Download

Listen

Explore our AI-RAN hub

AI-RAN is moving from network optimisation to a broader platform opportunity, but most operators remain focused on efficiency-led use cases. This article quantifies the revenue and cost benefits across three models – AI-for-RAN, AI-and-RAN and AI-on-RAN – and shows how value scales as new service layers are added.

AI-RAN is rapidly becoming one of the most strategically important topics in telecoms. As we explored in our recent article on AI-RAN architecture, operators are not simply upgrading their networks – they are making choices about what role they want the RAN to play in the future digital ecosystem. At a high level, these choices can be understood across three models:

- AI-for-RAN: using AI to optimise network performance

- AI-and-RAN: enabling shared infrastructure for both telco and partner workloads

- AI-on-RAN: positioning the RAN as a platform for third-party applications

The three AI-RAN models represent a progression not just in technical architecture, but in economic ambition. Moving from AI-for-RAN to AI-on-RAN increases both potential returns and required investment. While these models are often discussed in parallel, the industry today is heavily concentrated on the first. AI-for-RAN dominates because it delivers clear and immediate benefits. However, it is also where value is most constrained, with gains driven primarily by cost savings and only modest new revenue. The more significant opportunity will emerge only as operators move beyond optimisation and begin to layer new services on top of the network.

AI-for-RAN: Value led by cost savings, with limited revenue upside

AI-for-RAN focuses on applying AI to improve network performance, automate operations and optimise resource utilisation. This delivers meaningful cost savings. Predictive maintenance reduces downtime and field operations, AI-driven automation lowers operational complexity and energy optimisation reduces one of the largest cost components in the RAN. These benefits are immediate and relatively low risk, which explains why they are the primary focus of current deployments.

Efficiency gains from AI-for-RAN deployments are already being demonstrated in live networks. For example, Samsung and SK Telecom deployed an AI-based cell sleep solution across around 8,000 sites, achieving ~14–15% average energy savings and up to ~20%+ during off-peak periods, while maintaining network performance. Alongside energy savings, SK Telecom and Samsung have shown that AI-based optimisation can automatically tune base station parameters based on local conditions, improving coverage and user experience while reducing manual intervention.

More advanced optimisation approaches are also emerging. SoftBank, in collaboration with Red Hat, has demonstrated how its AI-RAN platform, AITRAS, can optimise resource utilisation across both network and compute layers. By integrating llm-d – an open source framework for distributing LLM inference across multiple nodes – the platform enables more efficient, dynamic allocation of compute resources between AI and RAN workloads.

