Download

Listen

Neoclouds are rising fast, offering GPU-first infrastructure built for AI workloads with lower costs and faster deployment than traditional clouds. But are they truly in competition with hyperscalers like AWS, Azure, and Google Cloud — or playing a fundamentally different role? This article weighs the pros and cons of neoclouds and explores their place in an increasingly multi-cloud, AI-driven world.

In our recent article “Neoclouds: The new cloud players vying for the AI crown”, we explored the emergence of neoclouds – GPU-centric cloud providers purpose-built for the demands of AI. Their rise is closely tied to a surge in demand for high-performance compute, growing interest in sovereign infrastructure, and increasing dissatisfaction with the economics and limitations of traditional hyperscale cloud platforms (HCPs) like AWS, Microsoft Azure, and Google Cloud.

While neoclouds offer lower costs and specialised performance, they haven’t yet disrupted the dominant position of the hyperscalers in the cloud computing market. Despite surging demand for AI infrastructure, the major cloud platforms have faced little sustained pricing pressure — in part because many enterprises are still willing to pay a premium for the convenience, integration, and perceived reliability of a single-cloud ecosystem.

In this article, we examine the pros and cons of neoclouds, compare them to traditional hyperscalers, and explore where each model fits into the evolving edge and cloud landscape.

A tale of two cloud models

At their core, neoclouds and hyperscalers offer similar services — compute resources delivered on-demand, paid for by usage. But their business models and design philosophies diverge significantly.

Neoclouds are specialised providers focused almost entirely on GPU-as-a-Service. Their infrastructure is built around dense racks of high-end GPUs (often NVIDIA H100s or A100s), high-speed interconnects, and advanced cooling systems, often deployed in newly built (greenfield) data centres. Their primary customers are AI model developers, AI application providers, startups, researchers, and increasingly, larger enterprises and hyperscalers themselves (e.g. Microsoft signed a deal to rent AI compute from Nscale).

Hyperscalers, meanwhile, offer a full stack of services — from CPU-only virtual machines and storage to managed databases, analytics, developer tools, and AI platforms. Their global presence, enterprise trust, and deep capital reserves make them the default cloud partner for many large organisations.

The case for neoclouds

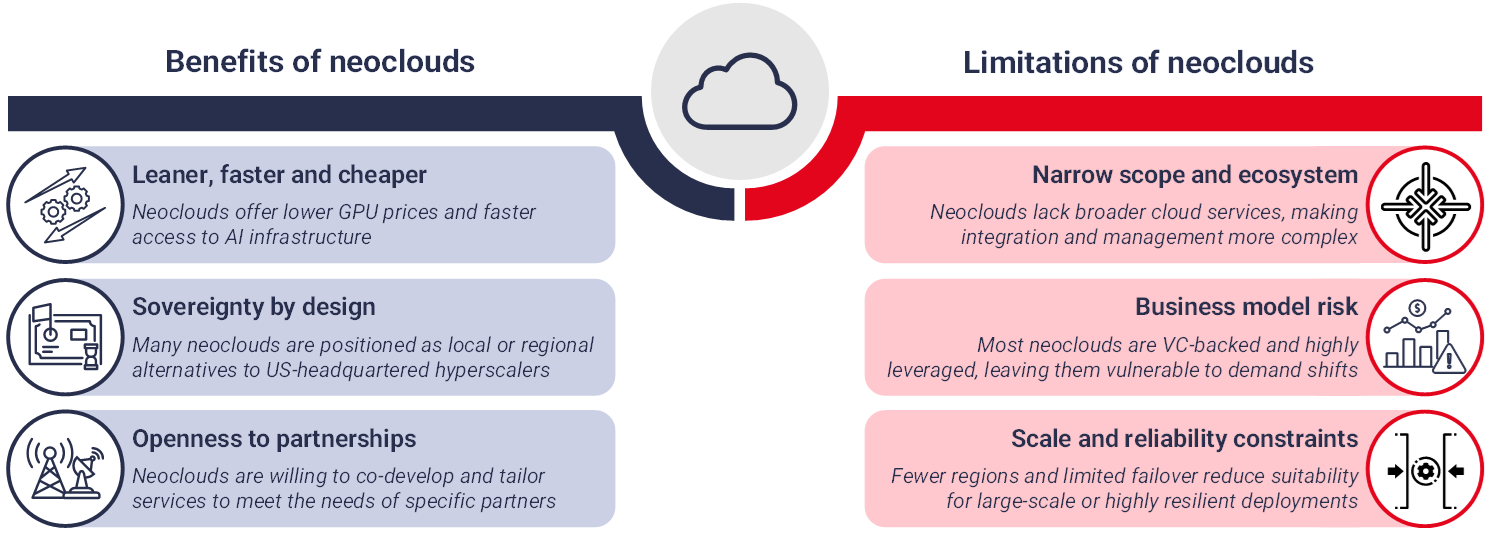

Leaner, faster, cheaper — for the right workloads

One of the biggest draws of neoclouds is cost efficiency. A 2024 analysis by Uptime Institute found that renting an NVIDIA H100 GPU via a hyperscaler could cost around $98 per hour, while neoclouds offered the same at just $34 — a 66% saving for equivalent performance.

