Download

Neoclouds are reshaping the cloud computing landscape, offering GPU-accelerated infrastructure purpose-built for AI. As demand for AI outpaces hyperscaler capacity, these lean, specialist providers aim to deliver performance at a lower cost. This article explores what is driving the neocloud boom, and where their role lies in the ever-evolving AI landscape.

The cloud computing landscape has long been dominated by ‘the big three’ US-based hyperscalers – Amazon Web Services, Microsoft Azure, and Google Cloud – which together account for roughly two-thirds of global cloud spending. But a new category of cloud provider is emerging to challenge the status quo, driven by the explosive demand for artificial intelligence (AI) and high-performance computing. These newcomers, called neoclouds, are GPU-centric cloud companies offering high-performance infrastructure tailored to AI workloads at lower cost.

This shift marks a broader change in cloud computing. Where traditional clouds were built for general-purpose computing, neoclouds are AI-first by design, built around specialised hardware and tuned for performance. Their emergence presents both opportunities and disruption for telcos, enterprises, and cloud infrastructure players.

What are neoclouds?

Unlike general-purpose clouds, neocloud companies design their platforms AI-first, built around specialised hardware like GPUs and TPUs to handle intensive workloads in machine learning, data analytics, simulations, and more. Importantly, they are entirely new organisations dedicated to GPU-as-a-Service, which distinguishes them from hyperscale data centres that may adopt similar infrastructure but would not typically be classified as neoclouds. In practice, a neocloud operates massive clusters of GPUs and high-speed interconnects, renting out this compute power on-demand (often termed GPU-as-a-Service, or GPUaaS) to customers who need to train AI models or run other AI workloads.This design makes neoclouds ideal for training large AI models, running inferencing at scale, performing simulations, or any workload needing massively parallel processing. For example, training a large language model (LLM) could be done in a few days on a dense GPU setup from a neocloud.

Most neoclouds operate similarly to hyperscalers – users rent compute power via APIs, scale workloads dynamically, and pay per usage. However, where they differ is in focus, economics, and agility.

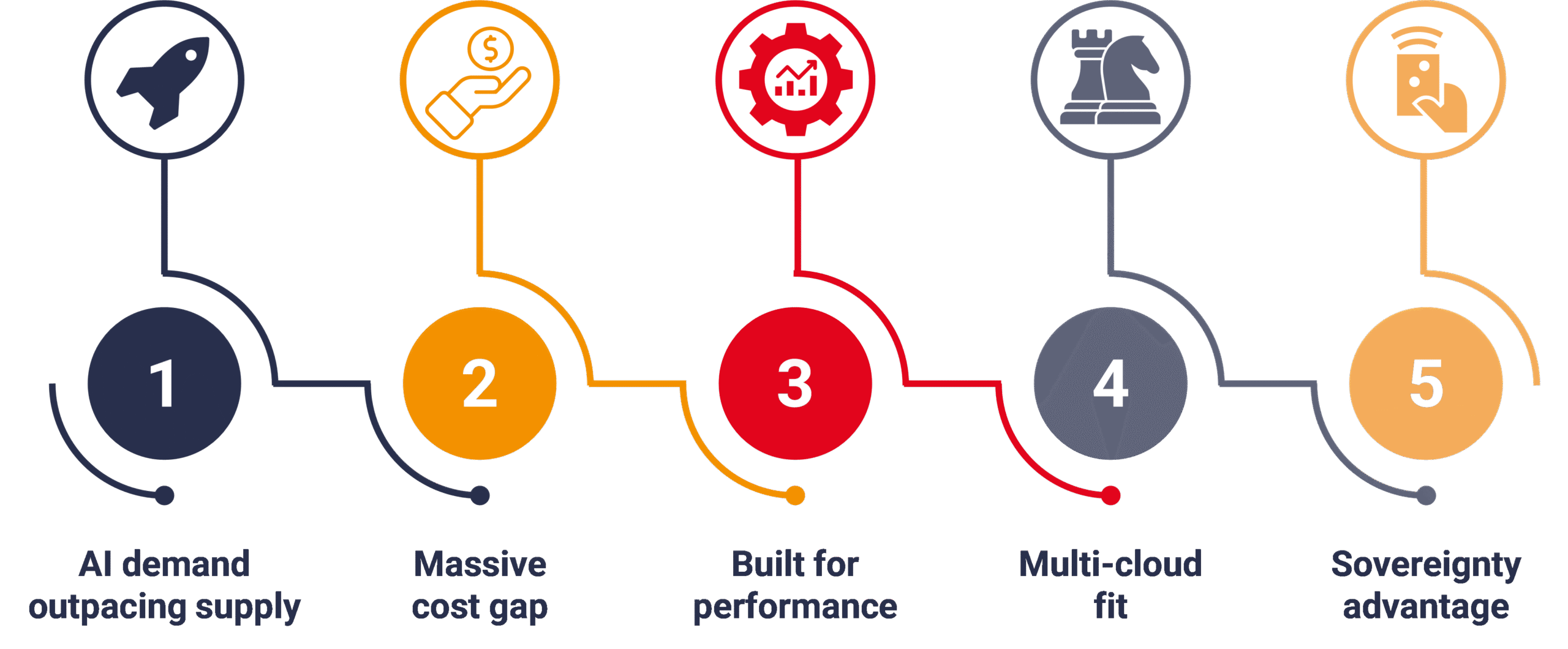

Why are neoclouds gaining traction?

Source: STL Partners

Several converging trends have fuelled the rise of neoclouds:

1. AI demand is outpacing supply:

The 2023-24 generative AI boom drove an unprecedented need for GPU compute – so much so that traditional clouds struggled to keep up. As such, renting a top-tier GPU like the Nvidia H100 became both costly and difficult. Neoclouds seized this opportunity, rapidly acquiring GPUs and attracting funding to build purpose-built AI infrastructure.