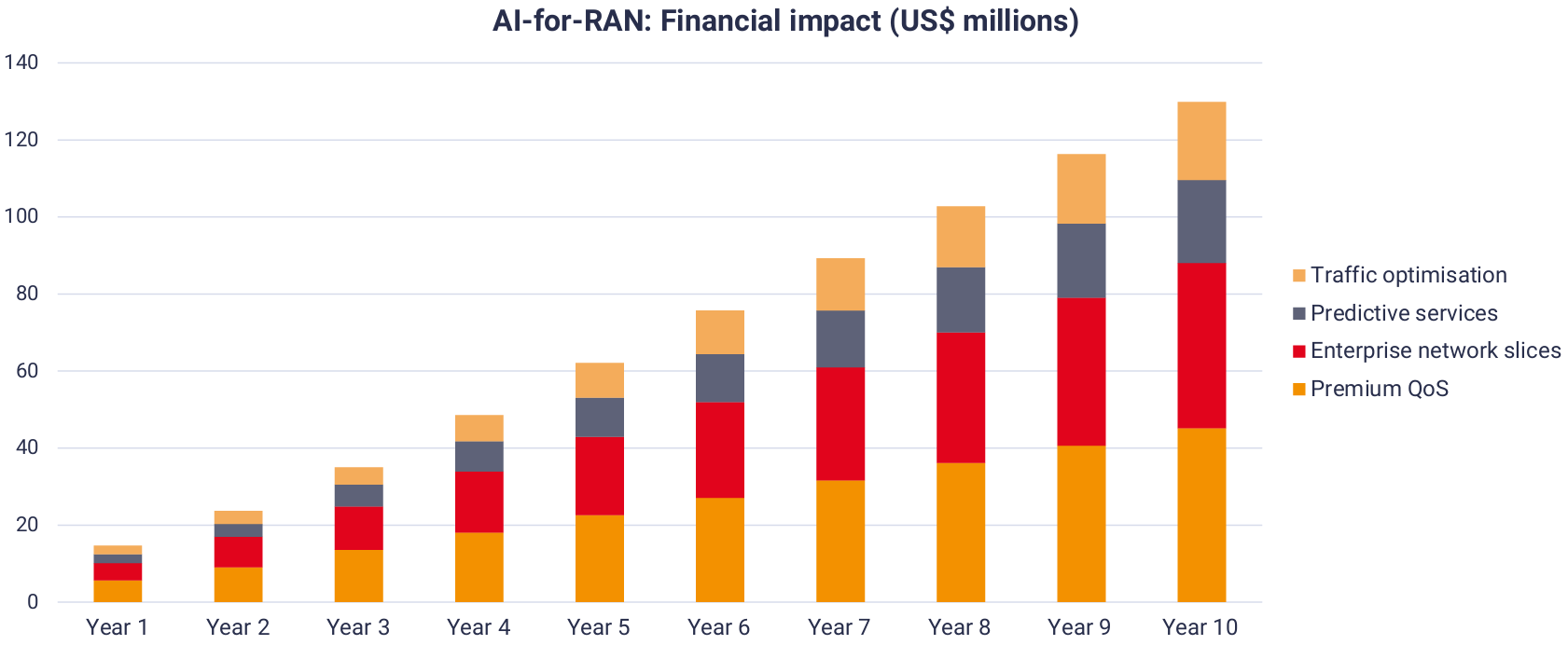

However, when looking at revenue, the picture is much more constrained. By year 10, total incremental financial impact could reach around US$ 130m for a mid-sized operator, equivalent to around 1.7% uplift over the base case. This reflects the fact that revenue is still tied closely to connectivity. The revenue stack in this model is built from four service categories: premium QoS, enterprise network slicing, predictive services and traffic optimisation. These are all valuable, but they represent enhancements to existing services rather than fundamentally new value pools.

Figure 1: Financial impact from AI-for-RAN deployments could reach US$ 130 million

Source: STL Partners

This is the key limitation of AI-for-RAN. It delivers clear efficiency gains, but only modest revenue growth. On its own, it is unlikely to justify the full scale of investment in AI-native infrastructure.

