Login to access

Want to subscribe?

This article is part of: Edge Insights

To find out more about how to join or access this report please contact us

Liquid cooling is creating a new M&A battleground in data centres, where different buyer groups are pursuing distinct acquisition strategies to control an increasingly critical part of the infrastructure stack.

Welcome to our ‘Coffee break reading’ series. These pieces are designed to be short and easy to read, presenting our opinion on a hot topic and challenging you to think about it too.

The battle for liquid cooling ownership

Liquid cooling is no longer just a technology question for AI-ready data centres; it is becoming an ownership question. In our recent coffee break read, we argued that the rise of liquid cooling is creating a new consolidation wave in data centre infrastructure, as coolant distribution units (CDUs) and related fluid systems move from niche high performance compute (HPC) and limited hyperscale deployments into the core of future scaled AI buildouts. That shift matters because the value is no longer just in the hardware itself, but in the ability to control the system around it – from cooling architecture and integration to service, support and roadmap influence.

This report looks at which buyer groups are best placed to ride that wave.

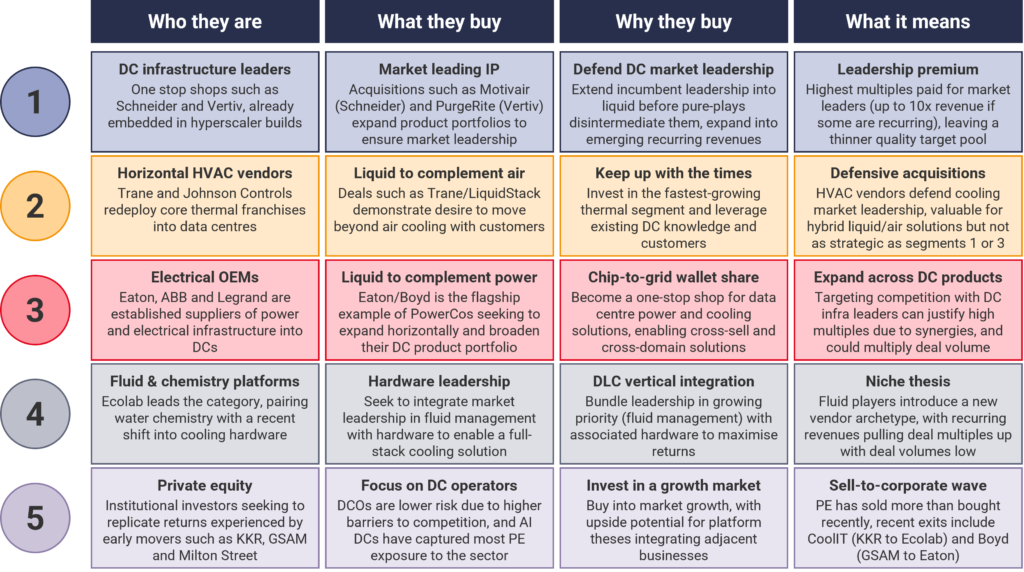

Acquisition archetypes in the liquid cooling ecosystem

Source: STL Partners

This figure above sets out five archetypes who are already playing a role in the M&A activity which is reshaping the liquid cooling vendor landscape. Almost every archetype – incumbents defending market leadership, HVAC vendors keeping pace, electrical OEMs cross-selling, chemistry players going full-stack – is converging on integrated, recurring-revenue cooling platforms, even as their starting points and risk appetites differ sharply. The clearest divide is between buyers rounding out product portfolios (data centre [DC] infrastructure leaders and electrical OEMs, where incumbency and cross-sell justify the richest multiples) and those engaging in a narrower defensive strategy (HVAC) or niche speculative play (fluid & chemistry platforms). Private equity, meanwhile, has predominantly flipped from buyer to seller, recycling capital out of cooling specialists and into DC operators where moats are deeper and anchor contracts offer outsized risk-adjusted returns. The implication is that the M&A contest is less about who wants liquid cooling, and more about how different archetypes are using such transactions to build a competitive portfolio in an increasingly crowded market.

The common thread is that liquid cooling is moving from a component sale to a system sale. As AI workloads push higher densities and reliability expectations rise, customers are increasingly looking for global, scalable and integrated platforms rather than isolated discrete products, and leading companies in the sector are proactively transacting their way to such a product portfolio.

If you are not a subscriber, enter your details below to download a free copy of the report

Related research

- Liquid cooling: The next consolidation wave in data centre infrastructure

- Data centres and water: Understanding the real impact