2. Massive cost gap:

Training AI models on hyperscalers can be expensive. Uptime Institute compared on-demand GPU instance pricing and found that an NVIDIA H100 server-hour averages around $98 with the major public clouds, versus about $34 with neocloud vendor. As such, by specialising solely in GPU rental and running lean operations, neoclouds can offer equivalent compute at 60–70% lower prices, making them highly attractive for scale-out AI projects.

3. Built for performance:

Neoclouds are engineered for AI. They use dense GPU clusters, liquid cooling, and high-speed interconnects to support massively parallel workloads. This hardware-first design delivers better performance for training and inferencing than CPU-centric, general-purpose clouds.

4. Multi-cloud fit:

Neoclouds help enterprises to achieve their multi-cloud strategies. While enterprises continue to rely on hyperscalers for general IT workloads, they are increasingly turning to neoclouds when they require scalable, high-performance AI infrastructure. This separation of concerns allows organisations to optimise for performance, cost, and vendor diversity – avoiding dependence on a single provider.

5. Sovereignty advantage:

With data localisation and digital sovereignty gaining prominence, especially in Europe, neoclouds offer advantages over US-based hyperscalers. Many are regionally headquartered or structured to align with local regulatory frameworks, making them better positioned to access public funding and serve industries with strict compliance requirements. This has drawn interest from both governments and telecom operators building domestic AI infrastructure.

It is clear that neoclouds arrived at a perfect storm of conditions: rising demand for AI, cloud GPU shortages, and the growing need for cost-effective, localised, high-performance compute. Industry forecasts reflect this momentum – the market for GPU-as-a-Service (encompassing hyperscalers and neoclouds together) is projected to grow from about $3.2 billion in 2023 to nearly $50 billion by 2032.

Key players and evolving ecosystem

A number of companies have emerged as prominent neocloud providers, each with a slightly different value proposition. Some of the leading neocloud players include:

1. CoreWeave is the largest neocloud provider, having pivoted from crypto mining to GPU cloud services. Backed by over $7 billion in funding, it now counts Microsoft, OpenAI, and Google among its clients. CoreWeave offers a range of GPU instances and has already hit $1B in quarterly revenue.

2. Lambda started with AI workstations and now offers both cloud and on-prem GPU clusters. Known for its developer-friendly tools, fast setup, and lower pricing, it’s popular among startups and research labs.

3. Crusoe Cloud takes a sustainability-first approach, repurposing stranded energy (like flare gas) to power GPU data centers. It raised $600 million in 2023 and markets itself as a low-emission option for AI infrastructure.

4. Nebius operates from Amsterdam and Finland, with plans to expand into the U.S. Initially tied to Russian-based web provider, Yandex, it now runs independently and targets enterprises seeking GDPR-compliant, non-U.S. AI cloud capacity.

These four are often seen as the leading neocloud providers, but the ecosystem is much broader. Dozens of other players are entering the space, from Paperspace (acquired by MosaicML) and Vast.ai (a peer-to-peer GPU marketplace), to hosting firms like OVHcloud, DigitalOcean, and Vultr, all offering GPU-based services. Even hardware vendors like Dell and HPE are entering the GPU cloud market.

Telecom operators have also thrown their hats in the ring, seeing neoclouds as an opportunity to leverage their infrastructure and local presence. In South Korea, for example, SK Telecom partnered with Lambda Labs to launch a GPU-as-a-Service offering. According to NVIDIA, at least 18 telcos globally are now building “AI factories” – GPU cloud data centers tailored for local use cases. With existing real estate, fiber networks, and enterprise relationships, telcos are well-positioned to deliver sovereign, latency-sensitive AI services. We have delved into the telco role in AI factories further in our recent report “Not all telcos need to build their own AI factories”.

Neoclouds signal a new era of cloud and edge infrastructure

Neoclouds have emerged as an important response to surging AI demand, offering high-performance, GPU-centric infrastructure with greater flexibility and often lower cost than traditional hyperscalers. Their rise has reshaped thinking across enterprises, telcos, and cloud infrastructure players, particularly for those seeking specialised, sovereign, or AI-first cloud services.

That said, the road ahead is uncertain. Market dynamics, capital intensity, and competition from hyperscalers will all shape their trajectory. But if neoclouds can navigate these challenges, they will remain a vital part of the AI infrastructure stack, especially for those seeking alternatives to the one-size-fits-all hyperscaler model. We will evaluate whether neoclouds are truly here to stay in an upcoming article on our Edge hub.

Are you looking for advisory services in edge computing?

Download the Edge insights market overview

Download the Edge insights market overview

This 33-page document will provide you with a summary of our insights from our edge computing research and consulting work:

Navigating AI Infrastructure: Can neoclouds challenge the hyperscale status quo?

Neoclouds are rising fast, offering GPU-first infrastructure built for AI workloads with lower costs and faster deployment than traditional clouds.

But are they truly in competition with hyperscalers like AWS, Azure, and Google Cloud — or playing a fundamentally different role? This article weighs the pros and cons of neoclouds and explores their place in an increasingly multi-cloud, AI-driven world.

Edge GenAI: A new chapter for generative AI

This article explores the emerging role of Edge GenAI and the deployment of generative models on local devices such as sensors, smartphones and edge servers.

Strategies for telco infrastructure in an AI world: Part 2

This second instalment in our series on AI-driven opportunities for operators analyses the edge computing side of the equation and in particular the feasibility of operators hosting AI inference workloads.