This price difference stems from their focused model:

- No legacy services or stock keeping unit (SKU) complexity

- Homogenous infrastructure optimised for AI

- Lower operational overhead

Neoclouds also benefit from deploying newer technologies more quickly. Many operate high-density GPU racks with liquid cooling, optimised for model training and inferencing. These are often easier to implement in greenfield environments than in legacy data centres. As a result, they can offer performance-per-dollar advantages that appeal to organisations with compute-heavy, time-sensitive AI workloads.

Sovereignty by design

Several neoclouds — such as Core42 (UAE) or Scaleway (France) — are positioned as local or regional alternatives to US-headquartered hyperscalers. In markets where data sovereignty and data localisation are critical (particularly in the public sector or healthcare), this can be a meaningful differentiator.

These providers are also more likely to align with regional or national digital funding frameworks, offering an advantage in accessing public sector AI or cloud transformation initiatives.

Openness to partnerships

A key advantage of neoclouds is their flexibility and openness to partnerships. Unlike hyperscalers, which tend to offer fixed service models at global scale, neoclouds are often willing to co-develop and tailor services to meet the needs of specific partners.

This makes them attractive collaborators for players looking to:

- Monetise local infrastructure or fibre assets

- Launch sovereign or vertical-specific GPU-as-a-Service platforms

- Deliver AI capabilities at national or regional scale

Examples include SK Telecom’s partnership with Lambda Labs in South Korea, Verizon’s partnership with Vultr in the United States and various European telcos working with neoclouds to deploy GPU infrastructure closer to end customers. Similar models are emerging across other sectors, showing how neoclouds’ nimbleness and deal flexibility can be a strategic differentiator.

The limitations of neoclouds

Despite the momentum — exemplified by CoreWeave’s 158% market cap growth from USD 14 billion to USD 37 billion since its IPO in March 2025 — neoclouds are not without challenges, both operational and strategic.

Narrow scope and ecosystem

Most neoclouds are infrastructure-only providers. While they excel at offering GPU compute, they lack:

- Managed services (e.g. databases, data lakes, observability tools)

- Platform-level integration (seamless connections between services such as compute, storage, security, identity management, and monitoring within a unified environment)

- Enterprise onboarding and migration support

This creates additional complexity for customers looking to integrate GPU workloads into broader IT ecosystems. For example, a business running applications on AWS or Azure may find it easier to extend those workloads within the same ecosystem than to manage data transfer and orchestration across multiple clouds.

Business model risk

Neoclouds are often highly leveraged and growth-dependent. Many are VC-funded and operate on thin margins — relying on aggressive expansion and continued capital availability. With AI infrastructure investments surging, concerns about overbuild and capital discipline are growing.

Even prominent neoclouds have experienced rocky IPOs (such as CoreWeave) and valuation volatility. And while demand remains strong today, capital markets may tighten — especially if the current AI wave enters a slower growth phase, as some industry voices (including OpenAI’s Sam Altman) have suggested.

In parallel, the proliferation of providers is creating additional pressure. STL’s latest database identified over 130 active GPU-as-a-Service (GPUaaS) companies. This saturation raises the risk of commoditisation or market consolidation, where weaker or undifferentiated players may struggle to survive.

Neoclouds’ narrow focus on AI compute also makes them vulnerable if demand shifts or flattens. Unlike hyperscalers, they lack diversified revenue streams to fall back on.

Scale and reliability constraints

Hyperscalers have spent decades building global data centre networks, complete with:

- Redundant regions

- Resilient networking

- Extensive interconnects and failover

Neoclouds, in contrast, tend to have limited availability zones, often concentrated in a few markets. This makes them less suitable for:

- High-availability, multi-region architectures

- Global enterprise workloads

- Use cases with strict disaster recovery requirements

Many also rely on greenfield builds — which, while offering technical flexibility, face growing constraints around power access, land availability, and regulatory approvals, particularly in developed markets. STL Partners’ recent report “Can mobile base stations be transformed into edge AI data centres?” highlights that regulatory hurdles and grid connection delays can lead to deployment timelines of up to 84 months in some markets, such as Germany.

Figure 1: Benefits and imitations of neoclouds

Source: STL Partners

Source: STL Partners

Where hyperscalers retain the edge

Hyperscalers today offer far more than raw compute power. Their ecosystems encompass a vast range of integrated capabilities — from developer services such as GitHub Copilot and Google Vertex AI, to advanced machine learning platforms like Azure ML and Amazon SageMaker. They also design and deploy their own custom AI accelerators, including Google TPUs, AWS Trainium and Inferentia, and Azure Maia, while ensuring end-to-end security, compliance, and observability across their platforms.

For most enterprises — particularly those focused on applying AI models rather than training them — these services are deeply embedded within IT and developer workflows. The tight integration and ease of use often make the convenience of hyperscaler ecosystems outweigh the higher costs.