AI-and-RAN: Adding new revenue layers through ecosystem participation

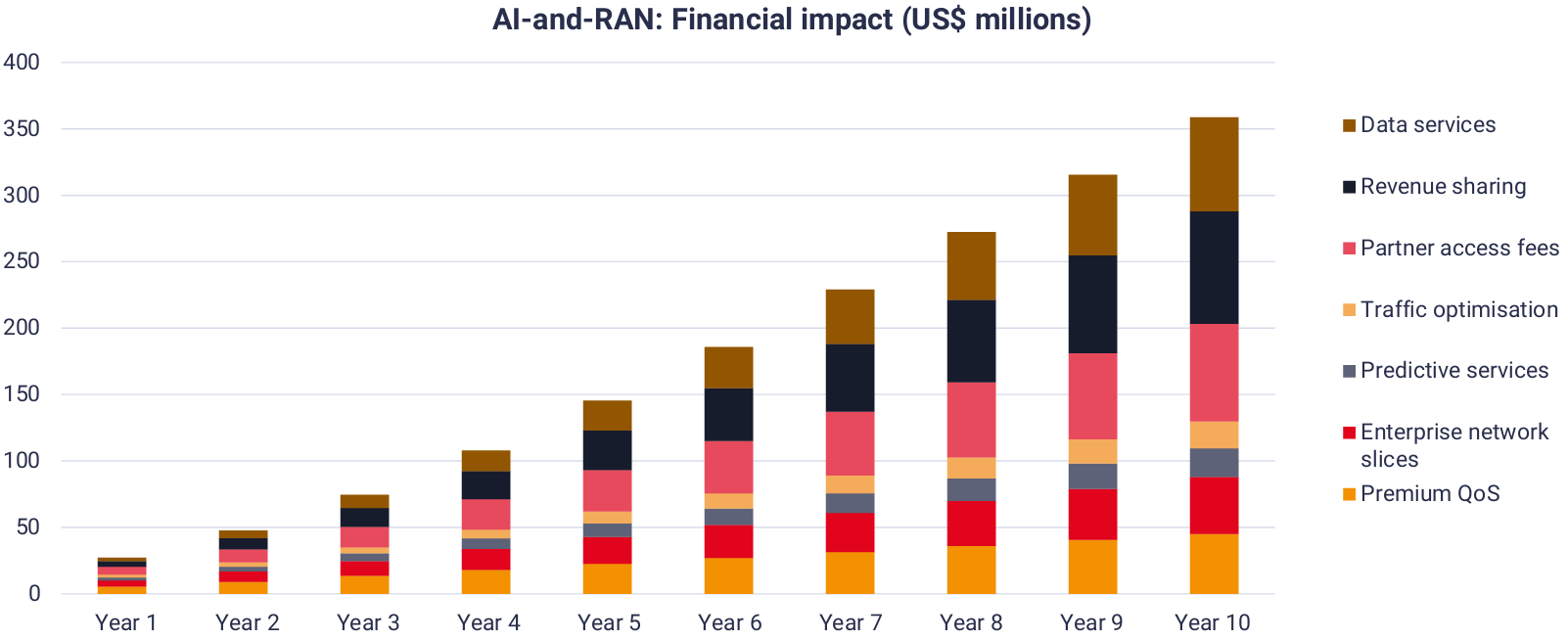

AI-and-RAN model builds directly on the base set out by AI-for-RAN. The cost-saving benefits of AI-for-RAN remain, but the key shift is the introduction of new revenue streams enabled by partners. By allowing third parties to deploy workloads on AI-RAN infrastructure, operators move from a single-layer business model to a multi-layer one. The same network can now generate value not only through connectivity, but also through applications and data. This is reflected in the revenue profile in our model. By year 10, incremental revenue increases to US$ 359 million, corresponding to around 4.8% uplift on an operator’s base revenue.

Figure 2: Financial impact from AI-and-RAN deployments could reach US$ 360 million

Source: STL Partners

Crucially, this growth is not driven by replacing existing services, but by stacking additional ones on top. The original connectivity revenues remain, but are complemented by:

- Partner access fees

- Revenue sharing from applications

- Data services based on network insights

This stacking effect is central to the improved business case. It allows operators to monetise the same infrastructure multiple times. For example, an enterprise slice can support a partner application, generating both access fees and a share of application revenue. The types of services driving this additional revenue are also broader. They include applications such as autonomous vehicle coordination, smart city platforms, and financial security systems – use cases that depend on low-latency compute and real-time data processing.

At the same time, cost savings continue to play an important role. Shared infrastructure and improved resource utilisation increase efficiency, while AI-driven optimisation continues to reduce operational costs. The result is a more balanced value proposition. Cost savings remain important, but new revenue becomes a meaningful driver of ROI.

There are increasingly concrete trials demonstrating the feasibility of AI-and-RAN models. SK Telecom has carried out live network demonstrations with partners including Nokia and Intel, showing that a single base station can simultaneously process both communication traffic and AI workloads using shared GPU-based infrastructure, while maintaining carrier-grade performance. These trials validated key capabilities such as dynamic resource allocation between AI and RAN functions and real-time optimisation of compute resources, providing early evidence that operators can support multiple workloads on the same infrastructure.

This shift towards shared infrastructure is reflected in a broader ecosystem of vendors working to support cloud-native RAN and AI platforms. For example, Nokia has highlighted its collaboration with Red Hat to provide a common cloud-native foundation for AI and network workloads, enabling operators to deploy and scale services consistently across environments.

In parallel, SoftBank’s AITRAS platform is evolving towards a more open ecosystem model. By contributing key orchestration capabilities such as its Dynamic Scoring Framework to open source projects, SoftBank is enabling more efficient multi-cluster resource optimisation and lowering barriers for partners to build on AI-RAN infrastructure.

