a substantial increase in telecom traffic between now and 2032?

How telcos can help consumers live more sustainably without compromising their business objectives.

Fixed operators see network disaggregation as a way to reduce deployment and operational costs, remove vendor lock-in, and combine residential, business and other types of access into a single infrastructure. This report examines progress and learnings from early movers.

Most consumers do not need FTTH speeds and capacity, but there are other reasons why households may pay a premium for full fibre connectivity.

Recently, Orange passed 22 million homes, Telefónica 20 million, and AT&T is now reaching five million more every year. The Chinese have over 300 million FTTH connections. What does FTTH do for ARPU, churn, OPEX and 5G that makes it so compelling?

BT’s attempt to acquire EE in the UK presents the regulator and its competitors with choices that could re-frame the principles of regulation and competition in an era of consolidation, with consequences for many other markets. Will BT succeed, and if so, what will be the terms of the deal, and how will the market subsequently play out?

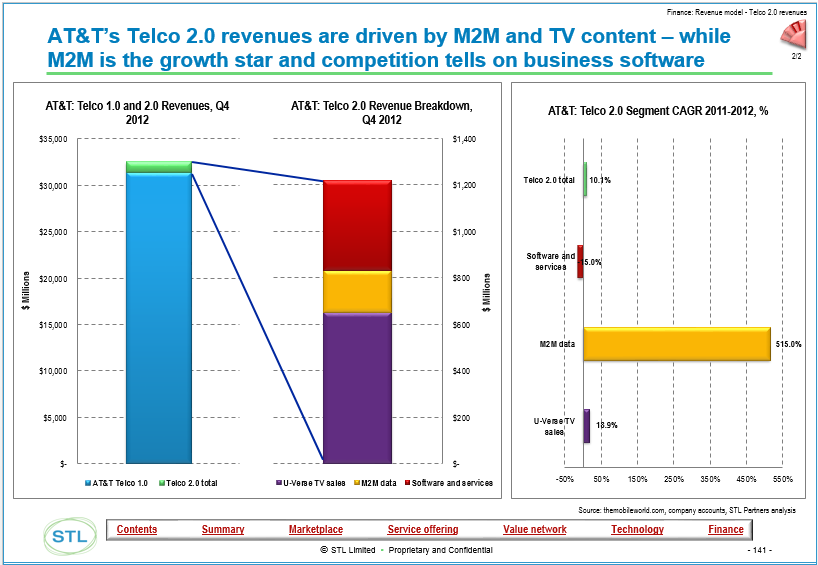

AT&T’s residential fixed operation is underperforming as faster cable connections take over. It would probably like to trim its footprint or get out, and invest in fibre and its content business model. Is that really an option, and what are the lessons for other telcos?

Verizon and Comcast have invested in high bandwidth fibre and cable networks, whereas AT&T has until recently focused on U-Verse, an IPTV play. Which strategy is winning out and why? The answer is surprising and may transform the US and other markets, and there are parallels with Apple and Samsung’s ‘deep value’ strategies of investing in assets that are hard to replicate.