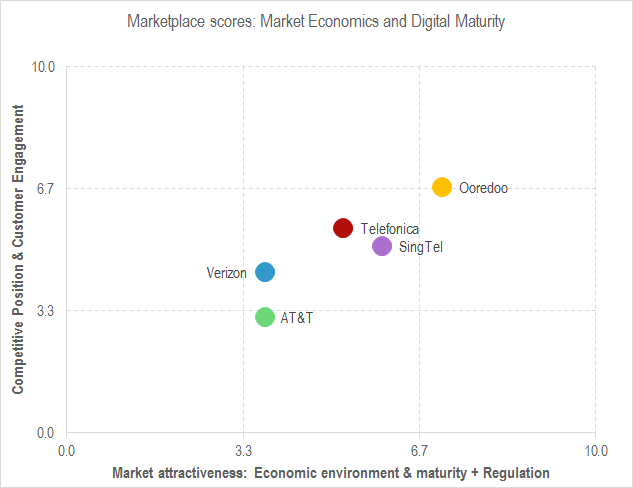

Are Telefonica, AT&T, Ooredoo, SingTel, and Verizon aiming for the right goals?

Operators face difficult choices on the best way to change their business models. In this note we analyse the approaches taken by AT&T, Verizon, Ooredoo, Singtel and Telefonica, extrapolate the options for all carriers, and offer a framework to help managers define the right new business model goal for their organisation.