AI-on-RAN: Scaling revenue through platform dynamics

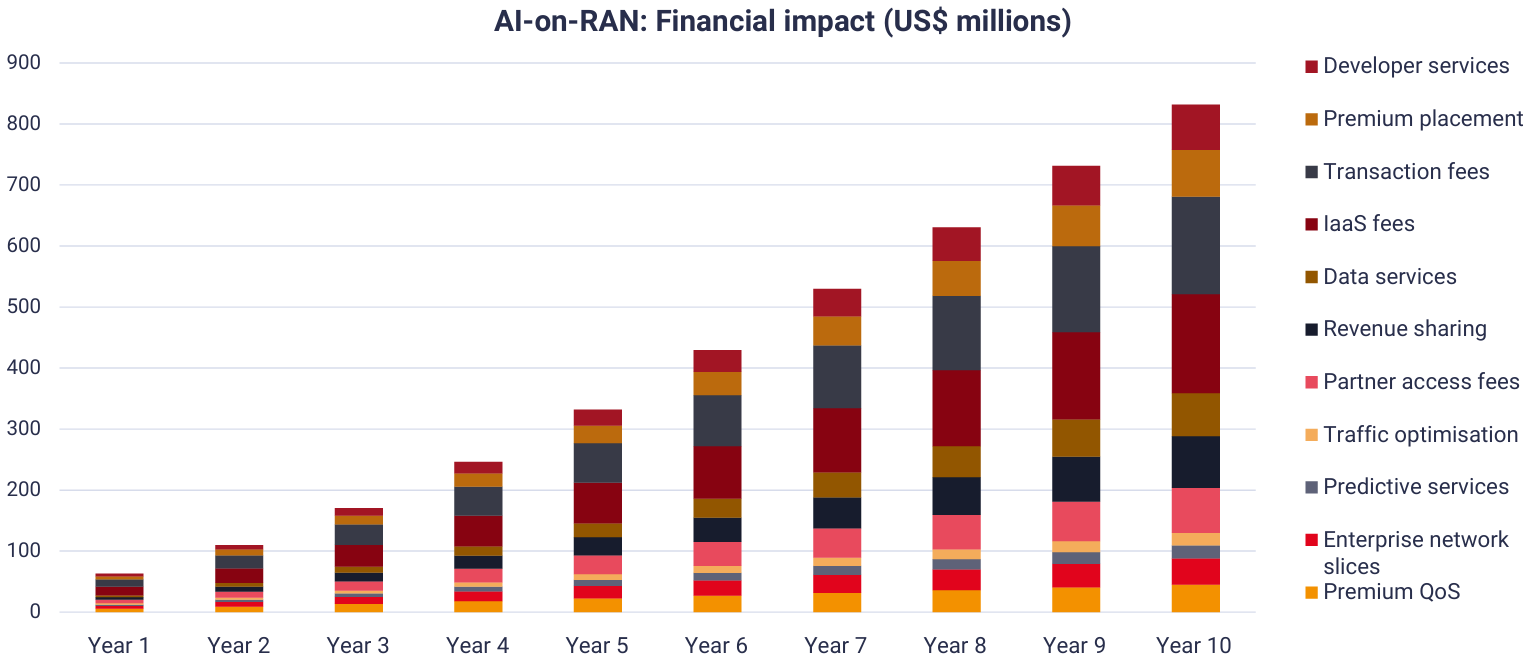

AI-on-RAN model extends this logic further. Instead of enabling selected partners, operators create a platform where a wide range of developers and enterprises can deploy applications. This significantly expands the revenue opportunity. By year 10 in our model, incremental revenue reaches around US$ 850 million, representing an 11% uplift on base revenue.

Figure 3: Financial impact from AI-on-RAN deployments could reach US$ 850 million

Source: STL Partners

Again, the key is cumulative growth. All previous revenue streams remain in place, but are supplemented by additional layers, including:

- Infrastructure-as-a-Service

- Marketplace transaction fees

- Developer services

- Data marketplace revenues

What differentiates this model is how revenue scales. Unlike the earlier models, where growth is relatively linear, the marketplace introduces platform effects. As more participants join, utilisation increases, transaction volumes grow and new services emerge. This is reflected in the steeper revenue curve in the later years of the model. Cost savings still play a role – particularly through more efficient utilisation of infrastructure – but they are no longer the primary driver of value. Instead, revenue growth becomes the dominant factor, driven by the expansion of the ecosystem.