Beyond their software and platform advantages, hyperscalers also bring significant financial muscle and supply chain control. They can sustain multi-year GPU refresh cycles, invest in custom chips, and secure long-term supply agreements with NVIDIA and other hardware partners. This enables them to maintain pricing, gain faster access to next-generation hardware, and exert greater control over performance and cost trajectories.

As GPU demand begins to stabilise and hyperscalers optimise their AI offerings, the cost gap between hyperscalers and smaller neocloud providers may start to narrow.

The real picture: Complement, not competition

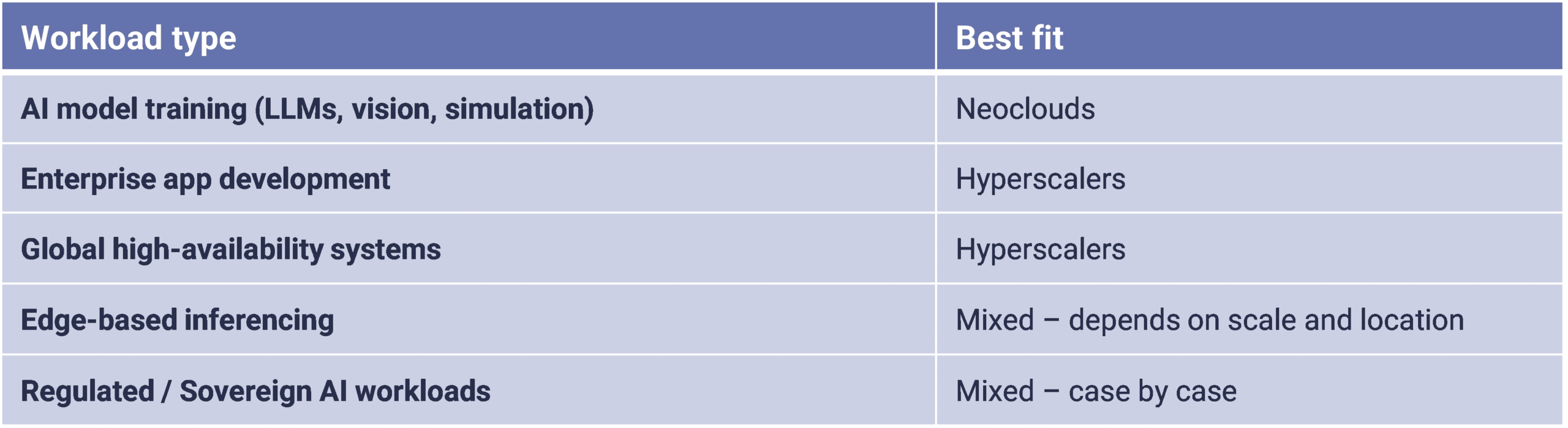

Rather than displacing hyperscalers, neoclouds are increasingly being used in complementary roles across both public and private cloud environments. Enterprises are adopting multi-cloud strategies, combining hyperscalers for general workloads with neoclouds for AI-specific tasks where high performance, lower cost, and sovereign hosting are critical.

This complementarity extends beyond public cloud: neoclouds are also working alongside private cloud deployments, including on-premise environments and regional colocation providers. In fact, even hyperscalers themselves occasionally source capacity from neoclouds, particularly when facing GPU supply constraints.

The table below shows how hyperscalers and neoclouds stack up across different workload types, reflecting where each currently has a comparative advantage

Figure 2: Split by workload type – neoclouds vs. hyperscalers

Source: STL Partners

Final thoughts: The role of neoclouds

Neoclouds represent a meaningful evolution in the cloud market. They offer AI-specialised infrastructure at competitive prices, with faster deployment cycles, and greater agility.

However, they are not a wholesale replacement for hyperscalers, nor without challenges of their own. Current deployment scale, financial resilience, and deployment breadth still matter. And hyperscalers are adapting fast — building AI-focused capacity, launching new platforms, and deepening their sovereign offerings.

For enterprises, the priority should not be to choose one over the other — but to develop intelligent, use-case-driven multi-cloud strategies, taking full advantage of the diversity the cloud market now offers.

Are you looking for advisory services in edge computing?

Download the Edge insights market overview

Download the Edge insights market overview

This 33-page document will provide you with a summary of our insights from our edge computing research and consulting work:

Neoclouds: The new cloud players vying for the AI crown

Neoclouds are reshaping the cloud computing landscape, offering GPU-accelerated infrastructure purpose-built for AI. As demand for AI outpaces hyperscaler capacity, these lean, specialist providers aim to deliver performance at a lower cost. This article explores what is driving the neocloud boom, and where their role lies in the ever-evolving AI landscape.

Edge GenAI: A new chapter for generative AI

This article explores the emerging role of Edge GenAI and the deployment of generative models on local devices such as sensors, smartphones and edge servers.

Strategies for telco infrastructure in an AI world: Part 2

This second instalment in our series on AI-driven opportunities for operators analyses the edge computing side of the equation and in particular the feasibility of operators hosting AI inference workloads.