This marks a fundamental shift. The operator moves from monetising connectivity to orchestrating and capturing value from a broader service ecosystem. While still early, there are field trials that point towards the AI-on-RAN model. SoftBank and NVIDIA have conducted what is described as the first outdoor AI-RAN field trial, demonstrating a fully virtualised RAN running on GPU-based infrastructure capable of supporting both network functions and AI applications in parallel. The trial validated key capabilities required for a platform model, including multi-tenancy between AI and RAN workloads, orchestration of shared resources, and the ability to run real-world AI applications on the network. Importantly, it also demonstrated that AI-RAN infrastructure could support an “AI marketplace” concept, where applications are created and consumed on top of the network.

Similarly, QCT, working with NeuroRAN, Red Hat and SUTD, has demonstrated AI-on-RAN orchestration use cases, validating real-time AI inference workloads – including vision-language models and robotics – across device, edge and cloud environments. These examples highlight how shared infrastructure can support both connectivity and AI-driven services on the same platform.

The foundation: Enabling AI-RAN at scale

While the three AI-RAN models differ in their revenue profiles, they share a common dependency: the ability to run network functions and AI workloads on the same infrastructure. In practice, this means deploying a cloud-native and AI-native foundation that can support both RAN and AI workloads across distributed cloud and edge environments. This includes enabling GPU-as-a-service and AI-as-a-service capabilities alongside traditional network functions, allowing operators to allocate resources dynamically across different use cases.

Open source plays an important role in this foundation, particularly in supporting flexibility, automation and interoperability across multiple vendors and partners. This becomes increasingly important as operators move from isolated optimisation use cases towards more complex, multi-party ecosystems. Without this shared platform layer, the three AI-RAN models cannot be implemented seamlessly. It is this foundation that allows operators to move from improving network efficiency to enabling and scaling new services on top of the network.

Recent industry developments reinforce this direction. For example, Red Hat’s participation in initiatives such as OCUDU (Open Centralized Unit / Distributed Unit) Ecosystem Foundation highlights the growing focus on open collaboration to support the scaling of AI infrastructure across hybrid cloud and edge environments.

Building value beyond optimisation

AI-RAN is often framed as a technological evolution, but its real significance lies in how it reshapes the revenue model of telecom operators. While cost savings from AI-for-RAN are tangible and provide a clear entry point, they represent only a fraction of the overall opportunity. The more meaningful value lies beyond optimisation. As operators move from AI-for-RAN to AI-and-RAN and ultimately AI-on-RAN, the focus shifts from efficiency to monetisation – layering new services, enabling partner ecosystems and, eventually, building platform-based business models. This is not simply a progression in architecture, but a shift in how value is created and captured.

The challenge that operators face now is one of ambition and timing. Moving too slowly risks locking into a low-growth, efficiency-led model. Moving too quickly introduces execution and investment risk. Ultimately, the question for operators is not whether to adopt AI-RAN, but how far they are willing – and able – to go beyond its first layer. The long-term winners will be those that successfully transition from optimising networks to enabling and capturing value from a broader ecosystem of AI-driven services.

Are you looking for advisory services in AI-RAN

Download the AI-RAN market overview

Download the AI-RAN market overview

AI-RAN is shifting from hype to practical strategy. This overview pack explains what AI-RAN is, why it matters now, and how operators can capture value.

Next phase of AI-RAN: Solving operational challenges to unlock new opportunities

AI-RAN is rapidly evolving from a network optimisation technology into a platform for new revenue generation.

AI-RAN architecture: A practical guide for operators

AI-RAN has become one of the hottest topics in telecoms, attracting significant attention and investment across the ecosystem, from operators and network equipment providers to chipmakers.

An insight into the future of AI-RAN

Discover insights from our recent interview with Dr. Alex Jinsung Choi on the AI RAN Alliance’s vision, drivers of RAN evolution, and how AI RAN tackles key industry challenges.

What is physical AI? Definitions, examples and implications for private networks

The term physical AI refers to the transition of AI from the mostly digital sphere into more real-world scenarios and physical processes.

How AI can accelerate IT and OT convergence to transform customer experience

AI can play a central role in enabling convergence, acting as a unifying intelligence layer across IT and OT.

Edge computing at MWC 2026

In contrast to previous years, when edge computing had drifted somewhat to the periphery of the agenda, it was more prominent at MWC 2026, with discussions and demonstrations across the Fira reinfo…